| https://www.next-finance.net/en | |

|

Opinion

|

Suddenly last summer

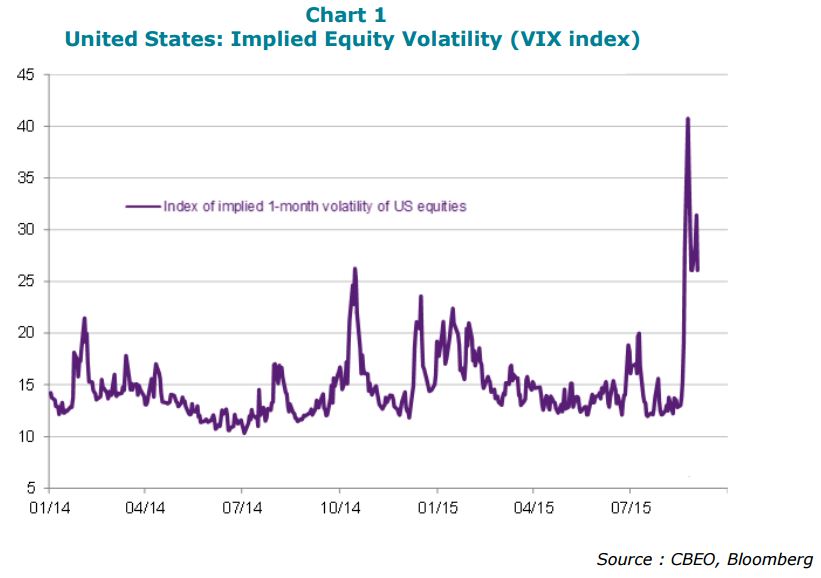

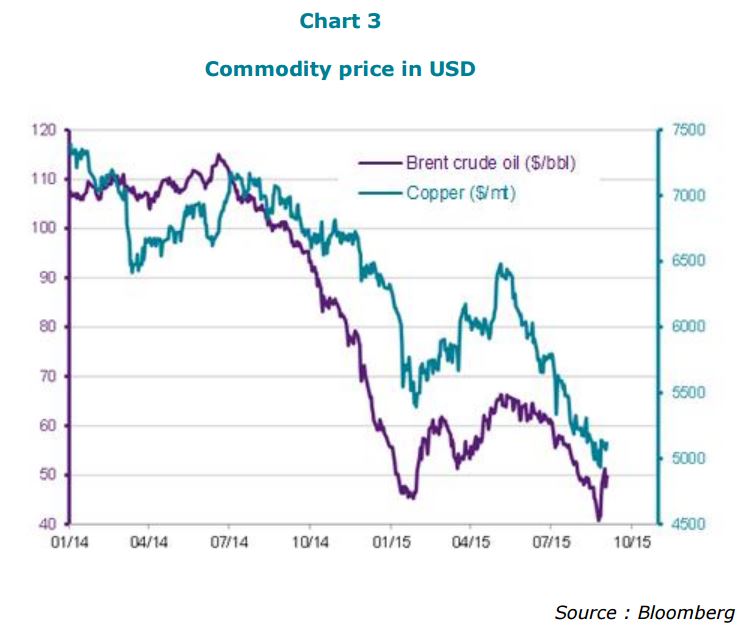

There were bouts of volatility in financial markets this summer: collapse in Chinese equities, depreciation of the yuan dragging down emerging currencies, drastic fluctuations in equity markets in developed countries, collapse in commodity prices, etc. How can we interpret this turmoil and what is its impact on our asset allocation?

Article also available in :

English ![]() |

français

|

français ![]()

There were bouts of volatility in financial markets this summer: collapse in Chinese equities, depreciation of the yuan dragging down emerging currencies, drastic fluctuations in equity markets in developed countries, collapse in commodity prices, etc. How can we interpret this turmoil and what is its impact on our asset allocation?

Autumn in Beijing

Macroeconomic figures for developed countries were more or less in line with expectations. Eurozone growth slowed down slightly in Q2 to 0.3% after 0.4%, but conditions remain extremely favorable for a continuation of the recovery: cheap oil, a weak euro, low real interest rates, constantly improving bank lending conditions. Moreover, in Greece, the parliament voted the first series of reforms without difficulties, paving the way for the disbursement of the first phase of the European bailout package. In the United States, growth jumped markedly in Q2, estimated at 3.7% at an annualized rate, after the disappointment in Q1.

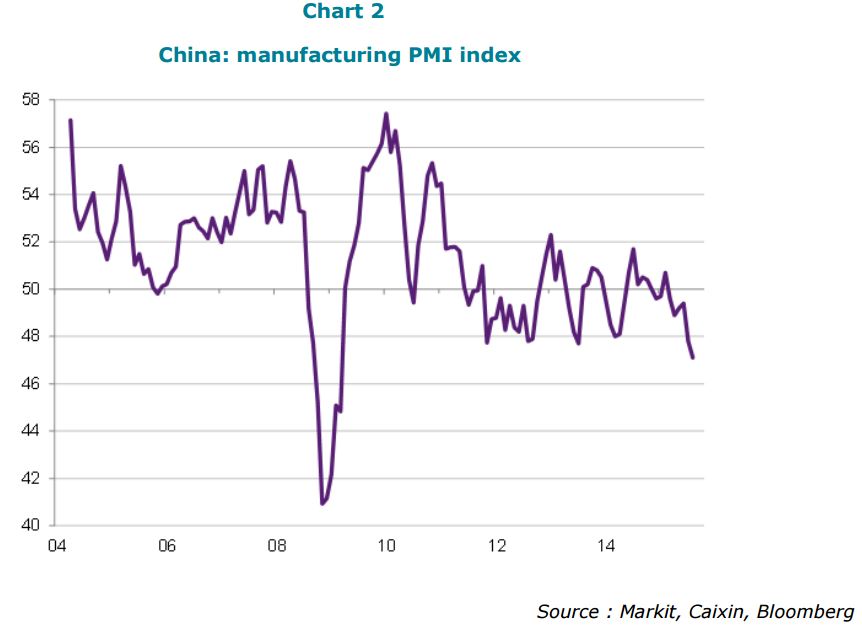

Investor concern is focused on emerging countries, where the macroeconomic risks combine with growing political problems in a vicious circle. In addition to domestic political risks (Malaysia, Brazil) international affairs are at play (Russia, Turkey, Egypt). The impasse in the Chinese development model is the main factor behind the slowdown in emerging countries. The growth regime based on urbanization is coming up against a number of constraints, be they real (overproduction of housing, industrial overcapacity, bad investments), political (surge in inequalities, corruption) or financial (excessive debt of property developers, heavy industries and local governments) while external competitiveness is suffering from the rapid rise in wages and the appreciation of the yuan in the wake of the dollar. In addition, economic policy has suddenly seemed muddle-headed and inconsistent, reflected by the authorities’ erratic interventions in the equity market at the beginning of the crash, or the incomprehensible announcements made by the central bank, which decreed a virtually free float of the yuan in August while resuming its interventions two days later, thereby restoring the status quo ante. Also, the use of a police crackdown to punish those "responsible" for the equity market crash reminds us of the ideological rigidity that is typical for a regime under pressure.

Serious, lasting, global

Whether or not the Chinese economy has a smooth landing is likely to haunt financial markets for many months to come. The authorities’ erratic reactions seem to reflect a rare indecisiveness at the highest level of the State, which is easily understandable as there are only “bad” answers to a bursting of an over-investment bubble: stimulating real estate or infrastructure once again would only create further distortions; devaluing the yuan would dampen consumption and create a dispersal of exchange rates throughout Asia. Meanwhile, scattered half-measures to stimulate the economy (rate cuts, acceleration in existing infrastructure programs) can be expected to curb the slowdown in the economy without solving the underlying problem.

The repercussions are felt worldwide, but have the heaviest impact on suppliers to China, in capital goods (Japan, Germany, South Korea, etc.) and on commodities, i.e. most emerging countries (Russia, Brazil, Chile, South Africa, etc.) but also some developed countries (Australia, Canada). Moreover, some emerging countries are also building up monetary imbalances (inflation in Brazil and Turkey, exacerbated by the currency depreciation) and external imbalances (excessive current account deficits in Turkey, South Africa, etc.), which will be exacerbated by the increased cost of imported capital once the Fed hikes its interest rates.

Asset allocation

What should be done? With the exception of Japan, equity markets in developed countries were expensive, but they have fallen. The Chinese risk should nevertheless continue to weigh on valuations, which remain fragile in the United States, caught between the Fed and faltering margins (wages, productivity). The credit market had already reacted to the deterioration in corporate balance sheets; its message should not be forgotten when analyzing PERs, which are currently being boosted by the mechanism of share buybacks with borrowed money ($550bn in one year for the S&P 500). Monetary policies are already at full throttle (ECB, BoJ) or at a dangerous turning point (Fed), so the support will hardly come from G7 central banks. Lastly, the disappearance of the recycling of petrodollars and the liquidation of foreign exchange reserves by emerging central banks are limiting the ability of long-term interest rates to dampen the risk of volatility in equities. The equity risk is therefore becoming more significant and increasingly difficult to hedge through bonds in a diversified portfolio.

We are therefore continuing our move to reduce risk in our multi-asset portfolios by changing over to neutrality in the equity asset class while keeping a long bias in European and US bonds, at the expense of liquidity. To this end, we are neutralizing our exposures to US and Japanese equities, but we keep an overweight position in Eurozone equities and an underweight position in emerging markets. We also maintain an underweight position in commodities with the exception of gold (neutrality).

Raphaël Gallardo , September 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |