| https://www.next-finance.net/en | |

|

Strategy

|

Frontier markets: what’s in a name?

When considered on their own merits, and approached with the same care and due-diligence as any other emerging market investment, frontier markets can provide valuable diversification potential, says Franklin Adatsi, member of the Global Emerging Markets team at Jupiter Asset Management.

Article also available in :

English ![]() |

français

|

français ![]()

When considered on their own merits, and approached with the same care and due-diligence as any other emerging market investment, frontier markets can provide valuable diversification potential, says Franklin Adatsi, member of the Global Emerging Markets team at Jupiter Asset Management. “As emerging markets are buffeted by a strong dollar, falling commodity prices and growing uncertainty in China, diversification can prove particularly valuable”.

Frontier markets, by their very name, suggest a place on the edge of lawlessness, a wild west where only the most intrepid investor would dare set foot. This reputation is, in our view, largely undeserved, overshadowing some of what we consider the many positive characteristics of these markets: strong economic growth prospects, favourable demographics, healthy government balance sheets, good corporate governance and high corporate payout rates. In this context, frontier-market listed companies can form a valuable part of an emerging markets strategy.

Potentially attractive diversification benefits

The prospect of interest rate hikes in the U.S., coupled with a slowing Chinese economy, has shaken emerging market economies in recent months. In an era of rising systemic risks, the attractions of an emerging markets portfolio can be enhanced by diversifying the potential sources of alpha, and adding frontier exposure can be one way to go about this.

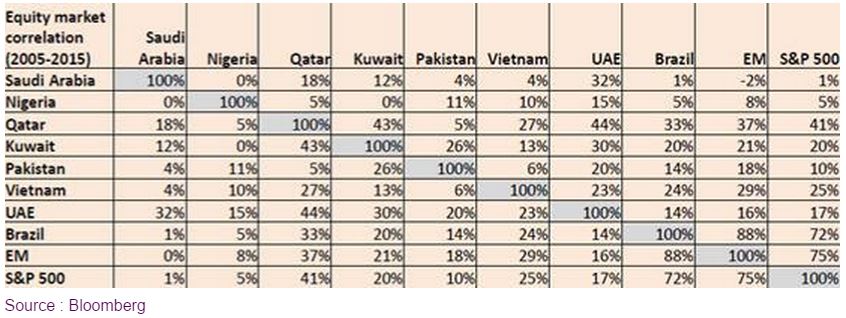

With low correlation to each other and to emerging markets (as shown by the table below), frontier markets can help diversify country risk, a major risk factor for emerging market portfolios. China, South Korea and Taiwan make up 50% of the MSCI Emerging Markets Index [1] and key non-Asian markets such as Brazil, Russia and Indonesia tend to be highly correlated with China and the emerging markets index. With the concentration of country risk and the high correlation between major emerging market country stock indices, seemingly isolated economic events in one country can create knock-on effects that can be felt more widely. Frontier markets, do of course, carry considerable risk, but crucially these tend to be more country-specific.

Shareholder friendly capital allocation

The risks conjured by the word “frontier” can often mean investors are surprised by the strength of underlying fundamentals in these markets, especially by levels of corporate governance. In many frontier markets, retail investors own meaningful proportions of company shares. Retail investors have strong political clout. As a result, regulators can be more effective in ensuring that the rights of minority shareholders are not abused and governments may be more sensitive to investor interests when considering capital allocation options for state controlled firms. For example, in several frontier markets in the Middle East, governments see the stock market and listed state owned enterprises as efficient vehicles for distributing wealth to the population. This alignment of interests is not typical in many emerging markets where state controlled firms are more likely undertake “national service” investments at the expense of minority shareholders. Furthermore, because retail investors appreciate receiving cash dividends to supplement their income, companies listed in frontier markets tend to be more willing to give back larger amounts of cash to shareholders. Shareholder friendly capital allocation has the potential to enhance long-term investment returns.

Strong structural reform potential

Structural reforms have the potential to enhance productivity and economic growth across emerging markets by improving competition in product and labour markets and creating a platform for a more dynamic and innovative economy. Based on our experience, stock markets generally react positively to countries that have the political capital and willingness to improve competiveness through effective structural reforms. India is a prime example that illustrates the potential of structural reforms to lift investor confidence. Within our investment universe, Saudi Arabia and Nigeria are two of the top candidates that we consider have immense potential to benefit from structural reforms over the medium-term.

Saudi Arabia - defying preconceptions

The Saudi market opened to foreign investors in June this year, and is not yet part of the MSCI Frontier index. However, the Saudi stock exchange is the largest and most liquid within the frontier universe. As a leading oil exporter, investors could be forgiven for thinking that the Saudi economy would be in the doldrums in the current environment of falling oil prices, but this in fact couldn’t be further from the truth. A hugely liquid market with a lot of company diversity, the Saudi stock market is currently trading at a significant premium to emerging markets, and has outperformed the MSCI emerging markets this year despite the significant drop in oil prices. (Source: Bloomberg) The Saudi government is implementing classic counter-cyclical fiscal policy. In the good times, the government paid down all of its national debt and saved a lot of money which is now being ploughed back into the economy. The government has also been trying to increase competitiveness by launching structural reforms. By liberalising laws to encourage women to work and encouraging companies to hire more Saudis (instead of expats), they have grown the workforce, boosting household incomes and improving productivity.

We own Saudi Telecom shares in our unconstrained emerging markets strategy. We believe Saudi Telecom has a strong competitive position and should be well placed to benefit from rising data consumption opportunities. A prime example of a state controlled company that has a history of allocating capital efficiently and returning excess capital to shareholders, Saudi Telecom has a cash-rich balance sheet and currently offers a 7% dividend yield (Source: Bloomberg), higher than any other dividend yield within the emerging market telecoms sector.

Nigeria- Time to shine?

We consider there is immense potential for positive change in Nigeria. Earlier this year, for the first time in the country’s history, an incumbent president was beaten at the ballot box. This is a major milestone for a country that has been plagued by political instability for decades. The new administration is focussed on fighting corruption, and a successful war on corruption could deliver immense benefits for Nigeria over the long-term. Nigeria is endowed with rich oil, gas and other natural resources but corruption has thrived at the expense of public welfare. As part of the war on corruption, we are likely to see structural reforms that improve transparency in the oil and gas industry and in public-sector finances. A climate of transparency and accountability can hopefully support the harnessing of greater national resources for needed investment in infrastructure, healthcare and education.

Nigeria is the largest economy in Africa. It has favourable demographics and the potential to sustain high economic growth rates. What has been lacking in Nigeria over the years has been good governance. The new administration’s commitment to good governance may represent a major catalyst that could provide confidence and stimulate long-term investment and accelerate the pace of economic growth. The market is now deeply concerned about the negative impact of low oil prices on the economy. In our view, market over reaction to falling oil prices is throwing up attractive investment opportunities. Supported by what we think are attractive valuation opportunities and prospects for structural reforms, we recently took a position in Access Bank which is well capitalized and at the early stages of generating returns from large investments in its retail franchise., The bank’s strong capital position and sound risk management practices should help it navigate credit risks arising from a low oil price environment. Access Bank trades on a price-to-book value multiple –(a measure of the market value of a company in relation to the equity capital invested in its operations ) - of 0.3x (Source: Bloomberg) , one of the lowest in our financials investment universe. It also currently offers a dividend yield of 10%.(Source: Bloomberg)

Frontier markets have the potential to generate attractive returns. But what of the risks? Individual country risks can indeed be considerable, and the smaller investment universe and lack of stock liquidity can be limiting. However, because frontier markets essentially expand our investable universe and because of their low correlation, we believe these investments could be highly complementary to enhancing the risk-reward characteristics of an emerging markets strategy.

Franklin Adatsi , September 2015

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] MSCI, August 2015

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |