| https://www.next-finance.net/en | |

|

Strategy

|

With budget stimulus talks in the U.S. likely to move forward soon, and despite deadlocked Brexit negotiations, risk assets set new records in the U.S. The S&P 500 is now up +13% since end-October, before the results on the Pfizer vaccine were announced. With modest earnings revisions, the forward P/E ratio jumped above 22x expected earnings in 2021 according to I/B/E/S, close to the late ‘90s record highs. Despite rich equity valuations, the availability of a Covid-19 vaccine and the looming normalization in economic activity prevents investors from being too defensive.

In this context, alternative strategies that can bring both performance and diversification are attractive. Global Macro strategies can deliver on both fronts.

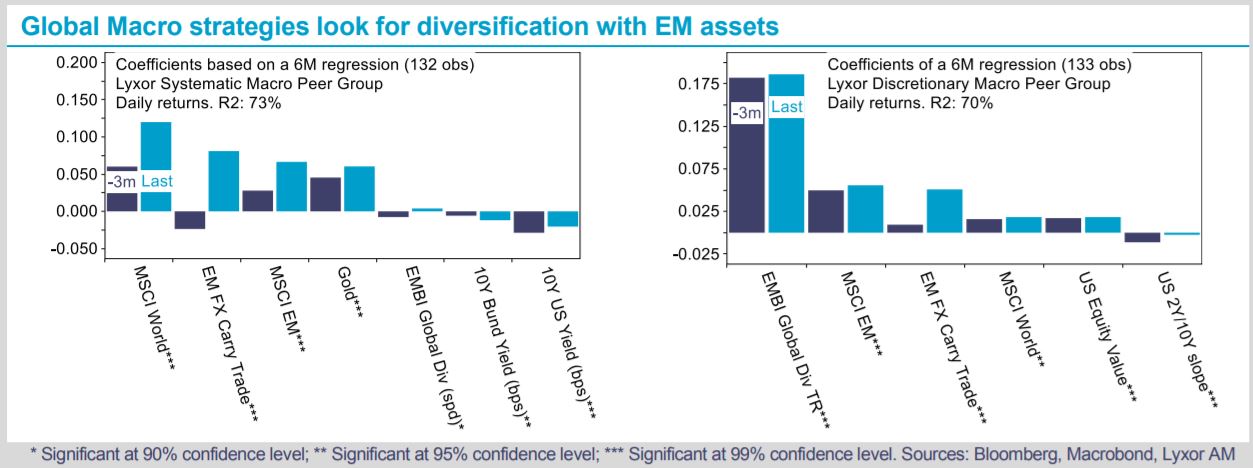

Global Macro strategies are quite heterogeneous, from pure fixed income players to multi asset strategies, discretionary or Systematic, invested in Developed or Emerging Markets, or both. We split the universe into EM, Systematic and Discretionary and find that i) they normalized their equity market beta at higher levels but in moderate proportions, especially for Discretionary strategies; ii) they remain long fixed income but often with decreased and reshuffled positioning and remain exposed to Gold as central banks keep expanding their balance sheet; and iii) maintain an elevated bias towards EM assets, in particular on currencies such as the CNY/ CNH, MXN, RUB and INR vs. USD. The EM FX carry trade, a strategy that borrows low-yield currencies to invest in highyield ones, is back. It was popular in the late ‘00s but did little since then, according to Bloomberg’s EM-8 Carry Trade index.

Yet, current positions from Global Macro strategies on EMFX appear to be backed by fundamental analysis, not a systematic risk premia approach.

Our stance on Global Macro strategies stands at Overweight, with a preference for Discretionary and EM strategies. The former tends to have a tactical bias which appears relevant at the trough of the business cycle. With regards to EM Macro, they may benefit from the improved credit profile of energy and metal exporters amid rising commodity prices. Carry strategies such as EM sovereign credit remain appealing as major central banks keep a lid on yields.

Lyxor Research , December 2020

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |