| https://www.next-finance.net/en | |

|

Opinion

|

Why investors should be optimistic about Japan

There are several reasons to be optimistic about Japanese equities in 2020. First, consider valuations. Whether on price-to-book or price-to-earnings, Japanese stocks are among the cheapest in all developed equity markets. Take the price-to-book ratio of the MSCI Japan.

Article also available in :

English ![]() |

français

|

français ![]()

There are several reasons to be optimistic about Japanese equities in 2020.

First, consider valuations. Whether on price-to-book or price-to-earnings, Japanese stocks are among the cheapest in all developed equity markets. Take the price-to-book ratio of the MSCI Japan. Currently trading at only 1.2x, it is 50% lower than the MSCI Europe’s price-to-book ratio of 1.8x, and less than a half that of the MSCI USA’s figure of 3.4x. [1]

Second, let’s take a look at Japan’s economy. Sure, the upturn in 2019 has been only modest. But there are signs that the global economy may have hit the bottom. Some cyclical data points such as Japan’s exports and machinery tool orders had sharply dropped since the beginning of 2018, but they look to be bottoming. If the bottoming view proves correct, it may be helpful to remember that in 2016-2018, the MSCI Japan surged roughly 50% in just 19 months [2] as global growth prospects improved. Even mere stability would benefit the cyclically geared Japanese equity market.

Indeed, we think many investors pay too much attention to the negatives in Japan such as October’s hike in consumption tax from 8% to 10%. We do not expect a significant negative impact on the economy this time, as there were some exemptions and subsidies from the government. In fact, we saw less evidence of pre-emptive purchases by consumers ahead of the hike than in the past. If the Japanese economy were to slump, it is highly likely that the Japanese government would announce a fiscal stimulus package to fully support the economy.

POSITIVE FACTORS

Some investors are also overly focused on Japan’s structural problems of high government debt to GDP and its rapidly ageing population, which acts as a drag on GDP growth as the labour force declines. As Japan’s labour force is not growing, the government has provided some support for women to return to work (the female labour participation rate in Japan already exceeds that of the US) and Japan is now actively accepting highly-skilled foreign workers (the number of foreign workers has been almost doubled in a decade).

With rising IT investment and the government-led labour reforms, labour productivity growth in Japan is now the highest among all developed economies. This should provide a welcome boost to Japan’s economic growth. Companies are looking to invest in areas such as IT and employee education to further drive productivity. We see sectors such as business services, outsourcing, IT and software benefiting. Also, as 5G wireless technology is starting to be rolled out across China, the US and Japan as a next generation infrastructure to support things like IoT and autonomous vehicles, we are investing in companies that will benefit from this roll out.

Next, we turn to tourism. The Japanese government has grand ambitions to significantly ramp up overseas visitors to Japan from current levels of approximately 30 million to 60 million a year by 2030. This would provide a significant consumption boost and follows an already steep rise in tourism in Japan. By comparison, in 2011, there were just over 6 million visitors to Japan. [3]

OLYMPICS SHOWCASE AND MORE

Investors should not ignore the 2020 Olympics in Japan. In 1964, Japan used the Olympics to showcase its pioneering high-speed train, the Shinkansen. This time it will showcase its many ground-breaking technological innovations, from robotics to autonomous driving, which can only help to focus the eyes of institutional and retail investors from around the globe on Japan.

The Tokyo Metropolitan Government estimates the economic effect will amount to ¥32.3 trillion ($300 billion) and 1.94 million additional employees from 2013 through 2030. We do not expect there to be a significant post-Olympic hangover in Japan as the Japanese government has been careful not to over-invest. This is just one more reason why we believe 2020 will be a good year for Japanese equities.

Unrelated to the Olympics, Japan’s Integrated Resort Bill could make the nation the next great gambling market, and casino operators are jockeying their way to win concessions. For as much as a casino will cost, the opportunity to be one of three concessionaires is tremendous. Fitch estimates that gambling revenue could be $10 billion annually, topping the $6.6 billion the entire Las Vegas Strip generates per year.

CORPORATE GOVERNANCE REFORM AS A GAME CHANGER Finally, we believe corporate governance reform is a game changer for both corporate management and investors. Overhauling corporate governance to harness the power of private enterprise is a key aspect of Japan’s growth strategy. Letting corporate management focus on return on equity (ROE), increasing external board membership and encouraging constructive communication with investors have been extremely beneficial. Corporate governance reform has materially changed the mindset of Japanese corporate management teams – they are now focusing more on profitability, capital efficiency and shareholders’ interests.

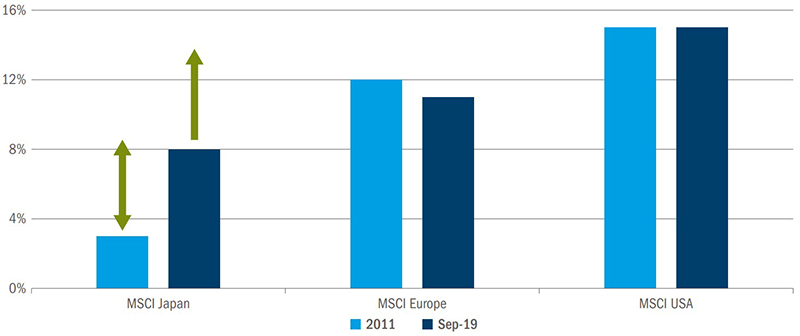

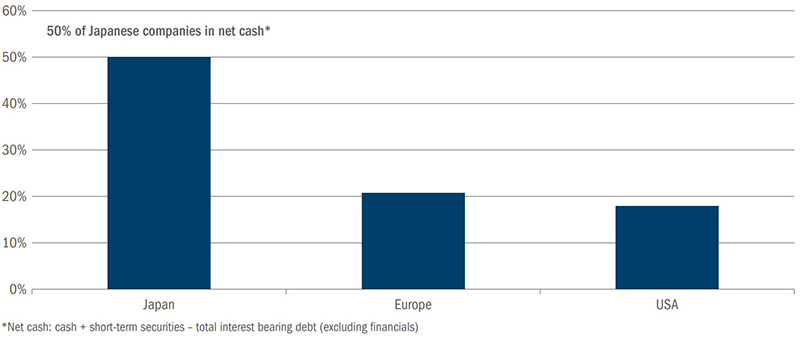

As a result, the average ROE has risen to about 10% over the past five years [4], in line with European averages. But there is still low-hanging fruit for a further increase since Japanese companies have a tremendous amount of cash on hand. Approximately 50% of Topix 500 Index non-financials have a net cash position, compared with only 20% for the US and Europe [5]. Looked at another way, cash as a percentage of the MSCI Japan Index’s market capitalisation is about 20%, which is twice as high as the MSCI Emerging Market Index and four times the MSCI USA Index [6]. Despite 10 consecutive years of increasing dividend payments and a roughly 50% year-on-year rise in share buyback activities, corporate Japan’s financial leverage has fallen consistently for almost a decade.

All this data suggests that Japanese companies are highly likely to continue putting excess cash to work in the decade to come. The average ROE of Japanese companies has already doubled since “Abenomics” was initiated, but we believe there is further to go, which can only be positive for share prices. This will be particularly true over the longer term as the compounding effect of these reforms takes hold.

Signs of global economic growth improving, as well as relatively attractive valuations, bode well for Japanese equity markets. Added to this the continuing positive impact of corporate governance reforms should play a critical role for share price appreciation in 2020 and beyond.

CHARTS TO KEEP AN EYE ON IN 2020

JAPAN: SUBSTANTIAL ROOM TO INCREASE ROE BY PUTTING CASH TO WORK

JAPAN: OUTSTANDING FINANCIAL FLEXIBILITY

Daisuke Nomoto , January 2020

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] Source: Bloomberg, 2019.

[2] Source: Bloomberg, 2019.

[3] Source: Japan National Tourism Organisation.

[4] Source: Bloomberg, November 2019.

[5] Goldman Sachs, 2019.

[6] Goldman Sachs, 2019.

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |