Credit Strategy : Follow The Flow: No flows...no bull market

BofA Merrill Lynch Global Research highlights the importance of the peripheral trade (BTPs vs. Bunds) for the health of the credit market. Should peripheral spreads fail to rebound, BofA Merrill Lynch think that flows into credit will struggle going forward and so will returns.

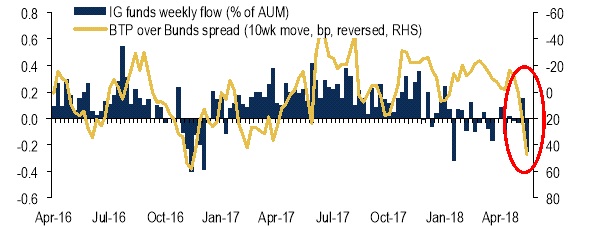

Fund flows weaken materially amid BTP sell-off

Politics are ruining the party it seems. All pockets of risk-assets we track have been hit last week. IG funds have recorded a sizable outflow as BTPs sold-off and currently are sitting above the 200bp handle over bunds. We have been highlighting the importance of the peripheral trade (BTPs vs. Bunds) for the health of the credit market. Should peripheral spreads fail to rebound, we think that flows into credit will struggle going forward and so will returns. Rates vol is critical, but so are peripheral spreads.

Without the return of inflows, the € credit market will be more susceptible to the rising number of event risks out there. Despite our optimistic view on European fundamentals and the cycle, without inflows, credit spreads will likely keep leaking wider for now.

Over the past week…

High grade fund flows reversed the positive inflow seen last week with the biggest outflow number seen in 17 weeks. The asset class have recorded outflows in 10 out of the 21 weeks YTD. However, the monthly number for April was positive. High yield funds continued to record outflows (28th consecutive week). Looking into the domicile breakdown, US and Globally-focussed funds have recorded big outflows. European-focussed funds recorded only a marginal outflow. Monthly data for April reveal that the HY space recorded outflows; however the outflow was the smallest YTD.

Government bond funds recorded outflows after two weeks of inflows. During the month of April, the asset class continued to see strong inflows, for the sixth consecutive month. All in all, Fixed Income fund flows were back in negative territory.

European equity funds continued to record outflows for the 11th consecutive week. The asset class is running towards a total YTD withdrawal of $9bn. The monthly data showed a deep outflow in the asset class last month - the largest since July 2016.

Global EM debt funds recorded an outflow, the fifth in a row, but much lighter than that of the week before. Commodity funds also recorded an outflow last week.

On the duration front, mid-term IG funds were hit the hardest; largest outflow in 8wks. Short-term and long-end funds recorded outflows, but to a much lesser extent.

Bank of America Merrill Lynch , May 2018

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |