| https://www.next-finance.net/en | |

|

Opinion

|

Are L/S Equity managers concerned by the covid resurgence?

Managers in the U.S. and Europe are continuing to reduce both their net and gross exposures, now converging near their long-term lows. They are selectively selling or shorting stocks that are the most exposed to tighter restrictions, preferring value stocks instead (to position on firming real yields).

Article also available in :

English ![]() |

français

|

français ![]()

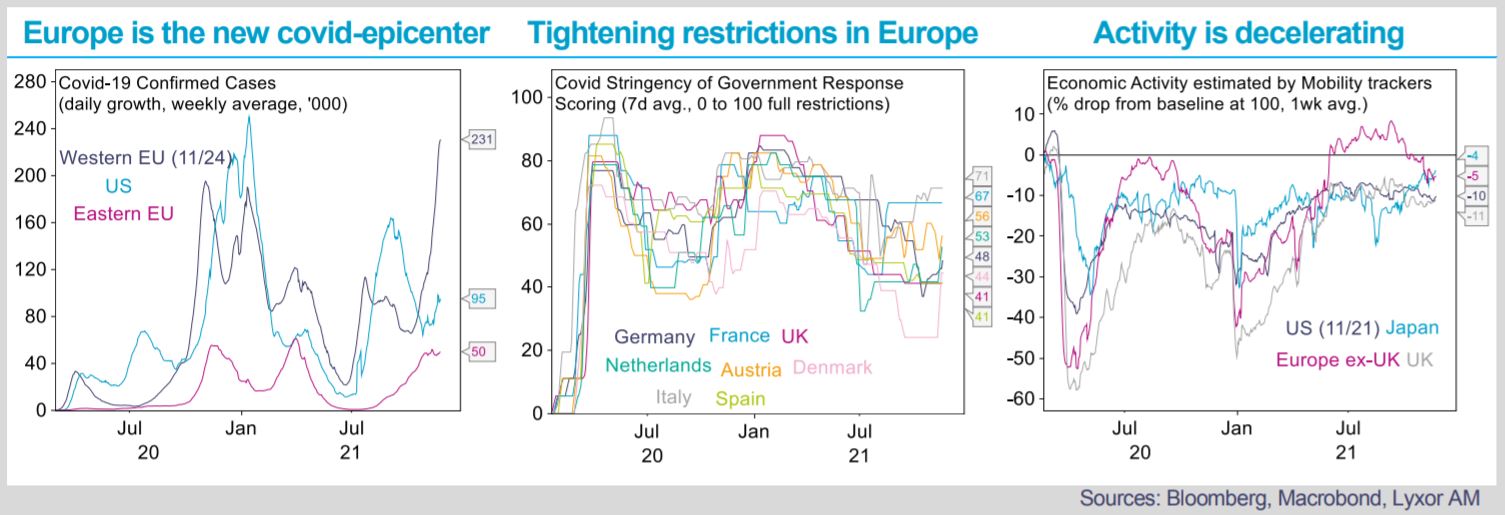

Surging Covid cases in EU and in the U.S. to some extent. Since October, Covid cases have been surging in Northern Europe and the virus is now spreading more broadly on the continent. The declining immunity provided by vaccines after 6 months and seasonality are suspected to be key factors. Countries such as Germany, Denmark, Austria reinstated tighter restrictions and might be followed by others. While broad lockdowns are seen as the last resort, tighter restrictions and a greater fear factor might delay the economic recovery, until this new covid wave is behind. Covid resurgence has been milder in the U.S. but cases might surge in the wake of Europe. The impact has been manageable so far, but high frequency data that track levels of activity are starting to decelerate on both sides of the Atlantic.

Markets are starting to take notice... Since November, concerns about a new covid wave emerged in markets, but the reaction has remained muted so far. In both the U.S. and Europe, differentiation increased between stocks, function of their sensitivity to covid trends. Home-staying related stocks outperformed sectors such as entertainment, consumer services. The Nordics and Eastern Europe markets (where infections are rising the most) also underperformed. At a broader level, cyclical stocks weakened, while flows returned to defensive stocks, downplaying upbeat economic releases in both regions. However, trends in rates and inflation remain bigger movers than Covid and are primarily impacting tech and bond proxies. A temporary loss of economic traction induced by Covid restrictions would give supply-chain glut time to resolve faster. This is reflected by lagging shipping, freight and containers stocks, as well as by the downward reversal in inflation assets.

… As well as L/S Equity managers. Managers in the U.S. and Europe are continuing to reduce both their net and gross exposures, now converging near their long-term lows. They are selectively selling or shorting stocks that are the most exposed to tighter restrictions, preferring value stocks instead (to position on firming real yields). In the U.S., managers are favoring energy, materials and industrial sectors, and are starting to buy tech on dips. In Europe, managers are favoring industrial and financials, and are cutting their core-EMU stocks (which increases allocation to extra euro-area stocks). They are both reducing their consumer discretionary allocations.

Besides, managers are taking profits on stocks with high operational leverage, which benefitted from pent-up demand but now face moderating top-line growth. In contrast with recent months, many managers are also moving to less crowded names.

Implicitly, these moves suggest that managers are starting to factor in greater risk due to Covid restrictions, though they do

not seem to expect broad lockdowns. They anticipate that consumers would bear the brunt of the impact, while the

manufacturing and economic activity would not be seriously jeopardized. The announcement of new restrictions in Europe

hit European managers’ alpha more than in the U.S.

Jean-Baptiste Berthon , November 2021

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |