| https://www.next-finance.net/en | |

|

Opinion

|

Perspectives on L/S Equity strategies after the Selloff

Risk assets have yet to find stable ground after the recent turmoil. The rebound in equities since the October 11th trough appears fragile. Last week, the minutes of the latest FOMC meeting were hawkish and Italy’s 10-year sovereign spread with Germany jumped to levels unseen since the eurozone sovereign crisis.

Article also available in :

English ![]() |

français

|

français ![]()

Diversified investors will find some comfort as bonds yields stabilized. In the medium-term, we stay constructive and argue that U.S. equities offer entry points at current levels.

Hedge fund performance was flat last week (from October 10th – October 17th) and L/S Equity strategies outperformed according to liquid benchmarks. The strategy captured the rebound that others, such as CTAs, did not because of systematic deleveraging. Broader measures of performance also point to L/S Equity outperformance year-to-date (up to end-September) versus an overall industry benchmark.

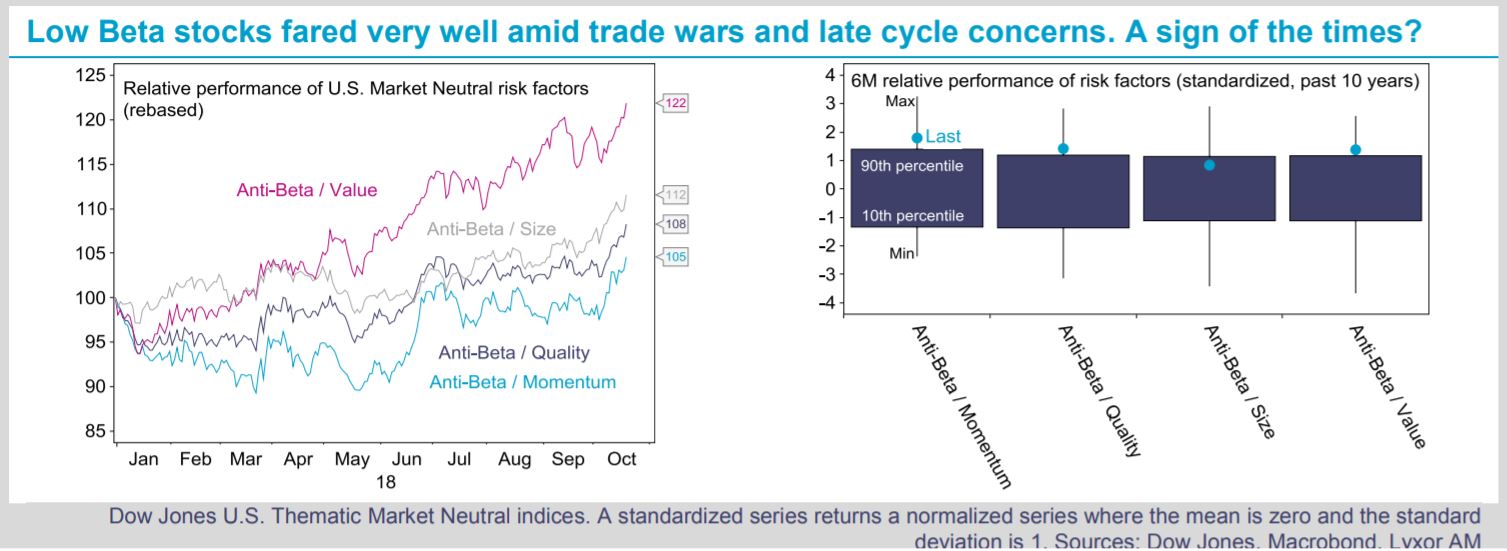

Yet, it has been a difficult year for L/S Equity strategies so far. Alpha generation has lagged most prior years amid risk factor rotations which saw low beta stocks outperforming. Recently, value stocks also staged a rebound and momentum stocks were under pressure. From a regional perspective, U.S. L/S Equity strategies faced difficulties due to their bias towards growth/ momentum stocks which suffered lately. European L/S strategies fared better as they have lower style biases and lower net exposure than U.S. peers. Market Neutral L/S strategies fared slightly better month-to-date but, at the difference of diversified L/S Equity strategies (i.e. non-market neutral), they did not rebound since the trough.

Going forward, a few remarks deserve attention regarding equity risk factors. First, we do not believe in a sustainable rebound of value stocks at this stage of the economic cycle. Second, we still believe in growth/technology stocks on the back of the assumption that bond yields have limited upside room from here. Third low beta stocks make a lot of sense at this stage of the business cycle where U.S. overheating fears may give way to recession fears in the coming months. When such views are applied to L/S Equity strategies, they suggest a preference for variable biased strategies that can adjust their net exposure down or up quickly.

Investors should also favor strategies that are tactical and less biased towards risk factors.

Lyxor Research , October 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |