Most turbulences are behind for merger arbitrageurs

Market volatility also played out, as well as the growing share of jumbo deals, usually more sensitive to adverse developments. Amid very supportive conditions for M&A (from the tax reform in particular), weaker deal rationales are also mentioned as a greater source of deal volatility.

Article also available in :

English ![]() |

français

|

français ![]()

Markets remained treacherous with multiple micro, macro and political movers. Trade concerns receded but remain live as the U.S. tackles Chinese tech. Investors also weighted the implications of a U.S. withdrawal from the Iran nuclear agreement. We expect the issue to hover at least until the summer and Iran to be initially cautious in its response before considering a more radical path. Besides, investors kept on digesting (strong) EPS reports, particularly sensitive to any guidance suggesting an earnings peak. Overall, investors are increasingly pricing a growth stagnation with higher inflation, in the U.S. especially. As a result, cyclical assets weakened, rates surged and boosted USD. This helped European and Japanese markets outperform.

CTAs and the U.S. long-biased managers were the most affected by current uncertainties. Merger funds also took a hit from bond yields and several deals’ unfavorable developments. The other strategies were resilient.

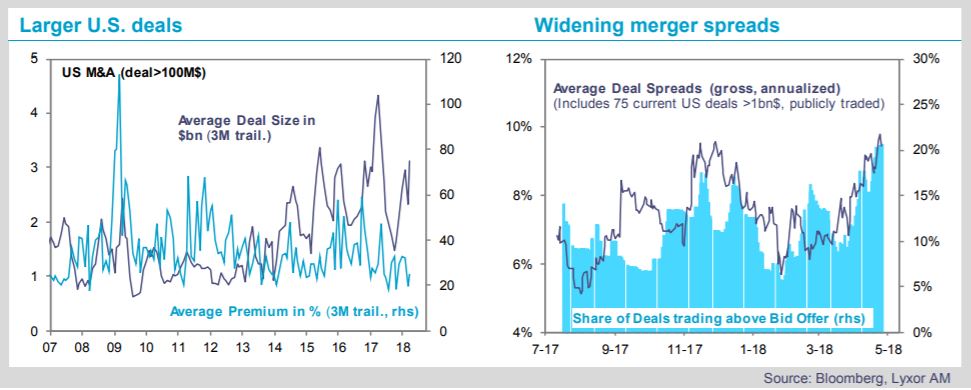

Since February, merger spreads widened meaningfully.

Rising bond yields, a key component of merger returns, contributed to about half of the widening. A hike of 50bp in Libor implies about a 150bp widening in annualized spreads. A second key factor was increased regulatory and deals’ duration uncertainty, in the U.S. but also for operations related to China one way or the other. An obvious example was the NXP Semiconductors / Qualcomm deal, under pressure from these factors and a key negative contributor for many funds. Market volatility also played out, as well as the growing share of jumbo deals, usually more sensitive to adverse developments. Amid very supportive conditions for M&A (from the tax reform in particular), weaker deal rationales are also mentioned as a greater source of deal volatility.

These turbulences are not shaking managers’ faith, to the contrary. While they expect rising rates to translate into structurally higher deal spreads going forward, they believe most of the downside is now priced, with more appealing entry prices. Their high leverage reflects their confidence.

Jean-Baptiste Berthon , Lyxor Research , May 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |