| https://www.next-finance.net/en | |

|

Strategy

|

Real money, real risk

“A billion here, a billion there, and pretty soon you’re talking real money.” Used for decades to describe the perceived high and ever-increasing level of government expenditures, this memorable phrase of unclear origin may also offer insight for those building investment portfolios today. Consider a slightly modified version: Potential loss here, potential loss there, and pretty soon you’re talking real Risk, with a capital “R”.

Article also available in :

English ![]() |

français

|

français ![]()

In reviewing the primary options available for investment – stocks, bonds and cash – noticing that each has its problems is unfortunately the easy part of the analysis. Stock P/E ratios have expanded dramatically over the past six years, reaching levels unseen for quite some time and exposing investors to any reversal in underlying confidence. Bond yields have fallen to extraordinarily low levels in nominal terms, thus presenting investors with the possibility of negative real returns should inflation or credit quality prove problematic down the line. Cash returns nothing today – as discussed in a prior Outlook – and similar to bonds, holds the prospect of lagging inflation over time. There is also real estate, which for many investors means their house. While home prices may not be out of line with long-term historical valuation parameters, most homeowners have learned the lesson that house prices can in fact decline, so yes, there is risk in this asset class too. In total, it seems the investment landscape today holds plenty of risk.

Beyond the bedrock approach of buying cheap assets, diversification can be of great assistance in building a strong portfolio, one with ample expected return but not too much risk. In theory, when one asset price zigs, another may zag. By combining assets with differing return and risk profiles, the characteristics of a portfolio may be superior to its individual components.

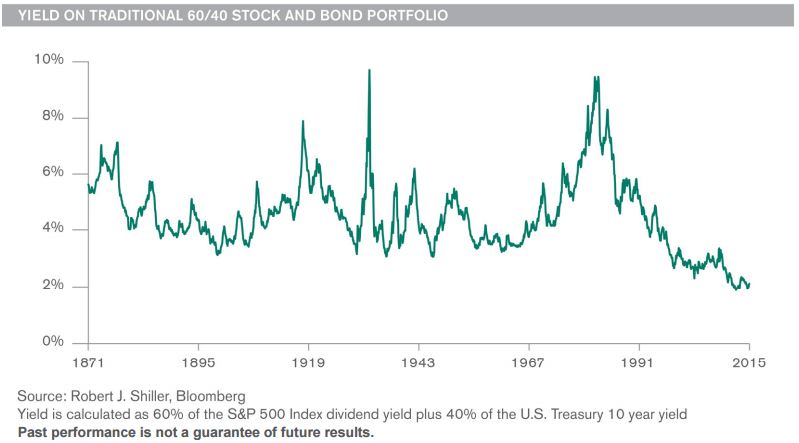

In practice today, however, the yield on a traditional 60/40 stock and bond portfolio is at a 100+ year low. Both asset classes are expensive, leaving an investor little to work with in the way of portfolio building blocks. Worse yet is the uncomfortable possibility that the correlation between stocks and bonds may become high should the mood of the markets darken, and thus mute the potential benefits of diversification.

In the realm of equities – our focus at Perkins – risk can sneak up on you, in a way. In a bullish environment, an investor may assess her portfolio as consisting of a pharmaceutical company with a potential blockbuster in the pipeline, a cable television operator which may participate in a merger boom, and a world-class industrial manufacturer focused on efficiency gains to drive its margins higher. In a less optimistic setting, the same investor may feel she owns a drug company facing pricing pressure, an old media provider grappling with cord-cutting, and a cyclical industrial firm earning peak margins with nowhere to go but lower. Further, it is when in this more pessimistic mood that she will recognize that in addition to a number of serious company-specific or perhaps industry-level risks embedded in the portfolio, the correlation among these risks is frighteningly high. For example, the drug pipeline optimism seems to fade at the same time as media M&A activity declines and industrial production rolls over.

The seemingly natural tendency to recognize risk here, risk there, risk everywhere in a stock portfolio – during and after a sizable drawdown in the market – is something to avoid at all costs. One must try to recognize and avoid/manage the risks in advance.

As our benchmarks keep setting new highs, our investment team keeps an account of the risks which are accruing. Our analysts model an explicit downside scenario for every stock under consideration. This discipline helps us identify risks, even during a bullish phase in the market.

We are especially leery of cyclically high sales and profit margins, as well as valuation multiples stretched by the demand for dividend yield. Conversely, we like companies which may benefit from “self help,” such as lowering operating expenses or refinancing high-cost debt. We also favor earnings streams which are tied to repeat purchases unlikely to change as a result of fluctuations in the economy, as we believe these stocks are relatively less likely to be subject to a weakening of market confidence.

Our portfolio managers are aiming for a thoughtful degree of diversification, not just in sector classification or geographic region but by underlying drivers of the cash flows, book values and valuations of our holdings. We are always on the lookout for that which is out of favor and unloved – even today there are examples of this “meat and potatoes” of value investing – and in its absence hold quality in high regard.

Gregory Kolb , July 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |