| https://www.next-finance.net/en | |

|

Strategy

|

Our take on opposite Macro/CTA views on bonds

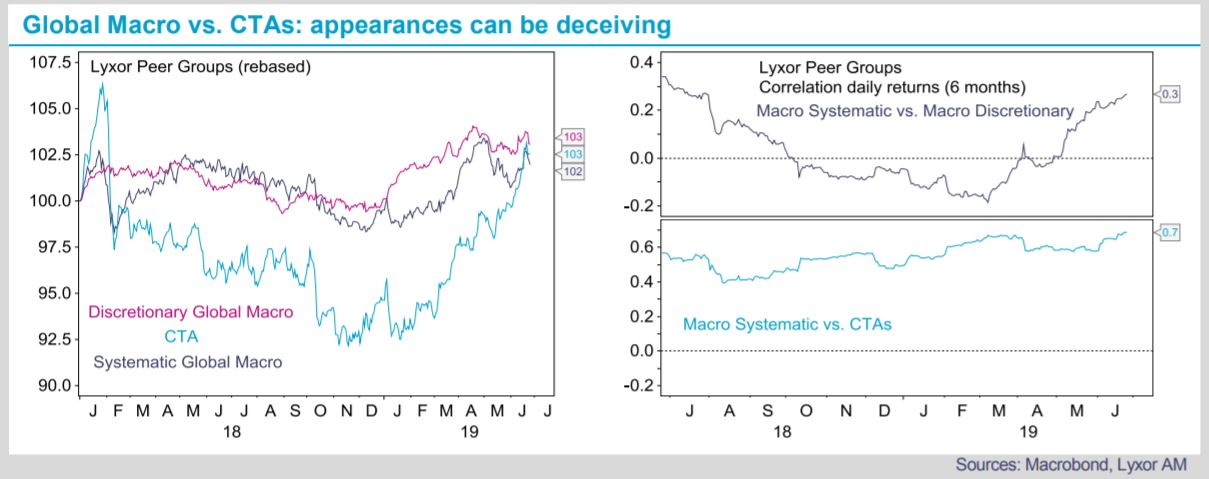

Systematic Global Macro and CTAs are often associated because many strategies are multi-asset, global, and have a top down investment process. Benchmark indices tend to pool them together.

Article also available in :

English ![]() |

français

|

français ![]()

Systematic Macro and CTAs are also appreciated for their diversification ability and have a good track record throughout bad times, when risk assets experienced sharp and protracted drawdowns. Yet, we argue that both strategies are quite different.

Performance between Systematic Macro and CTA strategies was comparable over the past 18 months (+2-3%) according to Lyxor UCITS Peer Groups. Concurrently, the 6-month correlation of daily returns between CTA and Systematic Macro strategies is as high at 0.7 at present (0.3 between CTAs and Discretionary Global Macro). From this perspective, they have common factors. Yet, their volatility is nonetheless contrasted. We estimate that CTAs’ return volatility was 6% (annualized) over the past twelve months, while Systematic Macro’s volatility was much lower, at 3.6%.

In terms of positioning, there are also substantial differences between them. The strong trend in bond prices since September 2018 has led CTAs to accumulate elevated net long positions on fixed income, especially in Europe. In turn, driven by fundamental inputs, Systematic Macro strategies expect a rise in bond yields and have accumulated net short positions on bonds. If monetary policy accommodation boosts growth and inflation expectations, this would steepen yield curves and push bond yields higher. Global Macro strategies are positioned to benefit from this outcome, while CTAs would suffer from such development.

Our preference for CTAs vs. Systematic Global Macro was rewarding in Q2. Going forward, we maintain this preference, but we are concerned about potential trend reversals in fixed income. Bond yields have reached very low levels, particularly in Europe. The bleak macro picture does not suggest they should rise materially and sustainably in the short to medium term. But even a modest repricing in bond yields would hurt CTAs, which hold sizeable long exposures. As such, we maintain the preference for CTAs but argue that recent performance could be seen as a reason to take some profits and rebalance towards Systematic Macro strategies to protect portfolios against a potential rise in bond yields.

Lyxor Research , July 2019

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |