| https://www.next-finance.net/en | |

|

Strategy

|

10-year yields for BTP, Bono and IGB at or below level for TNote: an anomaly?

Mario Draghi’s communication skills have proved exceptionally effective. Since the famous “whatever it takes” in 2012, yields for peripheral sovereign debts have converged sharply towards levels for German debt. Yields for BTPs, Bonos and IGBs sit at record lows.

Article also available in :

English ![]() |

français

|

français ![]()

One of the objectives of the measures announced last week by the European Central Bank (ECB) was to weaken the euro. At the moment, this appears to be working to plan: everything points to the single currency becoming a financing currency (the weak volatility in the foreign exchange markets is obviously propitious for carry trade strategies).

As regards sovereign debts, what is perhaps most startling is that the yield for the 10-year Bono is more or less level with that of the 10-year TNote, while the yield for the IGB is in fact lower than for the TNote and Gilt.

Italian, Spanish and Irish debts have been assigned triple-B ratings by S&P. By comparison US debt is rated AA+ and British debt AAA by this agency. Needless to say the liquidity of the US debt is nothing like the liquidity of the Eurozone’s peripheral debts, notably that of Irish debt, which offers the lowest yield.

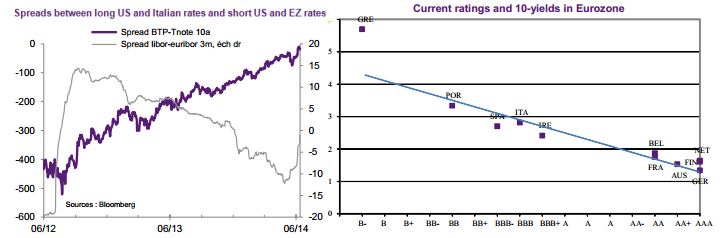

In the past, however, there have been similar episodes. The TNote-BTP spread has been positive on several occasions since 2000, in some cases for extended periods.

Until mid-2012, the spread between the TNote and BTP was relatively highly correlated to the spread between short US and EZ rates. Since then, however, these two spreads have clearly been negatively correlated. Everything is happening as if a “superior force” has suddenly gotten the better of this correlation. This “invisible hand” is obviously the threat of an intervention by the ECB, the market having been totally won over by the view that the central bank has the resources (and the resolve should this be necessary) to prop up Eurozone sovereign debts. Of course, this analysis also applies to Bonos and IGB.

The measures announced last week by the ECB are obviously not going to upset this phenomenon, on the contrary. However, the question is whether the protection now enjoyed by peripheral debts is not leading to a new mispricing. Contrary to what is often being said, this is not a certainty, at least not at this point in time. Before the sovereign debt crisis, the credit risk had just about vanished in the Eurozone, which clearly was an anomaly, as national debts in fact did not benefit from any protection at European level. Unless underlying fundamentals were good, there was no compelling reason for yields to be level with those offered by Bund. Yet this was the case. The credit risk reared its head once again with the crisis, with spreads against Bund still considerably wider than before 2008. Furthermore, sovereign debts now enjoy some protection in different, albeit imperfect guises. That is a big difference compared with the situation pre-crisis.

The curve charting ratings against yields has undergone a significant flattening, as underlined by the spread between the 10-year PGB and BTP, which has been divided by four since the start of the year, but once again the situation is a far cry from what it was pre-crisis when ratings failed to capture risks and the slope of this curve was near enough flat.

In short, right now, intra-EMU spreads are not aberrant (as yet). If one considers the TNote-Bund spread to be reasonable, then there is no major anomaly in the fact that yields for peripheral debts are less than or equal to yields for Gilts and TNotes.

There remains that, at global level, there is no one yield for a specific rating. One need look no further than yields for triple-A debts to see this, as the 10-year AGB yields 3.82% when the 10-year Bund yields only 1.38%...

René Defossez , June 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |