| https://www.next-finance.net/en | |

|

Opinion

|

A critical change of paradigm for hedge funds

At the turn of the month, hedge funds rebounded as market conditions improved. The Lyxor Hedge Fund Index was up 0.4% last week, following a 3.3% drawdown in August. Year to date, hedge funds have demonstrated their ability to protect portfolios, returning - 0.3% whilst the MSCI World and JPM Global Aggregate Bond Index were down 7% and 2.3% respectively.

Article also available in :

English ![]() |

français

|

français ![]()

At the turn of the month, hedge funds rebounded as market conditions improved. The Lyxor Hedge Fund Index was up 0.4% last week, following a 3.3% drawdown in August. Year to date, hedge funds have demonstrated their ability to protect portfolios, returning - 0.3% whilst the MSCI World and JPM Global Aggregate Bond Index were down 7% and 2.3% respectively. On a risk-adjusted basis, the outperformance of hedge funds is impressive and marks a critical change of paradigm.

Fears of competitive devaluations in EM and unease about the timing and amplitude of the Fed’s tightening cycle has recently caused markets to move in a way not seen for years. In the short term, we expect that market conditions will improve due to a combination of supportive fundamentals in developed markets and the Chinese not engaging in a beggarthy-neighbour policy. However, renewed bouts of volatility are likely to haunt investors regularly in the medium term due to uncertainties over interest rates. In this environment, hedge funds are likely to outperform traditional asset classes, a topic we have discussed in previous publications (See A New Era for Hedge Funds – June 2015).

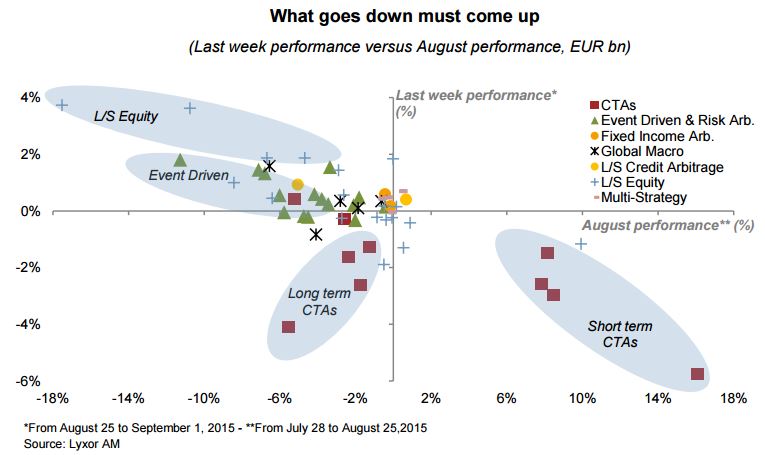

Following on from the drawdown in August, hedge funds were up in early September. Managers that suffered during the selloff rebounded the most last week (see chart).

Event Driven and L/S Equity funds outperformed while CTAs underperformed after being negatively affected by the rebound in commodities and the rise in bond yields. We are now upgrading Event-Driven, a strategy which we were defensively positioned during the selloff.

In response to widening deal spreads, these funds appear increasingly attractive at current levels. Meanwhile, we continue to favour CTAs over the midterm as they provide adequate diversification benefits in a portfolio. Their current positioning is vulnerable to any market rebound: neutral on equities, long bonds, long USD and short commodities. Nevertheless, from a strategic point of view, CTAs remain a good option in portfolios amidst the unprecedented challenge of normalising monetary policy in the US.

Philippe Ferreira , September 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |