| https://www.next-finance.net/en | |

|

Strategy

|

No news is good news for markets

The old phrase that ‘no news is good news’ has been working its magic in the markets lately – but it may be the calm before the storm, says Robeco’s Lukas Daalder.

Article also available in :

English ![]() |

français

|

français ![]()

- August was the least volatile month of 2016 due to problem drought

- Investors now face the traditional Autumn market wobbles

- Robeco remains underweight equities and overweight credits

A complete lack of volatility during the traditionally quiet month of August has allowed equities to naturally drift higher – but markets are now likely to enter the equally traditionally volatile Autumn with a new diet of things to worry about, he says.

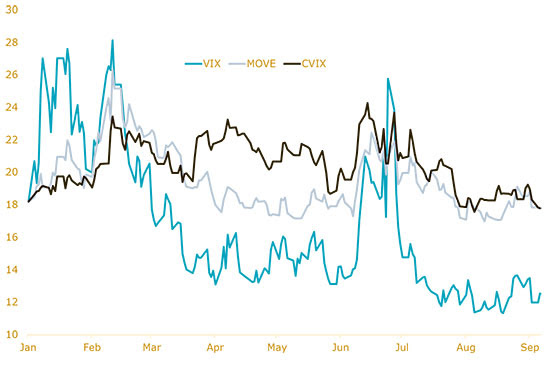

“August turned out to be the least volatile month of 2016 so far,” says Daalder, Chief Investment Officer of Robeco Investment Solutions. “Remarkably, this has been the case for all major asset classes, with the VIX (implied volatility calculated using derivatives in the US stock market), the MOVE (the same for US bonds) and even the CVIX (currencies) all hitting their lowest level for 2016 at the beginning of August.”

“During August, US 10-year yields traded in the narrowest range in almost 10 years, and by early September the S&P 500 had been trading for 40 days without recording a daily change in excess of 1%. The message is clear: volatility was the least of the worries for financial markets.”

Volatility declined across the board and reached lows in all major markets. Source: Bloomberg, Robeco

Volatility declined across the board and reached lows in all major markets. Source: Bloomberg, Robeco

No outspoken signals

“The cause of this drop in volatility is easy to explain: no big market-moving themes have emerged over the past two months. Oil has been in a trading range of USD 42-50 a barrel for four months now, no longer possessing the market-moving abilities it had earlier this year. Central banks at the same time have been in a wait-and-see mode, scrutinizing the data to assess whether they can hike rates (Fed) or whether more stimulus is needed (BoJ).”

“As it happens, this scrutinizing was a pretty easy task to complete, as most of the data points were in line with expectations, and they provided no outspoken signals to expect a change in policy. The Citi Surprise Index for all four regions steadily moved in a five-point range from zero, which is the level at which all data is exactly in line with expectations.”

“The end of the Q2 earnings season; no big political events; no important financial occurrences – the Italian banking sector is still there, the UK is still in the EU, Greece is still in the euro – they all helped to push financial markets into an end-of-summer lull.”

Stocks love low volatility

Is this lack of volatility something to worry about? “On the one hand, the answer is no: we have seen these low-volatile periods before, and they usually do not last much longer than two months,” Daalder says. “It is the longer-lasting low-volatility periods that tend to be harmful, as these create a false sense of safety, prompting investors to take on more risks. With the strong volatility seen at the start of the year, investors are still fully aware of the potential risks, so that is not the main risk right now.”

“There is a much more direct and shorter-term impact though: stocks love low volatility. The daily gains may not be very exciting, but the underlying trend is almost always positive in periods of low volatility. In absence of big news, stocks tend to have the natural tendency to drift higher.”

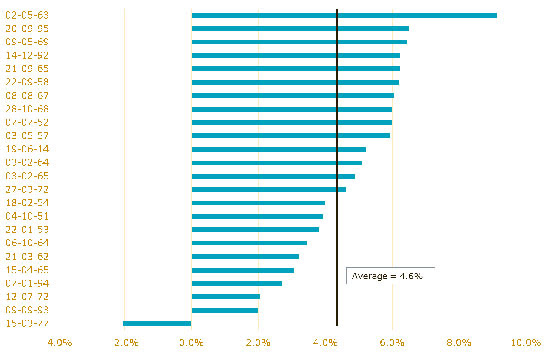

He says data for the S&P 500 index going back to 1930 show 24 periods in which low volatility lasted for two months and stocks rose by an average of 4.6%, as shown in the chart below.

Source: Bloomberg, Robeco

Source: Bloomberg, Robeco

Enjoy it while it lasts

Enjoy it while it lasts – because if history is also a guide, it won’t, Daalder says. Equity markets face their traditional September and October wobbles, as a number of issues from the continuing Brexit saga to the upcoming US presidential elections are likely to restore volatility to its former glory, Daalder warns. Subsequently, Robeco Investment Solutions remains cautious about equities, having avoided the temptation to load up during the low-volatility summer period.

“On balance, we remain underweight equities, as we see numerous risks which have been mostly ignored by stock markets, due to the natural upward drift during low-volatility trading periods,” he says. “Potential grenades include expensive US stocks, pressure on earnings, an uncertain outlook for China, high debt and the November US elections.”

“However, we have closed our short position in the British pound for now: the direct Brexit fallout appears limited, with retail sales and confidence numbers rebounding in August. We do not think that the UK is out of the woods, but the positive data flow will make the pound susceptible to sharp movements.”

“Additionally, with the continued spread compression in the high yield markets, we have reduced our overweight in that asset step by step. At the same time, we have increased our exposure to European credits, as we believe that this market segment will continue to be dominated by the ECB buying program for at least another half year. We expect spreads to tighten further, with investors looking at alternatives that have slightly more yield, such as financial credits.”

Lukas Daalder , September 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |