| https://www.next-finance.net/en | |

|

Strategy

|

CTAs as shock absorbers

In the space of alternative strategies, Global Macro and Event-Driven strategies rebounded the most since March 23rd. Both Merger Arbitrage and Special Situations sub strategies benefitted as M&A deal spreads tightened significantly since mid-March.

Article also available in :

English ![]() |

français

|

français ![]()

Market conditions improved in the wake of the aggressive Federal Reserve announcements to tame risks in the financial system. The MSCI World bottomed on March 23rd and rose more than 20% since then, leaving the broad equity market benchmark down -18.5% since the peak on February 19th. In the meantime, High Yield credit spreads tightened in the order of 200bps in EUR and 300bps in USD since the peak of risk aversion according to Merrill Lynch benchmarks.

In the space of alternative strategies, Global Macro and Event-Driven strategies rebounded the most since March 23rd. Both Merger Arbitrage and Special Situations sub strategies benefitted as M&A deal spreads tightened significantly since mid-March. During the rebound, CTAs underperformed due to their defensive positioning. But their negative returns over the past few weeks were fairly limited (c. -0.5% per week) compared to the trend reversal in equity and energy markets.

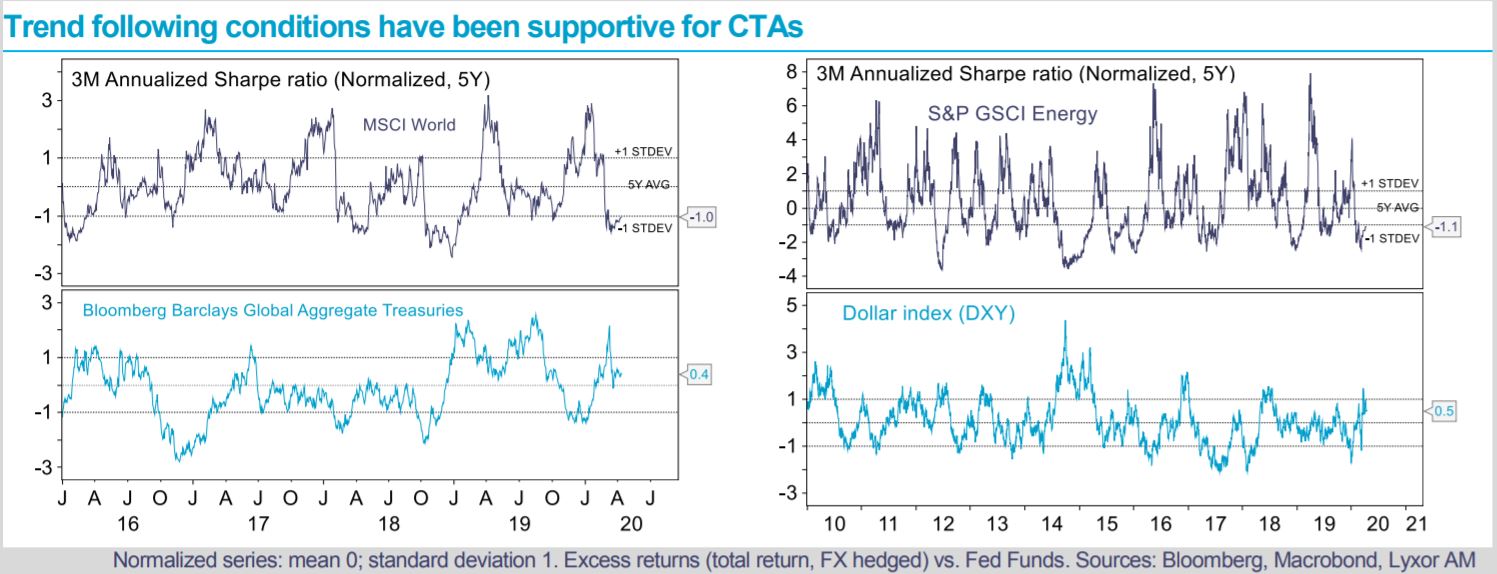

We focus on the reasons why CTAs did well during the selloff and why they contained the losses during the rebound, leaving it as the best performing strategy year-to-date (-1.3%) after a strong year in 2019 (+8.4%). CTAs navigated the market selloff remarkably well due to long positions on fixed income and defensive trades in commodity and FX markets.

Long precious vs. base metals and short energy trades were helpful as OPEC+ disagreed on oil production cuts. Then, long USD positions were rewarding as funding shortages in USD fueled the currency.

Equity positions were cut early March, to a negligible or in some cases short stance on the asset class now. CTAs showed great risk management capabilities. They cut exposures so much that they are now running one of their lowest level of risk ever, sitting on a huge level of cash. Market moves in the second half of March were thus muted even when markets continued to swing up and down. With a defensive bias, downside is limited, but upside too. High dispersion between strategies came from time horizons (the shorter the better) and sectors allocations (those with more commodities did better).

Going forward, we stick to our Neutral stance on CTAs, structurally, and reaffirm with a high degree of conviction its attractiveness in portfolios for the long run.

It has been highly challenging to time the momentum risk factor across asset classes, historically. In the coming weeks and months, the main source of risk would be a rise in bond yields if the risk adverse mood reverses in a sustainable manner. However, the strategy has recently demonstrated its ability to cut long allocations swiftly when conditions change. Finally, we also stick to our preference for mid-term CTAs, which have been more flexible in adapting to fast changing trend following conditions.

Jean-Baptiste Berthon , Philippe Ferreira , April 2020

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |