Hedge funds increasingly active in bitcoin

While the bitcoin bull run in 2017 was largely driven by retail investors, the 2020 surge appeared to be driven by a wider set of investors, including institutionals. In addition to retail investors, family-offices and high-net-worth investors remain dominant investors and sources of new bitcoin wallets and IP addresses.

Article also available in :

English ![]() |

français

|

français ![]()

While the bitcoin bull run in 2017 was largely driven by retail investors, the 2020 surge appeared to be driven by a wider set of investors, including institutionals. In addition to retail investors, family-offices and high-net-worth investors remain dominant investors and sources of new bitcoin wallets and IP addresses. Bitcoin benefitted from a supportive backdrop, increasingly used as a hedge against falling real yields and massive central banks QE, which are feared to ultimately debase world currencies and boost inflation. It is also an alternative to declining equity dividend yield. Unsurprisingly, bitcoin’s correlation with gold and inflation, and to some extent equities, has become reasonably stable.

Hedge funds have become significant bitcoin players, through dedicated investment vehicles, or through bitcoin additions to their allocations.

While still in its youth, the market continues to gain depth, both in types of investors and product range. In the early days, managers mainly focused on long outright positions on crypto assets, including Bitcoin, Ethereum, or Ripple. Since then, a broader range of digital assets-linked products allows managers to implement more flexible and sophisticated strategies. Managers can now use swaps, futures and options indexed on cryptocurrencies, they can also focus on income generated by the underlying technology.

Moreover, they may invest in securities issued by companies involved in crypto assets and their infrastructures – though most of these remain only accessible through venture capital and private equity strategies. Hedge fund styles include discretionary and quantitative approaches.

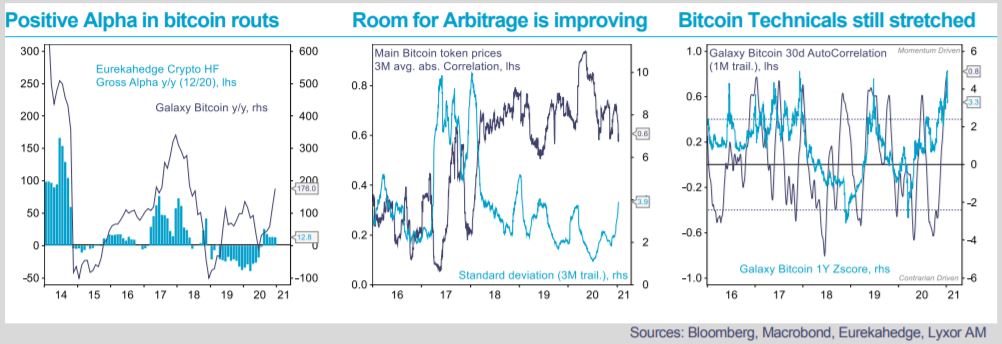

As the market gains depth, attracts new experienced investors, and has an improving information flow, the alpha potential will likely moderate over the coming months and years. Yet, the market remains highly inefficient, and significant digital asset price dispersion provide room for arbitrage.

Several key risks warrant persisting high volatility. Tighter regulation remains a structural risk (early regulation mainly focused on preventing fraud and misrepresentation, broader ranges of violations and risks will gradually be considered).

Speculation risk is another obvious risk, amplified by leverage and systematic trading. Moreover, the absence of a central authority to step in in times of crisis leaves investors without backstop. Risks also come from the complexity of crypto technologies and the surging supply of digital assets, though this nearly $1tn market remains dominated by two providers.

The recent bull run was cut short by a -20% drop. Valuation indicators keep on flashing red (in particular our macro and

market relative models). A normalization in momentum forces could also keep selling pressures. Yet, liquidity metrics

have not deteriorated in an exaggerated manner thus far. We expect the latest cold shower to moderate institutionals’

enthusiasm in the short-term, providing time to prepare for a third run later, and supported by tools better suited for

institutionals (including initiatives from central banks and commercial banks to offer more robust digital asset exposure).

Lyxor Research , January 2021

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |