Hedge fund positioning after the storm

The positioning of CTAs and Global Macro strategies on equities remains very cautious at present. Meanwhile, long Fixed Income positions have increased over the past few weeks. The stance has thus turned more defensive, even though the outlook on EM assets has turned more constructive.

Article also available in :

English ![]() |

français

|

français ![]()

The market rebound started at end of December has taken place amid an easing of trade tensions and hopes that a no-deal Brexit will be avoided. A softer stance from major central banks has also been supportive. But preliminary manufacturing PMIs for January suggest that growth deceleration continues. At this stage, it looks like any shock to the euro area could tip the economy into a recession. In this fragile environment, we discuss hedge fund positioning and the extent to which the recent rebound in risk assets has led hedge funds to add risk in portfolios. In a nutshell, caution remains the keyword, as L/S Credit is one of the very few strategies which added risk during the sell-off.

The positioning of CTAs and Global Macro strategies on equities remains very cautious at present. Meanwhile, long Fixed Income positions have increased over the past few weeks. The stance has thus turned more defensive, even though the outlook on EM assets has turned more constructive. We see a lot of divergence in views on FX and commodities. Long USD exposures are now less consensual.

Merger Arbitrage strategies have been very selective in regard to allocating capital to recently announced deals. They nonetheless invested into some new deals, such as the Celgene vs. Bristol-Myers proposed merger. Merger Arbitrage strategies maintain a short duration bias in terms of deals’ expected completion to contain portfolio volatility.

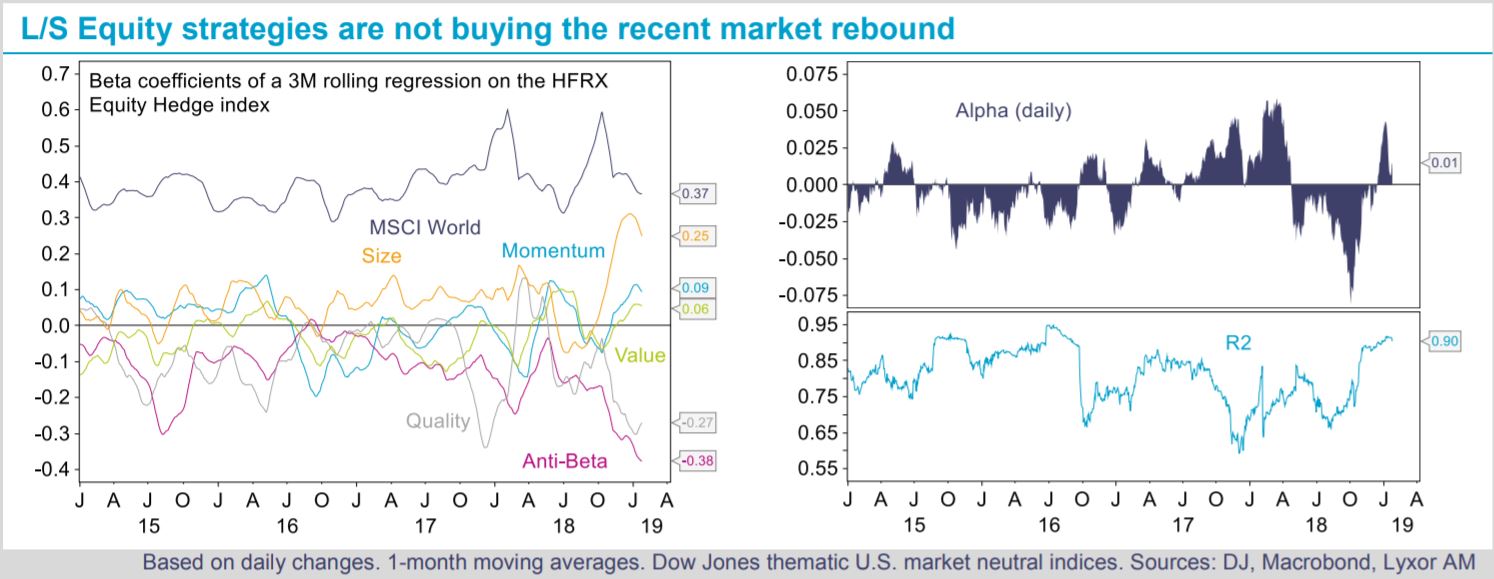

L/S Equity strategies reduced their beta in late 2018 and remain broadly cautious now. In Q4-18, they reduced gross and net exposures in a context where sector rotations were against their positioning (long cyclical vs. defensives). Market Neutral strategies, which tend to have a momentum bias, have also reshuffled their portfolios, turning short high-beta names and long low-beta stocks. The January market rebound, which was led by value stocks, still had a positive impact on L/S Equity performance overall.

Finally, L/S Credit strategies were among the very few to take advantage of deteriorated market conditions to add risk in portfolios in late December. The sharp widening in HY credit spreads was seen as an opportunity, and the strategy experienced a decent rebound in January, especially for directional strategies.

Lyxor Research , January 2019

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |