| https://www.next-finance.net/en | |

|

Strategy

|

Not the start of a bear market

According to Mohit kumar, Global Head of Rates Strategy, Crédit Agricole CIB, thus a rate sell-off from current levels becomes self-defeating. If rates sell-off further, it would trigger a sell-off in risky assets which would in-turn create a bid for fixed income.

Article also available in :

English ![]() |

français

|

français ![]()

Fixed Income market globally has been selling off since beginning of the year, with 10Y US Treasuries (USTs) and 10Y Bunds yields higher by nearly 50bp and 30bp respectively. The move has been driven by a number of factors 1) expected shift in central bank policies 2) beginning of year portfolio flows and the return of supply 3) better economic data.

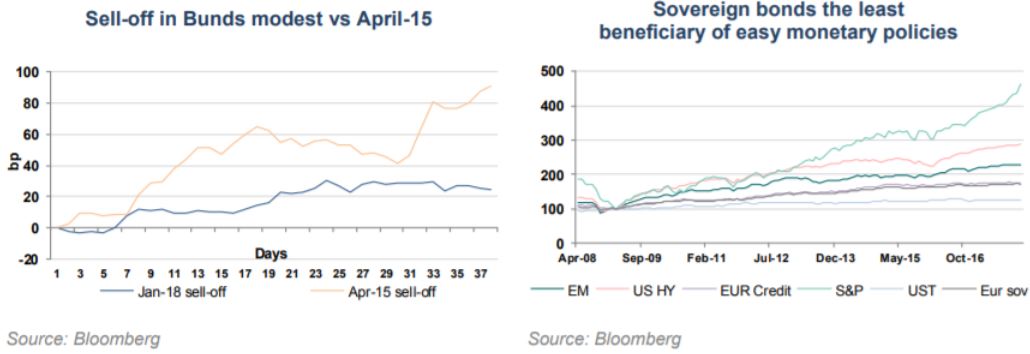

Even though the sell-off appears aggressive, it is relatively modest versus previous episodes. 10Y USTs moved by nearly 80bp in the month following US presidential elections in 2016 and by nearly 135bp around the taper tantrum. Similarly 10Y Bunds had sold off by nearly 90bp in April-15 which was driven by position squaring rather than macro factors. In all the above cases, the sell-off did not last long and eventually reversed.

Despite the recent sell-off, valuations for both the US and the European markets are not stretched. Our risk premium metric (which compares bond yields versus long term expectations of growth and inflation) suggests that the fair value range for 10Y USTs is 2.05% to 2.80% and that for 10Y Bunds is 25bp to 75bp.

Currently we have moved to the upper end of the fair value range both in the US and in Germany. While valuations may not be stretched, as rates move to the upper end of the fair value range, the sensitivity of risky assets to the level of rates should increase.

To gauge the sensitivity of risky assets to a move in rates, we can use a risk premium framework. Conventional measures of valuing equities would suggest that equities are over-valued. However, when valued vs rates (equity yield – real bond yield), equity risk premium does not appear in a bubble territory, suggesting that risky assets are supported only as long as rates continue to remain low.

We would argue that risky assets are more sensitive to a shift in central bank policies than rates. Using a simplistic framework for central bank policy impact, we compare the asset price evolution since the start of the easy monetary policy.

On a comparative basis, we find that rates have benefited the least from the easy monetary policies. Equities, EM and HY have been the largest beneficiaries of the support from central banks.

As the supportive policies are withdrawn, one would expect that the asset price evolution to be in exactly the same order i.e. Equities, EM and HY would be much more vulnerable to a rate sell-off than the sovereign bond market.

Thus a rate sell-off from current levels becomes self-defeating. If rates sell-off further, it would trigger a sell-off in risky assets which would in-turn create a bid for fixed income.

Mohit Kumar , March 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |