What’s behind the rally in global macro strategies

According to our estimates, CTA and Global Macro strategies have so far extended their winning streak in July. While we recently talked about the reasons for the outperformance of CTAs (+9.3% year-to-date), the performance of Global Macro strategies is a bit more ambiguous, due to the elevated dispersion between strategies.

Article also available in :

English ![]() |

français

|

français ![]()

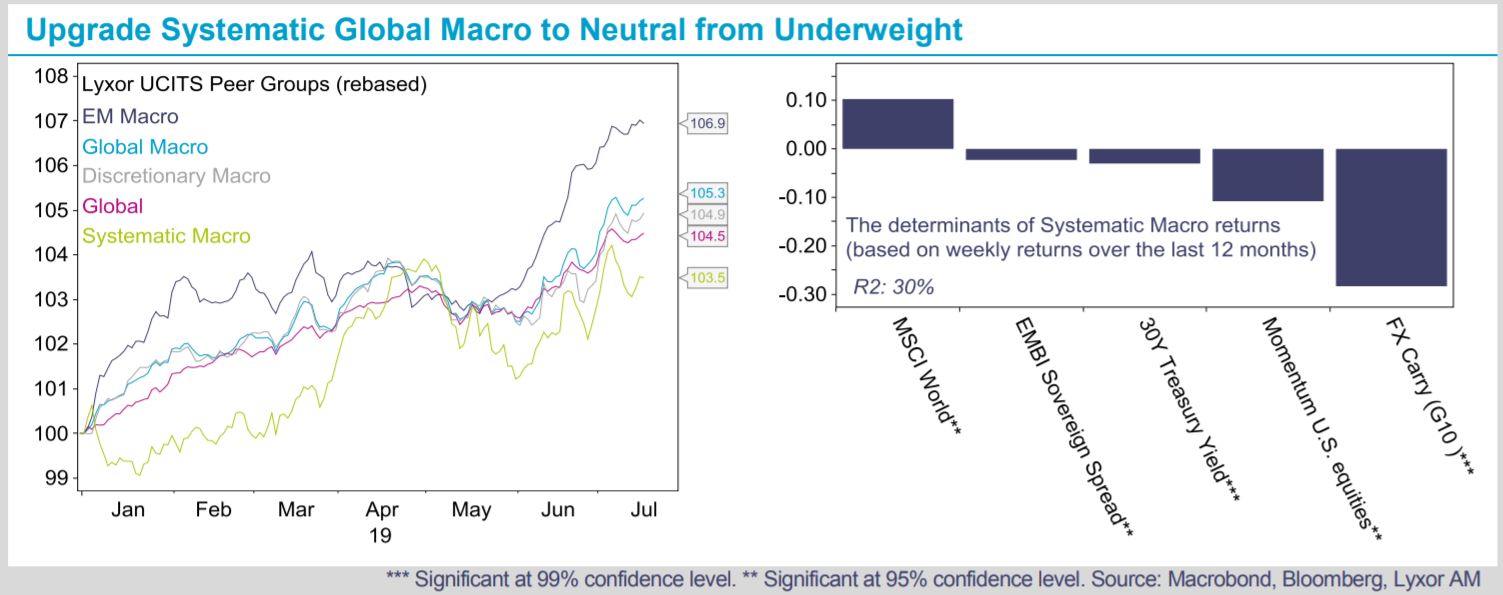

Global Macro strategies are up +5.3% year-to-date according to the Lyxor Global Macro Peer group, which pools together 40 UCITS strategies. A significant part of such performance has been delivered by Emerging Markets (“EM”) strategies (+6.9%), while Discretionary and Systematic ones lagged (+4.6% and +3.5% respectively). This was hopefully in line with our expectations. Our stance on EM-Macro has been Overweight for several months, while were more defensive on Discretionary (at Neutral) and Systematic strategies (at Underweight).

The factors behind EM-Macro returns are quite immediate. We explain the bulk of their returns over the past 12 months with two variables: an EM Currency Index and an EM Hard Currency Sovereign Bond Index. Concurrently, Discretionary managers’ returns during the same period can be partly explained by: i) curve flattening trades in the 2-10y segment in the U.S., ii) buying positions on EM assets (FX, bonds, equities), and iii) selling positions on FX carry and long-dated Treasuries (30 year). However, it is trickier to explain the returns of Systematic strategies.

Despite our efforts, we manage to explain only 30% of their recent returns with five variables: i) buying positions on global developed equities and long-dated Treasuries, ii) selling positions on the momentum equity risk factor and FX carry and, iii) positions which benefit from a tightening of EM sovereign spreads.

Going forward, we upgrade our stance on Global Macro strategies from Underweight to Neutral. We particularly upgrade Systematic Macro strategies to Neutral on the back of the Fed managing to lift growth expectations. We believe the Fed has both the room and the willingness to act and push forward our expectation for the first rate cut to the end-July FOMC meeting. Meanwhile our stance on EM sovereign bonds stays constructive and we upgraded U.S. equities to Overweight. Our scenario assumes that the trade truce will be extended since the U.S. administration is cornered by the presidential election next year. Trade uncertainty has caused a growth deceleration. Further escalation could dip the U.S. economy into a recession.

Lyxor Research , July 2019

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |