Merger Arbitrage outlook for H2 2019

M&A patterns are also showing healthy dynamics. A healthy number of hostile deals (usually riskier but more profitable) tends to concentrate on smaller targets. Jumbo deals are increasingly funded by stock and cash combinations, also favorable for arbitrageurs.

Article also available in :

English ![]() |

français

|

français ![]()

This week, we take a deeper look at the Merger Arbitrage strategy and its environment.

While off from recent peaks, the flow of M&A stands at its 20 years average. Persisting trade wars and Brexit uncertainty continued to take their toll on manufacturing, exports and now capex. It is weighting on executive confidence and delaying some corporate operations. Yet, these concerns do not seem to question the relevance of external growth, amid stalling internal growth opportunities, and declining reward from pure investors distribution strategy. Additionally, liquidity conditions remain supportive. Companies accumulated more debt and have less cash, but funding costs are low and acquirers continue to get banks’ support as well as credit access. Moreover, corporate valuations (and hence M&A opportunities) remain affordable. In the U.S., the equity market value is in aggregate 14% richer than the replacement cost (a more relevant book-value estimate), marginally higher than the long-term average.

M&A patterns are also showing healthy dynamics. A healthy number of hostile deals (usually riskier but more profitable) tends to concentrate on smaller targets. Jumbo deals are increasingly funded by stock and cash combinations, also favorable for arbitrageurs. At 30% in average, deal premiums are attractive, yet not so high as to jeopardize operations. All in all, by most measures, M&A activity, which sets the menu of opportunities for arbitrageurs, is consistent with mid-cycle patterns, neither too hot, nor too cold.

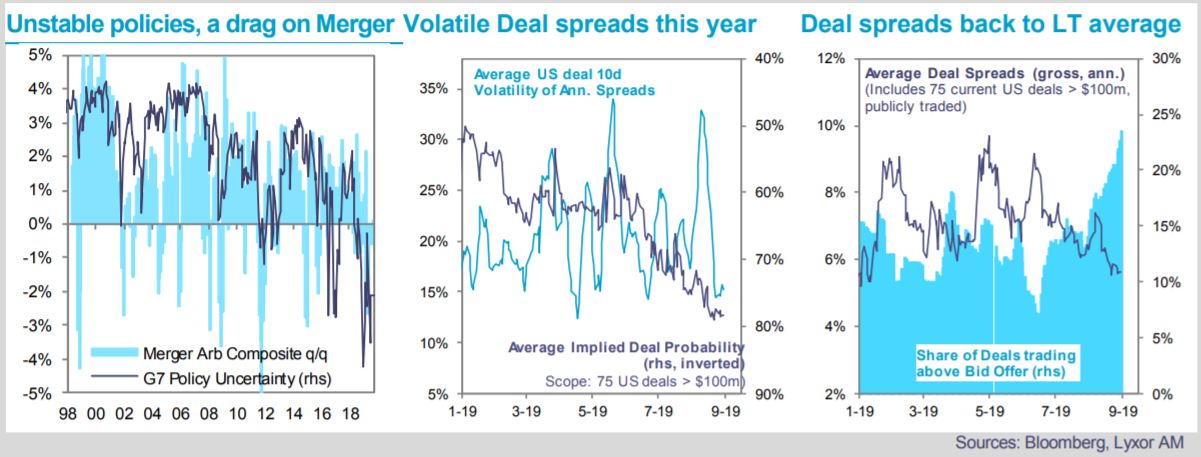

The Merger Arb. backdrop is attractive given its strong diversification patterns.Well isolated from market volatility, swings in fiscal/regulation/trade policies are however unsettling.

It contributed to moderate YTD returns (+1.5% on average). Volatility in deal spreads spiked, forcing managers to reduce exposures or take higher risks. Despite greater volatility, the risk of M&A break-up remained minimal (< 2% transactions failed), translating in elevated implied deal probability and contributing to compress merger spreads. The average gross spread of 75 live and large deals stands at 6%, close to the long-term average. With only few compelling bidding war situations and external flows from carry investors, the best deals were crowded, leading to several hits to merger portfolios this year.

The merger environment may seem currently “average”, but its returns-to-correlation profile outrank most other market segments. Its carry favorably compares with credit or dividend yield, the strategy also shows strong diversifying patterns in allocations and decorrelation from risky assets, with consistent alpha generation. We are O/W.

Lyxor Research , September 2019

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |