| https://www.next-finance.net/en | |

|

Strategy

|

Why Merger Arbitrage should continue to do well

To navigate such unstable conditions, there is a limited range of “all weather” strategies. Merger Arbitrage and Fixed Income Arbitrage (including L/S Credit) have demonstrated their ability to navigate such a difficult year like in 2018, when most asset classes delivered negative returns...

Article also available in :

English ![]() |

français

|

français ![]()

The market rebound since end of December is in stark contrast with the adverse conditions that prevailed in December for risk assets. In our view, the main reasons behind the turnaround are related to: i) a softer monetary policy stance from the Fed, which is likely to be confirmed at the January 29-30th FOMC meeting, ii) easing trade tensions between the U.S. and China, and iii) the announcement of economic stimulus measures in the latter. This suggests that the market recovery can continue in the short term. However, in our view, caution prevails in the medium-term, as recession risks in the U.S. and Europe have risen and Brexit uncertainty remains high.

To navigate such unstable conditions, there is a limited range of “all weather” strategies. Merger Arbitrage and Fixed Income Arbitrage (including L/S Credit) have demonstrated their ability to navigate such a difficult year like in 2018, when most asset classes delivered negative returns. We focus on Merger Arbitrage and why we think it could continue to do well in 2019, below are three main reasons:

- U.S. M&A activity has started 2019 with a bang. The announcement that Bristol-Myers Squibb is planning to acquire Celgene for 71bn USD boosted M&A volumes after a deceleration in Q4. It highlights the fact that the M&A wave in the health care industry remains unabated, offering opportunities for Merger Arbitrage managers to deploy capital and diversify portfolios. The recent 57bn USD Shire vs. Takeda merger contributed to fuel Merger Arbitrage returns in Q4 while markets were struggling.

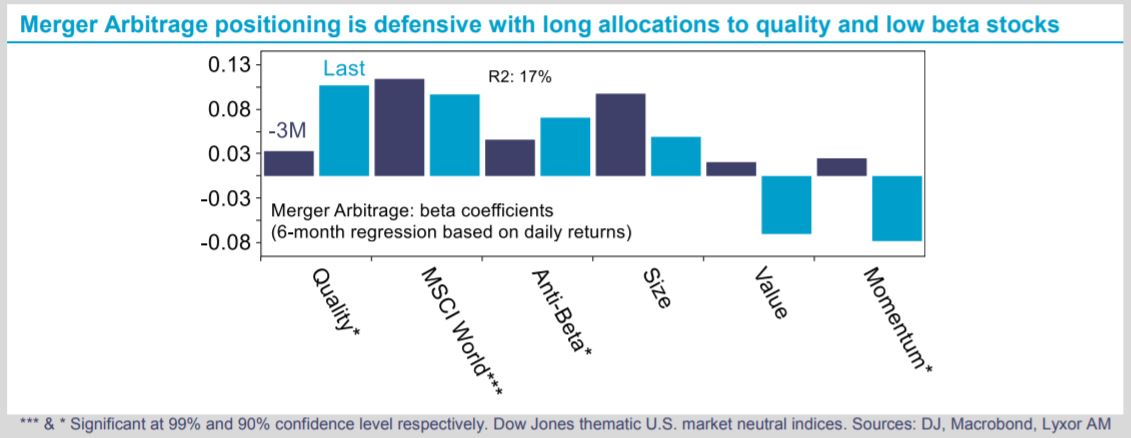

- The strategy is structurally defensive. Statistical analysis points to a low market beta (approximately 10%) and long allocations to quality and low beta stocks. It contrasts with L/S Equity strategies, which in aggregate have a higher beta (40%) and short allocations to both quality and low beta stocks. Historically, Merger Arbitrage strategies have proved to be extremely resilient when equity markets are in risk-off mode.

- Recent adverse market movements and new deal announcements led to a widening in deal spreads. They currently stand close to 7%, which is above the average since mid-2016. Deal spreads can nonetheless move rapidly, and current levels should rather be seen as an attractive entry point to reinforce the strategy in portfolios than a structural factor supporting the strategy.

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |