| https://www.next-finance.net/en | |

|

Interview

|

Simon Bond : “Our European Social Bond Fund is carefully managed with a mix of maturities to offer daily liquidity”

According to Simon Bond, Threadneedle (Lux) European Social Bond Fund manager, the fund aims to balance three key elements: clear social impact, daily liquidity and financial return with a similar risk/return profile as a regular investment grade fund...

Article also available in :

English ![]() |

français

|

français ![]()

Next-Finance : You invest in Investment Grade bonds, while associating a social dimension directly related to the securities selected in the portfolio. Could you remind us the principles of a social bond (versus green bond)?

Simon Bond: A social bond is a bond issued to fund social projects that have a positive impact on individuals, communities and society. For example, the money collected could be used to facilitate access to affordable housing, support health, employment and education. These products are therefore different from the Green bonds that aim to finance the energy transition. It is important to note that this is not philanthropy. Our objective is to unlock the full potential of bonds to deliver both financial returns and positive social outcomes. The fund aims to balance three key elements: clear social impact, daily liquidity and financial return with a similar risk/return profile as a regular investment grade fund.

Is your investment universe sufficiently broad and diversified? Do you have a benchmark?

Yes, I think so even though I would like it to be broader and more diversified. That’s why I spend a lot of time trying to convince issuers to get into this market.

In the last few years, we have encouraged governments, supranationals, and charities to consider issuing social bonds for socially beneficial projects.

Out of 4 286 European corporate bonds in the market, we have identified that approximately 43% are social in nature across different sectors and countries. By actively selecting specific bonds with positive social outcomes, rather than excluding bonds through conventional negative screens, we aim to generate positive social and financial results.

For our benchmark, we use a composite index : 50% Bank of America Merrill Lynch Euro Non Sovereign Index + 50% Bank of America Merrill Lynch Euro Corp Euroland Issuers Index.

In your opinion, it is the right time to discuss with governments how they could they also issue social bonds, in line with the United Nations Sustainable Development Goals (SDG)... Can we see in the near future, a market for sovereign social bonds? What is necessary for this market to take off?

Yes, absolutely even if it is not the case today. Governments can benefit from private investments to finance social projects. Stable, long-term financing for organisations operating in areas of social need is critical. But following the global financial crisis, many socially-focused sectors are finding traditional sources of funding less attractive and less plentiful. Some are suffering from years of chronic under investment. Social bonds help bridge this gap by matching investor capital to projects with a defined positive social outcome.

Indeed, we have reported this subject to the ICMA (International Capital Market Association) which lead to the publication in June 2017 of the Social Bond Principles and Sustainable Bond Guidelines, a voluntary framework for good practice around guidelines, transparency and disclosure, similar to the Green Bond Principles.

Since the fund launch, there have been two significant milestones in the growth of the market.

1) 14 November 2017 was a seminal day in the development of the market, with an unprecedented number of specific use-of-proceeds bonds being issued in Europe. Hot on the heels of Black Friday and Cyber Monday we christened it "Social Tuesday"!

2) A key development in the social bond market came in March 2018, with the launch of the first corporate social bond by Danone. It will focus significantly on funding the advanced medical nutrition business, supporting research and development.

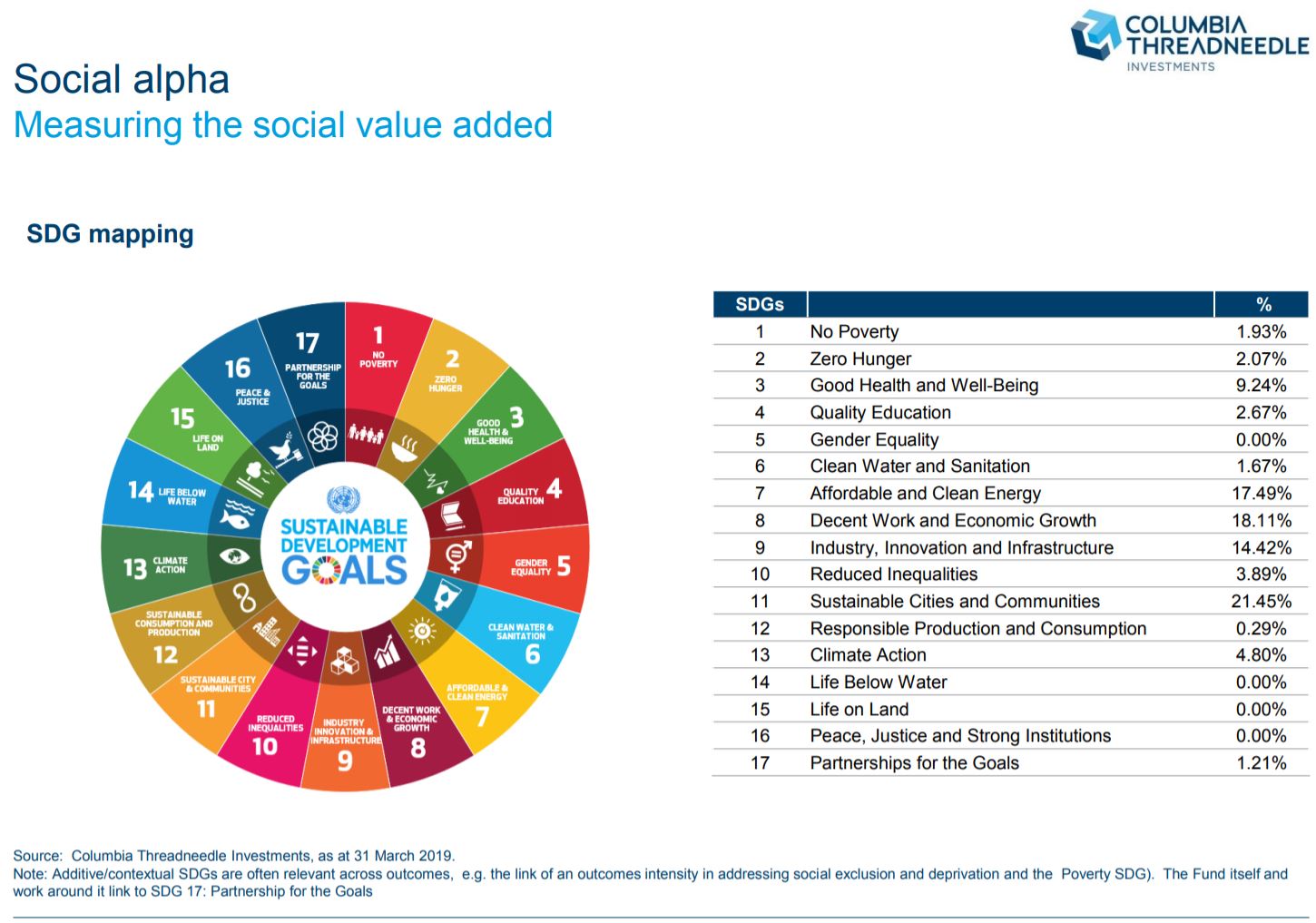

Regarding the SDGs, I would like to add that each of our investments has been made according to criteria aligned to the SDGs, as you can see below.

Can you tell us more about the partnership with INCO?

INCO is an investment organisation specializing in companies with a strong social and environmental impact. Thanks to its expertise and independence, its role is to advise us about the assessment of the social impact of the bonds subscribed in the Threadneedle (Lux) European Social Bond Fund portfolio. INCO publishes an Annual Social Impact Report for the fund.

The fund was launched in 2017, what are your assets currently? What is its maximum capacity?

Strategy outstanding assets are approximately 408 million dollars, including mandates, with a capacity of $ 2 billion at the time I am speaking to you. But if the market of Social Bonds is going to grow, of course this limit will be revised upwards.

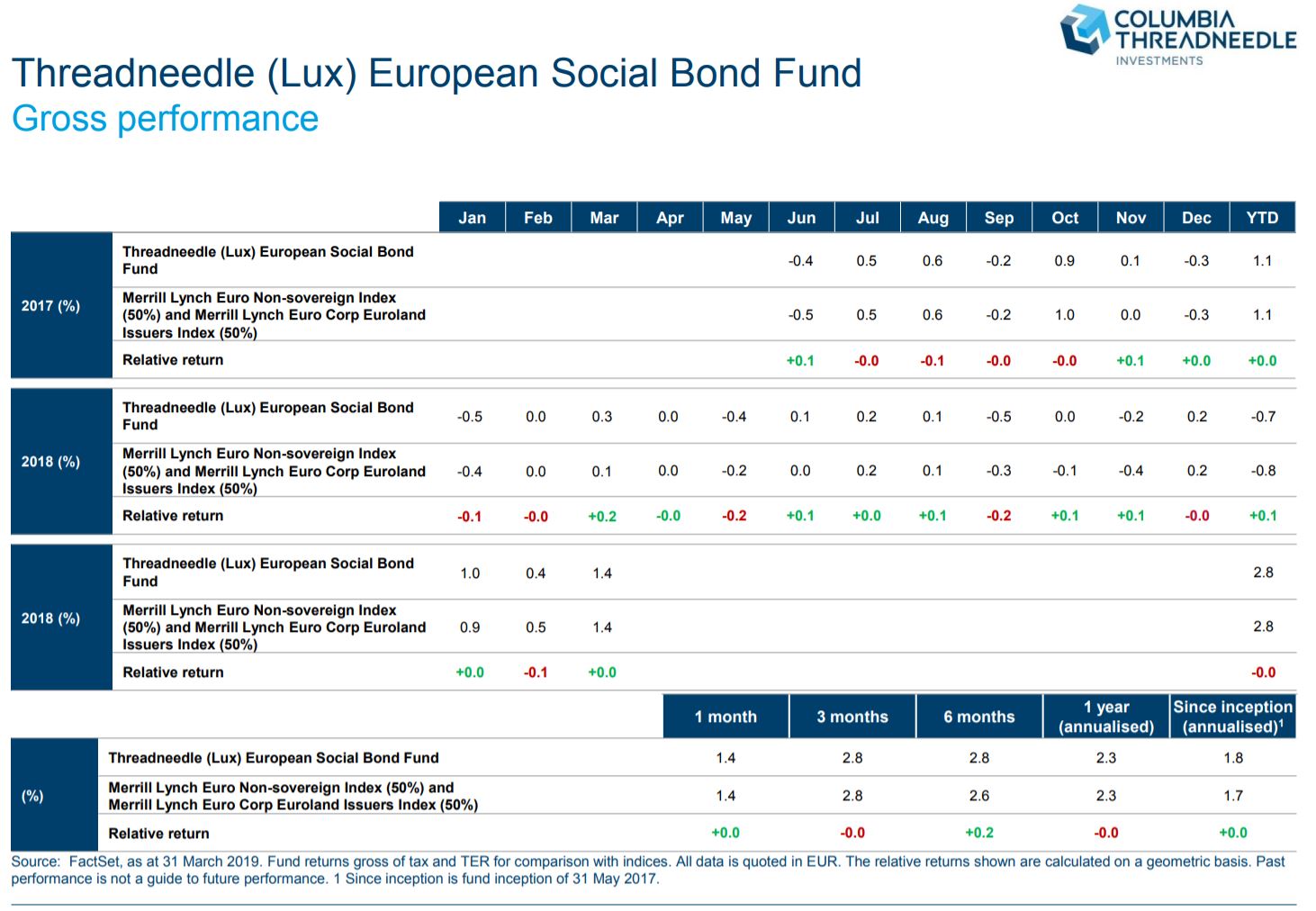

What about the performance since inception ? Beyond performance, do you report annually on the overall social impact of your fund?

We have managed outcomes-focused social bond strategies for over five years and have delivered strong risk-adjusted returns for our investors.

Since its inception, the European fund’s annualized return has been 1.8%, with a very low level of volatility as its Sharpe ratio is around 1 over the period.

With regards to the overall social impact, INCO analyses the impact and publishes an annual impact report. In addition, we continually analyse the social intensity of each individual bond in the portfolio according to our proprietary metholodology aligned with the SDGs.

Finally, the fund has been awarded the ESG label by the Luxembourg Finance Labelling Agency (LuxFLAG).

What type of investors are interested in your fund ?

As a consequence, all types of investors are interested in our product: from private individuals to leading investors such as pension funds and insurance companies.

The fund is carefully managed with a mix of maturities to offer daily liquidity. Frequently, impact investment and other social impact vehicles must tie up money for long periods. Furthermore, the risk profile can be challenging to understand. The European Social Bond Strategy, by contrast, offers a corporate bond strategy type risk and aims for a corporate bond return, making it accessible and understandable to a wide range of investors.

Paul Monthe , RF , May 2019

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Interview Isabelle Bourcier : “Our ambitions is to grow in Smart Beta and SRI ETFs”

Evolution of the ETF market, impact of the regulations, ongoing development at BNP Paribas Asset Management...Isabelle Bourcier, Head of quantitative and index management at BNP Paribas Asset Management shares its view with (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |