| https://www.next-finance.net/en | |

|

Interview

|

Aude Lerivrain : « Can we invest in the chinese banking sector without worries? »

According to Aude Lerivrain, Head of Credit Research at CPR AM, we are seeing in the Chinese banking system many of the early warning signs of the major banking crises of recent years (in the US, Ireland and Spain)...

Article also available in :

English ![]() |

français

|

français ![]()

WHY LOOK INTO CHINESE BANKS TODAY?

Aude Lerivrain: Chinese banking issuers are increasingly present on international bond markets. That’s why we decided to look into the health of the Chinese banking sector, which is at the heart of this economy in full flux.

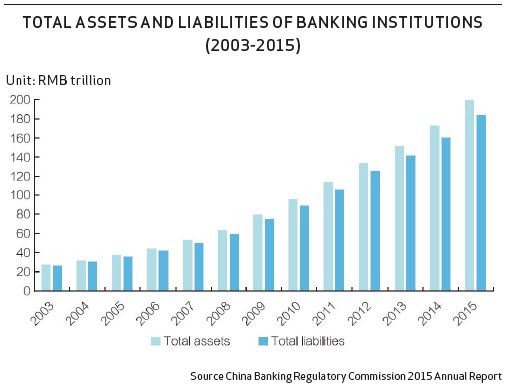

To get a good idea of the workings of this complex system we need to look back at the uniqueness of its development. The banking system was a monopoly and hardly existed at all before 1978. It was recast from the ground up by Deng Xiaoping’s reforms and opening up of the economy, with the establishment of four state banks, each enjoying a monopoly in a specific area, i.e., infrastructure, industry, foreign trade and agriculture. The Commercial Bank Law of 1995 eliminated this monopoly for state banks and expanded the system with the creation of three policy banks in charge of assisting the development of certain sectors without a profitability objective and the creation of public-private banks and local banks. This raised the number of banks from five to more than 30,000 in 20 years. Bank assets quintupled in 10 years to 232 trillion renminbi in 2016 (about 32 trillion euros), and four Chinese banks are now classified as GSIBs (Global Systemically Important Banks). This breakneck growth was driven by the fact that the government at first counted on the banks and not the financial markets to finance China’s development. It is now turning towards market financing on both its domestic market and internationally.

ARE THE CHINESE BANKING SYSTEMS’ WELL-KNOWN WEAKNESSS DUE TO ITS HISTORY?

Aude Lerivrain: It is quite right that Chinese banks’ structural weaknesses are due to the structure and development of the Chinese economy. The “all state and administered” model with its implicit state guarantee at all levels has not urged banks to develop a culture of risk and fair price.

WHATS THE POINT OF REVIEWING A LOAN PORTFOLIO IF THE COMPANY IS PUBLIC AND IF THE STATE IS THE GUARANTOR OF LAST RESORT?

Aude Lerivrain: This phenomenon has been made even worse by the reliability of the legal framework and reporting, corruption, and the proper economic functioning of publicly owned companies (including “zombie companies” and “living dead public-sector groups” the banking regulator talks about). Coming on top of the explosion in outstanding loans and the cyclical nature of the Chinese economy, no wonder non-performing loans skyrocketed. The Chinese state has taken on this problem many times in the past with the creation of defeasance structures, but this is still an issue, as the flow of nonperforming loans continues, in particular in city commercial banks and credit cooperatives!

Another risk factor to keep an eye on is shadow banking. In recent years banks have developed off-balance-sheet activities in order to get around regulations that hemmed in their growth. With their frightening amount of offbalance-sheet assets (more than 20 trillion renminbi), wealth management products, which are bank deposit substitutes, are the main concern, as they are still implied liabilities for banks, given that they are targeted to retail customers but with no offsetting capital. They are invested in assets that traditionally are riskier than balance sheet assets and carry short maturities and need to be rolled over very often. So Chinese banks could begin to face liquidity issues, whereas financing via domestic customer deposits was one its main strengths and seemed to rule out any liquidity risk.

In short, we are seeing in the Chinese banking system many of the early warning signs of the major banking crises of recent years (in the US, Ireland and Spain). Is a soft landing of the Chinese financial system possible? Seems unlikely without state support!

IN THAT CASE WHY TAKE THE RISK OF INVESTING?

Aude Lerivrain: The state is ubiquitous in China. Banks are state-run; they lend to public-sector companies; and investors authorise investments, while assuming that the state will serve as a last resort. So confidence in the Chinese government to control leverage in the financial system, manage economic growth and overheating in certain sectors is crucial. And the government’s will to do so in this area is beyond a doubt! Especially as it can rely on the strengths of its economy, including abundant domestic savings, very heavy fiscal resources, and little dependence on foreign investors. But is this argument enough for investing in Chinese banking groups?

Next Finance , July 2017

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Interview Isabelle Bourcier : “Our ambitions is to grow in Smart Beta and SRI ETFs”

Evolution of the ETF market, impact of the regulations, ongoing development at BNP Paribas Asset Management...Isabelle Bourcier, Head of quantitative and index management at BNP Paribas Asset Management shares its view with (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |