| https://www.next-finance.net/en | |

|

Strategy

|

Time to reinforce neutral fund allocations

We think it is time to strengthen L/S Neutral funds allocation. While they faced months of challenging transversal stock rotations, we expect their environment to improve for several reasons.

Article also available in :

English ![]() |

français

|

français ![]()

Regarding trade, markets had remained confident thus far before abruptly correcting this week as the U.S. moved against China. After 7 months of investigation, Trump announced tariffs on about 1300 Chinese products worth $50bn to $60bn (about 2% of Chinese exports), in tech, transport, health care – for which undue technology transfers from U.S. firms to Chinese ones are suspected the most. The U.S. will also file complaints against China in the WTO, and Chinese investments in the U.S. could face restrictions. While waiting for the Chinese response, the correction was broad, with the tech, healthcare sectors and key Asian suppliers’ markets leading on the way down. Financials also suffered in response to weaker yields. The impact was mild in commodities. The proportionality of the Chinese response could indicate how far both sides are willing to go. The broad exemptions finally granted on steel and aluminum seem reasonably encouraging. Hedge Funds were resilient, with the most diversifying strategies – CTAs, Merger and L/S Neutral funds taking the lead.

We think it is time to strengthen L/S Neutral funds allocation.

While they faced months of challenging transversal stock rotations, we expect their environment to improve for several reasons.

First, the peak in the economic momentum suggests that future stock rotations could be more macro/cyclical driven. These are easier to capture for quant and neutral funds.

Second, the return of volatility is a strong positive, the lack of which plagued the strategy for months while forcing to raise leverage.

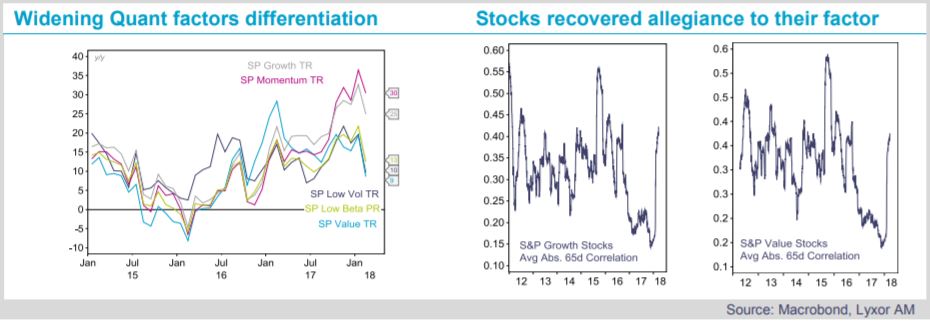

Third, “stocks’ loyalty” to their quant factors has returned. The correlation among stocks belonging to the same quant factor fully normalized. It suggests that quant stock-picking should become more reliable. Fourth, after moving in pack, the differentiation across quant factors is resuming.

Fifth, the lack of rationality, visible over the latest EPS season, between stock returns and the quality of their earnings, is unlikely to repeat.

This is an improvement for neutral strategies which tend to have a value bias.

Finally, we see more short opportunities, a noticeable improvement for neutral styles.

Jean-Baptiste Berthon , Philippe Ferreira , March 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |