| https://www.next-finance.net/en | |

|

Strategy

|

ECB full QE

According to Jean François Robin, Analyst at Natixis, Considering that a EUR 500bn asset purchase programme was anticipated, one can expect a bull flattening and convergence trades (search for liquidity plus pooling, albeit partial) to predominate, while euro looks set to extend its decline whereas risky assets, especially equities, should benefit, probably even gold in the short term...

Article also available in :

English ![]() |

français

|

français ![]()

It’s a done deal, there will be a full QE in Eurozone, and it will be massive, with EUR 60bn of purchases each month on top of the upcoming targeted longer-term refinancing operations (TLTRO).

The European Central Bank (ECB) announced three measures:

(1) A full QE.

(2) A cut in the interest rate applicable to the next six TLTRO in line with the repo rate, i.e. 0.05%, which means that

the ECB has waived the 10bp spread over the MRO rate applied in the first two TLTRO.

(3) Repo rate kept on hold. After the decision by the Swiss National Bank and Danmarks Nationalbank, the ECB

confirmed it was not adjusting its own key monetary policy rate, which it considers to be at a floor. There were talks

the rate for the deposit facility could be raised to encourage banks to sell eligible assets to the ECB without being

penalised by being long cash. However, logically so, the decision was taken to maintain a negative rate, the intention

being to inject liquidity, but not for this liquidity to find its way back on the central bank’s balance sheet.

Of course, the most important measure was the decision to expand QE to include bonds issued by Eurozone central

governments, agencies and supranationals. In effect, QE was already under way through non-sterilised purchases of

covered bonds (CB) and asset-backed securities (ABS), also with the VLTRO (through the intermediary of the banks

and the carry generated by these operations).

About the size

Combined monthly purchases to amount to EUR 60bn (both private and public sector assets) from March until at least September 2016, i.e. EUR 1,140bn in total. This is more than the EUR 50bn that had been bandied about. Especially, this in addition to the liquidity that will be injected by the six TLTRO scheduled in 2015 and 2016. This means that the ECB’s balance sheet will be restored to its 2012 dimension and even more: around EUR 3.3trn (depending on assumption concerning demand at the TLTRO), which is a record for the ECB. This means that in terms of the size of the balance sheet in relation to GDP, the ECB’s QE at end-2016 will exceed the Federal Reserve’s (33% vs. a maximum of 26% for the Federal Reserve). The expansion of the balance sheet in relation to 2008 levels should be of the same order as for the Federal Reserve (i.e. an increase of between 10 and 11 points of GDP). Very importantly too, the press release states that purchases are intended to be carried out until at least September 2016 and “in any case until the Governing Council sees a sustained adjustment in the path of inflation that is consistent with its aim of achieving inflation rates below, but close to, 2% over the medium term”. This means that the ECB’s balance sheet could reach EUR 3trn, but possibly significantly more. While details are still awaited concerning the breakdown between asset classes the ECB has already indicated that the purchases of securities of European institutions would represent 12% of the additional asset purchases.

About the securities

In addition to CB and ABS, the ECB is expanding its purchases to include bonds issued by Eurozone central governments, agencies and European institutions (i.e. EFSF, ESM, EIB, EU, EBRD, etc.) but not corporate bonds.

To be eligible for the expanded asset purchase programme, securities must be denominated in euro and have a

credit rating of at least BBB- (best-credit assessment basis), with exceptions in the case of Member State under

financial assistance programmes. This signifies that, as indicated by Mario Draghi, the ECB should buy Portuguese

and, potentially, Greek bonds, but only from June of this year (as the central bank must wait for purchases made

under the SMP to reach maturity).

The ECB has indicated that index-linked bonds will be eligible for purchase under the expanded asset purchase

programme.

Securities must have a minimum remaining maturity of 2 years and a maximum remaining maturity of 30 years at the time of purchase (which had not necessarily been fully priced in by the market, as reflected by the significant bull flattening at the long end observed yesterday). The ECB will be able to buy securities offering negative yields.

About the process

In this case too, and as we announced, the ECB will proceed through purchases by national central banks (NCB)

applying the ECB capital key (see Market Round Up daily of 12 January: “In sum: the ECB can be expected to

announce an expansion of its asset purchase programme to other asset classes eligible as collateral, rated at least

Investment Grade. The bulk of these purchases should concern Eurozone sovereigns (for reasons to do with liquidity)

that would be acquired by NCB (under the umbrella of the ESCB) based on the ECB capital key”).

This means that ECB purchases will be confined to the secondary market, with the application of aggregate holding

limits, complying in this respect with the recent ECJ legal opinion that purchases must not distort prices in the

secondary market. In addition, to this end, the ECB has indicated it will be active in the repo market for bonds issued

by Eurozone central governments, agencies and certain European institutions. _ It has indicated that aggregate

holding limits will be 33% per issuer and 25% per line.

NCB will purchase most of the securities and all of the securities of European institutions (i.e. 12%), while the ECB

will hold 8% of the additional asset purchases (i.e. excluding CB and ABS).

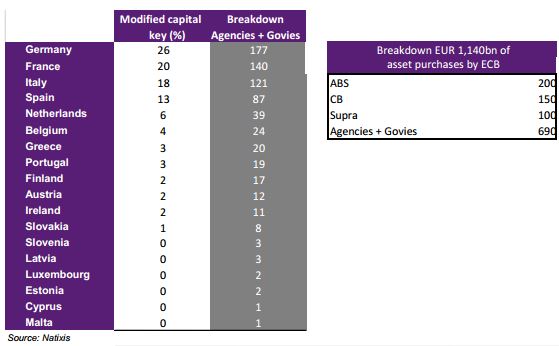

Based on the assumptions set out below for CB and ABS and assuming the programme totals EUR 1,140bn (i.e. EUR 60bn a month over 19 months) applied using the ECB capital key, this means that EUR 690bn of central

government and agency bonds will be purchased under the expanded asset purchase programme, with notably

EUR 177bn for Germany, EUR 140bn for France, etc.

Amounts are far from neutral if one considers that the bulk of the purchases will concern govies, when compared with amounts expected to be issued this year and, especially, net supply (EUR 2bn for Germany, EUR 97bn for France, etc.).

Risk sharing

With regard to the sharing of hypothetical losses, it was decided that, in the event of default, direct purchases by the ECB (8% of the additional asset purchases) as well as purchases of securities of European institutions (12% of the additional asset purchases) will be subject to loss sharing, i.e. borne by the ESCB (ECB plus NCB).

Other purchases will be carried on the balance sheets of each NCB. That was one of the big question marks, hence it was somewhat of a disappointment that the ECB should have given in to pressures from certain NCB governors (in particular Jens Weidmann) to have NCB bear most of the risk. At the same time, the ECB overcame this hurdle by explaining that this did not denote the absence of risk sharing since OMT are covered in their entirety by the ESCB. If there is an excessive widening of spreads, this would be addressed by the OMT programme, QE being intended solely as a monetary policy tool (and considered so apparently unanimously).

In the past, other monetary policy measures have drawn a distinction between national and European risks (ELA, Tier 1 vs. Tier 2 collateral). In the event of default, and pursuant to the conditions set out in the ECJ legal opinion, the pari passu principle would apply to the ECB (and/or NCB), which would be concerned by a credit event in the same way as any investor.

About the impact

The macro impact risks being limited (see Let’s get this party started). As regards the market, it would have been mainly the absence of major measures that would have been a real market mover. Considering that a EUR 500bn asset purchase programme was anticipated, one can expect a bull flattening and convergence trades (search for liquidity plus pooling, albeit partial) to predominate, while euro looks set to extend its decline whereas risky assets, especially equities, should benefit, probably even gold in the short term. Similarly for the short end, one can expect even more issues to slip into negative territory.

Jean François Robin , January 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |