| https://www.next-finance.net/en | |

|

Opinion

|

Central banks: toward a bipolar world

Should one expect a huge differential in interest rates? Undoubtedly. According to René Defossez, having said that, this differential should be far more pronounced at the short end of the curve than at the long end. The reason is that short rates will be influenced directly by monetary policy, whereas long rates will remain more or less protected by many factors...

Article also available in :

English ![]() |

français

|

français ![]()

We mentioned at the start of last week that strategies for the world’s leading central banks were on diverging paths. This is all the more apparent after the decisions taken by the Federal Reserve and Bank of Japan last week. While the US central bank exited Q3 last week, its Japanese counterpart announced a ramping up of QE (the objective now being to expand the monetary base by JPY 80trn a year). The former is preparing the market for an increase in the Fed Funds rate in 2015, whereas the latter, which can no longer act on short rates (which are already near zero percent), is looking to bring down long rates, the goal being for real long rates to be as low as possible (the Japanese 10-year currently sits at its lowest level since April 2013).

On the one hand, there are central banks which have (or believe they have) the possibility to tighten monetary policy in a no longer very distant future (Federal Reserve, Bank of England, Bank of Canada). On the other hand, there are central banks attempting to ease their monetary policy (European Central Bank, Bank of Japan). At the level of the G7, there are providers of liquidity, and then there are countries that stand to benefit from the liquidity injections. Monetary policy rates in these two categories of countries are set to move apart. Pre-crisis, the one exception to the rule at the level of G7 countries was Japan. It will soon be joined by the Eurozone.

Turning to smaller developed countries, the same dichotomy is in evidence. Sweden, for example, where inflation has been very weak for some time, on occasion negative, has just lowered its repo rate to zero percent. Switzerland, where inflation is also negative (running at -0.1% currently), is likely to align its monetary policy on the European Central Bank’s monetary policy for quite some time.

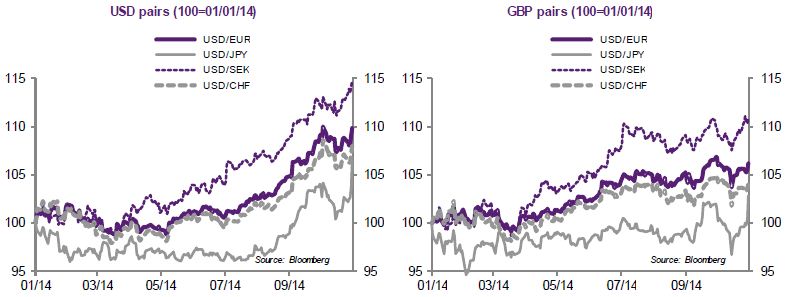

The bipolarisation mentioned above should therefore concern not only G7 countries, but a far larger number of countries, as suggested by the chart below.

This configuration raises a number of issues:

- 1. How can one part of the world grow without the other part benefiting from this growth? The answer probably lies in the nature of the economic recoveries: they are essentially domestic and have not, therefore, led to a sharp rebound in global trade. Put more plainly, the US economic recovery is proving a rather poor engine of growth at global level.

- 2. Should one expect major adjustments in the foreign exchange market? In theory yes, especially since those central banks that will keep their rates on hold for a prolonged period are also those that will expand their balance sheets. In fact, these adjustments are already under way, with the decline of the euro, Japanese yen (more recently), Swedish krona and Swiss franc against the US dollar and sterling.

- 3. Should one expect a huge differential in interest rates? Undoubtedly. Having said that, this differential should be far more pronounced at the short end of the curve than at the long end. The reason is that short rates will be influenced directly by monetary policy, whereas long rates will remain more or less protected by many factors, notably the still very abundant liquidity at global level. The one major difference will be the identity of the central banks providing this liquidity. Moreover, through their balance sheet policies, central banks confronted by a difficult economic situation should be able to sever the correlation between their rates and US rates.

Of course, many of our strategies are or will factor in the two-speed world.

Of course, many of our strategies are or will factor in the two-speed world.

René Defossez , November 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |