| https://www.next-finance.net/en | |

|

Strategy

|

Fed, Oil, yuan: towards a triple capitulation?

The first few days of the year were particularly challenging for capital markets. Further incertitude regarding the strength of the US cycle and the possibility that the Chinese economy is weathering a heavy depression drove risky assets lower, bucking the traditional early-year trend.

Article also available in :

English ![]() |

français

|

français ![]()

This context was symbolized by the fall in the oil price, which crystallizes all of the fears stemming from sluggish global trade and risk aversion.

Which factors could therefore trigger an inversion of the bearish market trend in which investors seem to see nothing but the glass as half-empty? Three key drivers could possibly inverse market sentiment over the relatively short term.

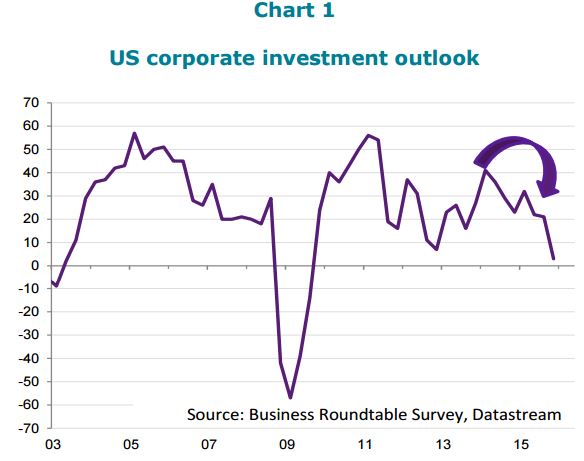

The Federal Reserve could acknowledge that the US cycle is less robust than expected. Despite persistent strength in the labour market, corporate investments are seriously struggling to take off (see chart).

The US cycle probably peaked in 2015, and the Fed should review its rate-tightening policy if economic indicators show further signs of weakness (in fact, the ISM Manufacturing Index continues to fall).

The Fed is, of course, refusing to take into account signals sent by Wall Street currently, and is being careful to dispel the idea that the stock market influences its policy. Indeed, the FED used the market to influence household mindset, over a period of several years, by maintaining a major wealth effect through unprecedented quantitative easing, which greatly fueled a strong rally in the equity market. For now, we prefer fixed-income assets, in anticipation of a more dovish tone from the Fed, but a shift back into equities could be considered, even if the market should benefit from fewer share buybacks.

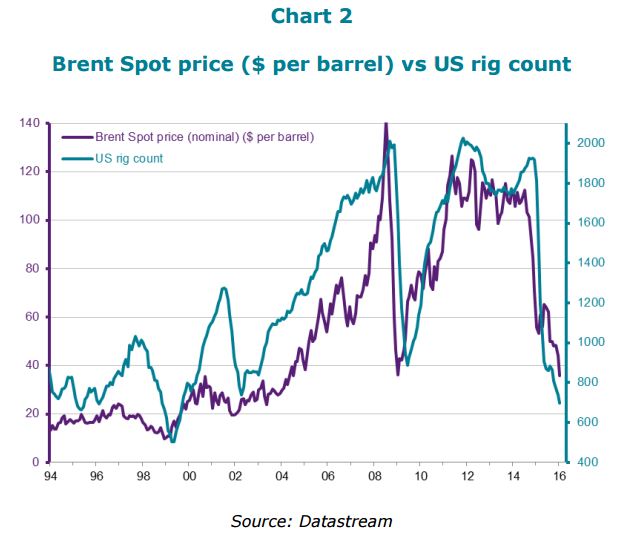

Concerning the oil price, the underlying trend should also be closely watched during the coming year for any potential turnaround. The overproduction strategy adopted by Saudi Arabia to undermine the profitability of US shale oil is currently a success. There has been a surge in high-yield defaults in the oil industry and the US banks will soon restrict their funding in this sector, which is seeing profitability and solvency nosedive. As a result, drilling and extraction projects in the US will slow down in line with the fall in the price of crude oil (see chart).

The risk of another subprime crisis in the US is limited, even though a large proportion of the (allegedly liquid) debt has been repackaged into the financial system as classic investment products.

However, oil-producing countries may now perceive the possibility of capping production and turn prices up again, even in a context of reduced global demand. Indeed, those very low prices strongly penalize countries whose budgets depend largely on income from the energy sector. Direct or indirect exposure (energy sector equities, oil-producing emerging markets countries, Canadian dollar and Norwegian krone, or even the break-even inflation rate in the US) could be built up progressively to capture the potential turnaround.

The third inversion will perhaps take place within the Chinese economy. If the economic climate continues to darken (see chart below: railway freight is often a reliable leading indicator for future growth), the authorities will not be able to drive growth indicators eternally and will have to implement some real measures. Supporting the yuan is proving to be a costly policy in terms of foreign currency reserves, with almost 20% of reserves evaporated since summer 2015.

Reinforcing currency controls would progressively squeeze China out of global trade and could worsen the credit crunch by preventing capital from entering the country. A more radical devaluation, on the other hand, would deteriorate domestic spending power, due to rising import prices, but would nonetheless open the door to implementing strong budgetary stimulus, without deepening the balance of payments deficit, as local investors would no longer have any reason to withdraw capital once the currency has adjusted.

Currently, we prefer to avoid all assets in the region (Asian equities, developed and emerging currencies, and especially credit). If such a shift takes place, it could rekindle the Chinese economy, which could then continue its transition towards a more domestic consumer-driven model.

These three potential shifts in policy, which could be implemented over the course of this year, clearly represent at least three solid reasons to believe that markets may yet post robust performances in 2016. Furthermore, the ECB’s accommodating policy will also remain a constant underlying support factor. However, 2016 yields will certainly be lower than preceding years. Interest rates are at a very low point and risky assets may need to correct some of their past excesses.

Franck Nicolas , February 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |