| https://www.next-finance.net/en | |

|

Strategy

|

Stockpicking strategies remain in the driving seat

Market developments in May saw some trend reversals across the fixed income and commodity space. On the one hand, the unfolding of the Italian political crisis coincided with a rebound of U.S. Treasuries during the second half of May. On the other hand...

Article also available in :

English ![]() |

français

|

français ![]()

Market developments in May saw some trend reversals across the fixed income and commodity space. On the one hand, the unfolding of the Italian political crisis coincided with a rebound of U.S. Treasuries during the second half of May. On the other hand, the rising likelihood that OPEC and Russia will raise oil output under the pressure of the U.S. administration led to a reversal in oil prices.

Both developments hurt the performance of Macro and CTA strategies, which had built up short positions on Treasuries and long positions on oil over the recent quarters.

On a positive note, bottom up strategies (Event-Driven/ L/S Equity) have fared relatively better. They were up lately despite turbulent market conditions in Europe and to a lower extent in Japan. L/S Equity funds were more resilient thanks to their strong allocations to cyclical sectors such as IT and Materials and Industrials which outperformed. Meanwhile, their reduced exposures to financials, communications, and energy were also rewarding due to their underperformance.

On the Event-Driven side, long exposures to stocks such as Tiffany & Co. and Facebook generated substantial returns for special situations funds, while merger arbitrage strategies benefitted from the spread compression on the Qualcomm vs. NXP deal. More recently, the bidding war for Sky between Fox and Comcast was also supportive.

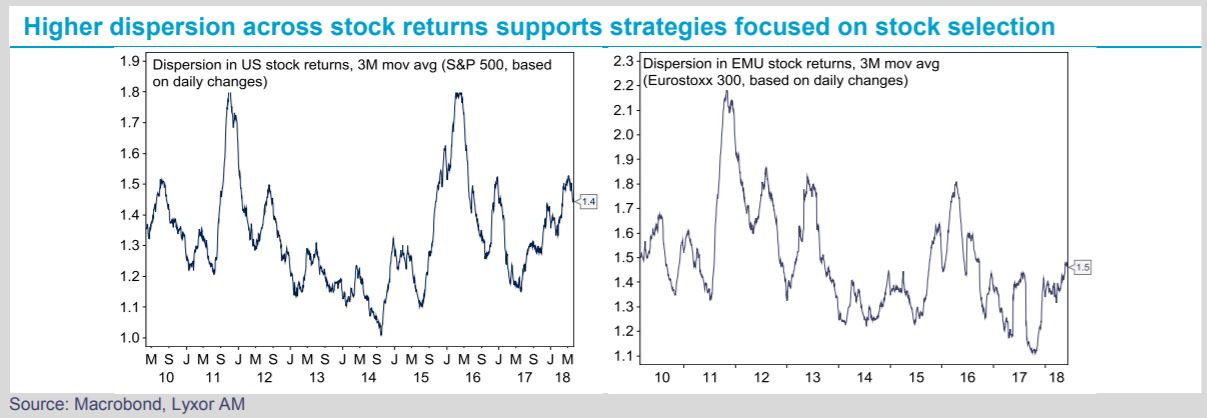

Going forward, we maintain a preference for stockpicking strategies. L/S Equity appears well equipped to navigate turbulent markets and we have a strong preference for strategies with a variable bias that can adjust their net exposure to fast changing market conditions. Meanwhile, we maintain strong convictions on Merger Arbitrage, in the context of the U.S. fiscal reform and skyrocketing M&A activity in 2018. Overall, monetary tightening and the rise in bond yields have pushed higher the dispersion across stock returns both in the euro area and the U.S. which should prove supportive for hedge fund strategies focused on stock selection.

Lyxor Research , June 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |