| https://www.next-finance.net/en | |

|

Strategy

|

Five reasons why value will be back with a vengence

Mark Donovan, David PyleValue investors have had a rough ride over the past 18 months, but the tide may now be turning due to five major catalysts, says US fund manager Mark Donovan.

Article also available in :

English ![]() |

français

|

français ![]()

Speed read:

- Value stocks have fallen as investor seek ‘expensive defensives’

- Five catalysts from oil to earnings surprises are now emerging

- Large Caps are seen leading the reversal once sentiment changes

Amid fears over the global economy since the end of 2014, ‘expensive defensive’ and ‘glamorous growth’ stocks have been sought by investors seeking either perceived safety or higher earnings. The ‘sweet spot’ that is value stocks – those companies whose share prices do not fully reflect their earnings potential – has been largely shunned.

But better times may now lie ahead, particularly for the big established companies which are likely to lead earnings growth in the coming months and years, says Donovan, co-portfolio manager of the Robeco Boston Partners US Large Cap Equities fund.

As a long-time bottom-up value investor, Donovan follows the Boston Partners ‘three circles’ philosophy of only buying stocks which display the core value element, along with strong business fundamentals and momentum – where the company is deemed to be getting better rather than worse, and so can benefit from share price improvements.

Late-cycle market behavior

“The narrow, growth-driven market environment over the past 18 months has been inhospitable to our style of investing,” says Donovan, who manages the US Large Cap fund with David Pyle. “This is typical of late-cycle market behavior which often creates the conditions for a strong reversal, particularly in unloved areas. However, there are now several market catalysts that may precipitate such a reversal.”

Donovan sees five major catalysts that could now place the odds in value’s favor:

- A bottoming in the oil price: This has hit the US energy sector hard, with looming bankruptcies, capital expenditure cuts and layoffs, as oil fell from a peak of USD 130 a barrel in 2014 to as low as USD 26 in recent months. Now there is potential for supply cuts from OPEC and other non-OPEC nations to drive the price higher.

- Waning dollar strength: A strong greenback hurts US exporters and cost S&P companies USD 9 dollars in earnings per share in 2015 against an earnings base of approximately USD 118, according to Fundstrat. As dollar strength wanes, what was a headwind to companies reporting revenue growth will become a tailwind.

- Value differentials: Value/growth differentials are stretched at approximately1.5 to 2 standard deviation points from the mean, according to Empirical Research Partners data, and are not sustainable. This can clearly be seen in the valuation differentials of the likes of US large caps Facebook, Amazon, Netflix and Salesforce.com at 3.3x market averages at the end of 2015. A ‘reversion to the mean’ helps value stocks.

- US profit surprises. The very essence of value investing is picking those companies whose earnings are seen exceeding what is priced into their shares. Many ‘unloved’ value companies end up surprising on the upside, producing a premium for the fund. If economic growth can rebound from the low levels of the first quarter of 2016, there is will be considerable operating leverage that could drive earnings across many industries.

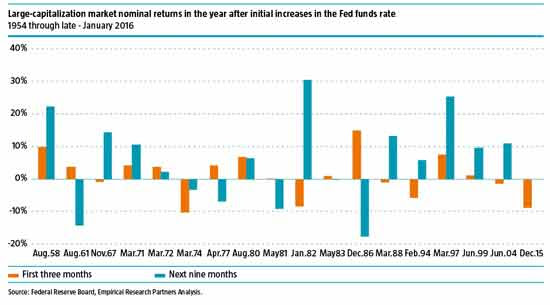

- Fed time lag: Markets typically rise following a three-month adjustment period to a policy move by the US central bank before they move. As the Fed raised rates in December 2015 for the first time in almost a decade, this suggests that the adjustment period will end around March or April (see chart below).

Present and future sentiment

The impact of a reversal in sentiment could be considerable, particularly as many of the market’s wobbles have been caused by exaggerated fears over a growth slowdown in China, a US recession, and even another financial crisis, Donovan says. “While growth expectations have undoubtedly been downsized, the worst fears rarely materialize, and there are counter arguments for many; the low oil price, for example, has benefits as well as drawbacks,” he says.

“As is often the case, short-term market action is driven by sentiment, which is responding very negatively to concerns of slowing global growth and the potential for an economic crisis. However, segments of the US market such as the banks, commodities and industrial companies are being valued as if there will be a significant recession. This is creating ‘three circle’ opportunities in Financials, Industrials and Energy that Boston Partners is selectively pursuing.”

Mark Donovan , April 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |