| https://www.next-finance.net/en | |

|

Strategy

|

Re-weighting carry strategies

In a context where monetary conditions are more accommodative and sovereign bond yields are back to low levels, it seems appropriate to re-weight carry strategies such as EM-focused Global Macro and L/S Credit.

Article also available in :

English ![]() |

français

|

français ![]()

Throughout 2018, our investment views on alternative strategies shifted in favor of low beta strategies as risks were tilted to the upside. However, in early 2019 the Federal Reserve reversed the policy normalization course, and economic growth may have stabilized. The balance of risks is thus less adverse despite the political uncertainty. The likelihood of an escalating U.S./China trade war and a no-deal Brexit has probably decreased but has not vanished.

In a context where monetary conditions are more accommodative and sovereign bond yields are back to low levels, it seems appropriate to re-weight carry strategies such as EM-focused Global Macro and L/S Credit. The views on these alternative strategies are aligned with our recommendations on traditional asset classes. We suggest an overweight stance on High Yield (in USD and in Euro) and EM sovereign credit. Specialized alternative managers in those asset classes tend to have a long bias which implies that spread tightening, as we expect, would be as a tailwind.

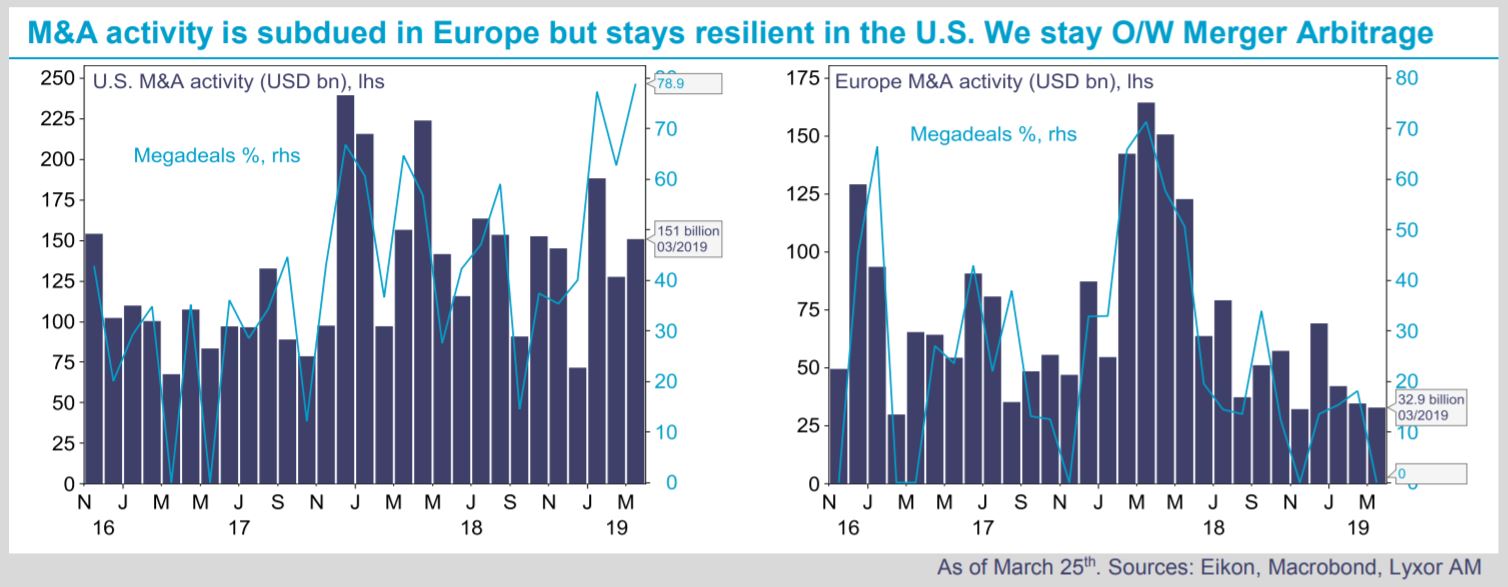

Overall, we maintain a preference for Event-Driven vs. L/S Equity; and a preference for Fixed Income Arbitrage (including L/S Credit) vs. Global Macro and CTA, with some readjustments at the level of sub-strategies. We keep an OW stance on Merger Arbitrage, which offers a low correlation to equities and a low volatility in returns. Global M&A volumes are down (-30% YTD - as of March 25th - vs. Q1-18) but remain stable in the U.S. where the share of megadeals is significant. Deal spreads have decreased in Q1 but they tend to be volatile and are of little help to formulate midterm views. The strategy is also an attractive hedge if things go wrong (Brexit, global growth slowdown).

We also remain OW on Fixed Income Arbitrage. However, within the strategy we downgrade sovereign Fixed Income, that is less attractive as implied volatility is likely to be tamed by the Fed’s bond purchases, in favour of L/S Credit strategies.

Finally, we re-weight L/S Equity long bias to capture the market beta in an environment which is likely to be more supportive of risk assets. Historically, alpha generation by hedge funds has proved difficult when QE programmes compressed risk premia across asset classes and dispersion within asset classes. However, in 2019 the Fed will not expand its balance sheet, it will just stabilize it. The implications for hedge fund performance should be less significant.

In terms of recent performance, our UCITS peer groups point to an outperformance of CTAs and Special Situation strategies month-to-date (+1.7% and +1.3%, respectively) and an underperformance of L/S Equity Market Neutral (-0.1%).

On a year-to-date basis, Directional L/S Equity, Special Situation, and EM-focused Global Macro strategies are up close to, or above, +4%.

Lyxor Research , March 2019

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |