Market Neutral L/S struggles as momentum stocks take a hit

Risk assets failed to reach a bottom early December despite the U.S and China agreeing to negotiate on trade at the G20 summit. The near-term outlook remains unclear from political uncertainties, which prevent investors from adding risk in portfolios despite lower equity valuations and wider credit spreads.

Article also available in :

English ![]() |

français

|

français ![]()

Risk assets failed to reach a bottom early December despite the U.S and China agreeing to negotiate on trade at the G20 summit. The near-term outlook remains unclear from political uncertainties, which prevent investors from adding risk in portfolios despite lower equity valuations and wider credit spreads. Going forward, the Federal Reserve (the “Fed”) meeting from December 18th – 19th will be critical to gauge whether its stance has effectively turned less hawkish after recent comments in that direction from FOMC voting members. We think the Fed will adjust its stance, and now expect two rate hikes in 2019 vs. three in the Fed dot plot at present.

The dynamic in the hedge fund space throughout November remained similar to October’s, though the damage was far more limited. Merger Arbitrage outperformed while L/S Equity and Special Situations strategies underperformed. L/S Credit strategies remained pretty much resilient despite widening high-yield credit spreads in the U.S. and Europe.

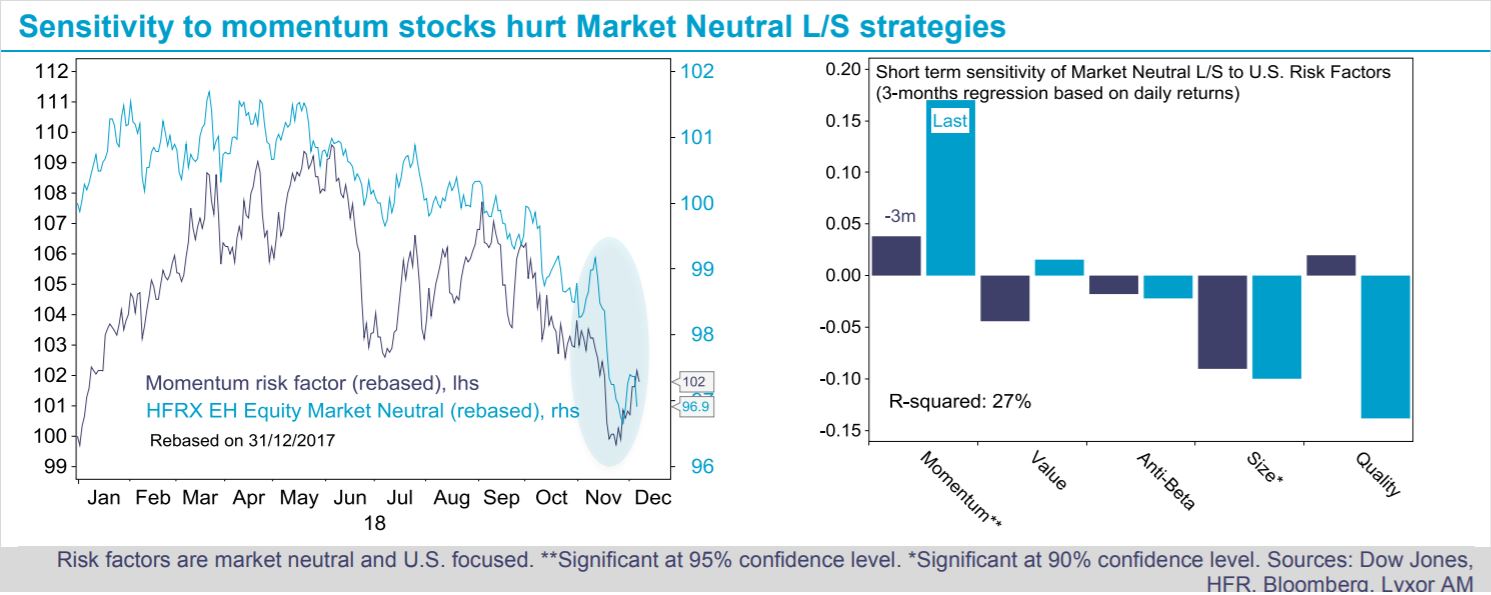

Market Neutral L/S Equity strategies were one area of disappointment in November. The strategy underperformed as momentum stocks suffered another hit. We have long highlighted the sensitivity of the strategy to the momentum equity risk factor over the long run.

Our estimates suggest that such sensitivity, which was limited in early September, has risen markedly since then (see charts below). Based on a sample of 35 L/S Equity Market Neutral UCITS strategies, the median performance was -1.6% in November, the worst was -9.1% and the best was 4.1%. Only 17% of the strategies in our sample were in positive territory last month. Digging into the roots of the momentum’s headwinds, we observe that it has been highly vulnerable to the reversal in Technology stocks. Finally, our views on the Market Neutral L/S strategy have been somewhat defensive. We maintained a neutral stance on the strategy throughout the year. Our lack of enthusiasm for the strategy reflects its perpetual vulnerability to momentum reversals. At the same time, we haven’t recommended an outright underweight stance, due to the benefits of low beta strategies in the current environment. Our stance remains unchanged with a bias towards an upgrade at a later stage, as risk appetite is likely to remain limited in 2019.

Lyxor Research , December 2018

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |