Hedge funds’ remarkable resilience in turmoil

The Lyxor Hedge Fund Index was down -0.9% in January. 5 out of 11 Lyxor Indices ended the month in positive territory. The Lyxor CTA Long Term Index (+2.2%), the Lyxor Global Macro Index (+0.7%), and the Lyxor Fixed Income Arbitrage Index (+0.7%) were the best performers.

Article also available in :

English ![]() |

français

|

français ![]()

- Hedge Funds displayed remarkable resilience in January. Both markets and analysts started the year with reasonable growth expectations. These were aggressively revised down, triggered by the release of the disappointing Chinese PMI and the CNY depreciation. Strikingly, investors started to price in more serious odds for a Chinese hard landing, the growing central banks’ impotence, the risk of a US recession, and the return of global deflation.

In that context, CTAs thrived on their short commodities and long bond exposures. FI Arbitrage and Global Macro funds exploited monetary relative and tactical opportunities. To the exception of the L/S Equity Long Bias and Special Situations funds – hit on their beta - the other strategies managed to deliver flat to modestly negative returns.

- L/S Equity funds were resilient as they remained on the

sideline. European managers kept their low market exposure. Their

beta was mainly expressed through sectors tilts, with the bulk of

their allocation on the consumer and financial sectors. Implicitly,

they played the reflation and stronger domestic demand themes,

keeping some optionality on the coming March ECB meeting.

The performance of the Long bias funds mirrored their beta exposure. They produced limited alpha, amid elevated stock correlation and thinner dispersion.

Japanese funds maintained their cautious positioning since August 2015. They raised their allocation to financials but maintained low exposure to domestic demand driven sectors. Such a positioning is consistent with greater expectations from BoJ, but persisting skepticism as to Abenomics’ success.

- The pricing of M&A deals and the Merger Arbitrage returns were reasonably insulated from the market turmoil. Investors’ concerns expressed in January did not put in question the existing M&A operations. Besides, merger funds benefitted from several deal completions. The erosion of executives’ confidence and market volatility tamed the pipeline of M&A deals in January. However, significant operations continued to fuel arbitragers’ opportunities, including the announced Shire vs. Baxalta, Tyco vs. Johnson Controls, Abott vs. Alere deals.

Special Situation suffered yet again in line with their market beta. There was a limited number of idiosyncratic events in the Special Situations space. Their aggregate net exposure remained steady at 50% - including a 10% of short indices - the bulk of which allocated to consumer, telecom and technology situations.

- The rebound in oil prices eased the pressure on L/S Credit strategies. While credit markets kept on bleeding, they outperformed equity markets. Spreads already pricing a recession and the rebound of oil did help. With growing dispersion within credit sectors, the alpha backdrop improved. By month-end L/S Credit funds started to chase opportunities, while adding long government bonds.

- Source : Bloomberg, Lyxor AM

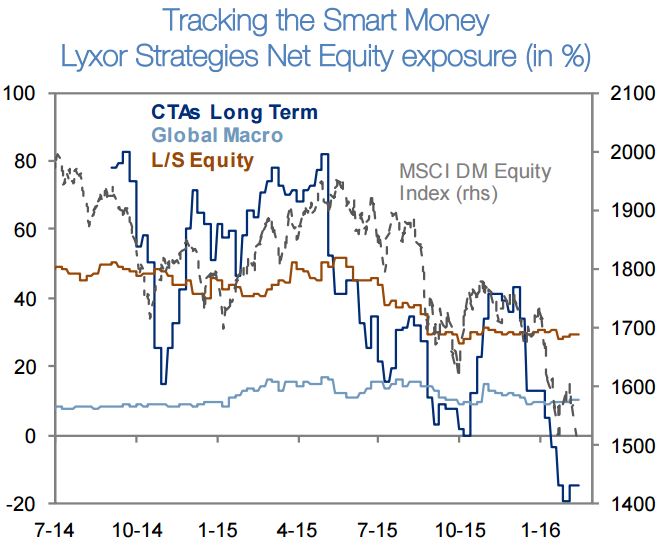

- CTAs, best performers, thrived on their short commodities and

long bond exposures. Meanwhile they were immune from the

equity sell-off, having cut all of their remaining exposures by midDecember.

Short-term models even built up short exposures to

equities.

They gave back some of the accumulated gains by month-end. Indeed, the sharp rebound in oil prices hit their short on energy futures and their short FX exposures on the commodity block (CAD especially). As of today, they are -40% short on energy positions and 49% long on USD crosses.

CTAs once again stood as hedge in portfolios during risk aversion episodes.

- Bond positions saved the day for Global Macro funds. Individual positioning displayed increasing managers’ divergence. In aggregate, most of the gains were made main through global rate arbitrage. They were overall long US and short European bonds, according to their relative monetary policy anticipations. They did not profit from BoJ unexpectedly pushing rates further into negative territories: they held a small short allocation to Japanese bonds. A majority of the managers refrained from playing commodities, though some of them built up short positions in the second half.

Within their equity bucket (a small one, around 10% in net exposure), they concentrated on reflation zones: a drag on performance, but a modest one. Overall, global macro funds continue to maintain relative value and balanced exposures. Their key vulnerability lies with their long USD crosses, which would suffer from a reversal in dollar.

“While a sub-par global growth seems well priced in, the accumulation of downside risks lead us to stick to our preference for relative-value, tactical and macro styles, which should outperform the more directional strategies.” says Jean-Baptiste Berthon, senior cross asset strategist at Lyxor AM.

Next Finance , February 2016

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |