| https://www.next-finance.net/en | |

|

Strategy

|

CTAs Shave Off Bond Exposures As Treasury Yields Rise

Fixed income markets have faced some pressures lately, as investors fret about less accommodative monetary conditions going forward. In addition, higher energy prices have fuelled bond yields, as both OPEC members and Russia...

Article also available in :

English ![]() |

français

|

français ![]()

Fixed income markets have faced some pressures lately, as investors fret about less accommodative monetary conditions going forward. In addition, higher energy prices have fuelled bond yields, as both OPEC members and Russia reiterated their willingness to find an agreement on an oil production freeze. Meanwhile, inflation rates have moved higher in September, as the energy component started to be less of a drag.

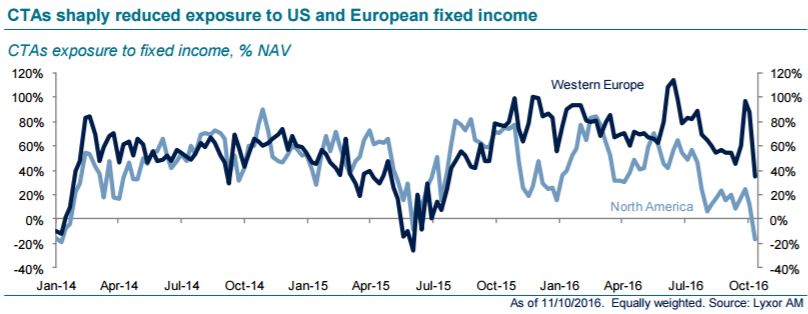

This upward trend in bond yields has led to a sharp adjustment of CTAs’ long exposures to fixed income. Trend followers have actually turned short duration on US fixed income according to our most recent available data. Meanwhile their long European fixed income exposure has been massively shaved off, from 87% of net assets to 24% in a single week (from October 4th to October 11th). In line with the more defensive positioning on fixed income, CTAs have increased their exposure to energy, from a short stance a few weeks ago to a long stance at present. It is important to note, however, that our aggregate positioning measure includes short term CTAs that adjust their positioning very swiftly.

Back in mid-September, we downgraded CTAs to neutral (from overweight) on the back of the long fixed income stance of the strategy which appeared to us as too aggressive. We also expressed a preference for short term models. This recommendation has worked well so far. The Lyxor Long Term CTA index is down 2% since September 20th while the Lyxor Short Term CTA index is down 0.6%. Meanwhile, the trend-following environment has continued to deteriorate according to the SG Trend indicator. As a result, it seems too early to re-weight the strategy but we stand ready to buy back.

With regards to other hedge fund strategies, there have been little changes to notice. Performance was flat across the board last week, though market neutral managers showed signs of revival, especially Asian managers.

Finally, flows into alternative UCITs continued at a sustained pace in September. Inflows into alternative UCITs jumped to EUR 7.5bn in Q3, up from EUR 2.8bn in Q2.

Lyxor Research , October 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |