Nascent Social Bond Fund Sector Faces Implementation Challenges

Dedicated social bond funds, such as the social bond strategy announced recently by Amundi, may face heightened single-name concentration risks as a result unless they have latitude to invest in a wider array of instruments than just social bonds.

Article also available in :

English ![]() |

français

|

français ![]()

Dedicated social bond funds may initially be constrained in their ability to diversify effectively, Fitch Ratings says. Social bond issuance has been limited both in terms of volumes and active issuers. Dedicated social bond funds, such as the social bond strategy announced recently by Amundi, may face heightened single-name concentration risks as a result unless they have latitude to invest in a wider array of instruments than just social bonds.

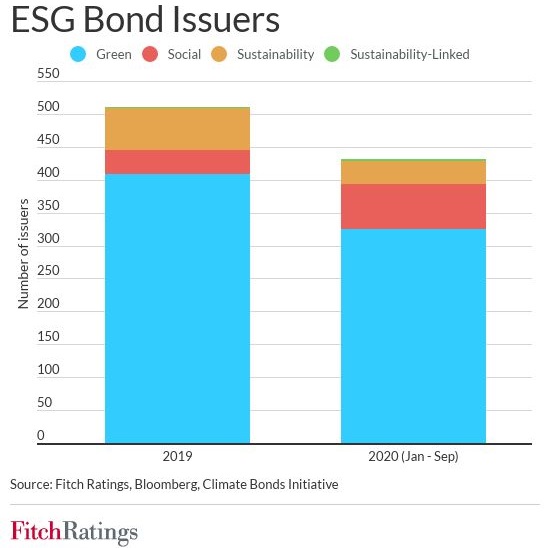

Fitch is aware of just two social bond funds launched - one managed by Columbia Threadneedle (GBP260 million at end-October 2020) and the recently announced Amundi fund - demonstrating a sector in its infancy. However, the recent upsurge in social bond issuance may lead to more fund launches. Growth in issuance has been rapid, driven mainly by greater investor focus on humanitarian considerations spurred by attention on social inequalities highlighted by the coronavirus pandemic. Social bonds issued in January-October 2020 amounted to USD85 billion, according to media reports, far more than the USD10.9 billion issued in 10M19.

By way of comparison, as green bond issuance has increased, so too have assets in dedicated green bond funds, with green bond fund assets growing more rapidly than bond funds overall (albeit from a low base). As well as launches of green bond funds, several existing funds have converted to green bond strategies. Investor demand has been strong, consistent with increasing investor interest in ESG. This suggests that social bond funds may also attract significant inflows.

Issuer selection criteria will be an important differentiating factor between social bond funds as the sector develops. Most social bond issuance has been from government agencies, development banks and banks. This means that social bond fund investors, at least initially, are likely to face concentration risk, with exposure to a limited number of sectors and potentially issuers. The green bond fund sector took several years to achieve a broad ability to diversify effectively, due to green bond issuance dynamics.

Some social bond funds may be able to invest in social bonds that are not necessarily labelled as social bonds. This is consistent with the green bond fund segment, where funds will typically express a minimum percentage of (labelled) green bonds, while being able to invest some other percentage in unlabelled bonds that still meet the fund’s other investment criteria (for example, an unlabelled bond issued by a "green" issuer). The Amundi social bond strategy has a stated minimum of 75% investment in social bonds.

A more fundamental question for social bond funds - and social bond investors in general - will be social bond selection. The range of issues addressed by green bonds is narrower than that which can be addressed by social bonds. This may make bond selection more challenging, particularly in the case of "linked" bonds that reference key performance indicators (as opposed to "use of proceeds" bonds), such as the sustainability-linked bond issued this year by Novartis.

Much of the surge of social issuance in 2020 was driven by the coronavirus and future issuance is likely be shaped by a long-lasting increase in focus on social issues as a result of the pandemic.

ESG factors do not directly affect Fitch’s fund ratings unless they also affect factors such as fund credit quality, duration, liquidity and concentration. However, potentially higher concentration levels in social bond funds could be negative for ratings.

Next Finance , December 2020

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |