| https://www.next-finance.net/en | |

|

Strategy

|

Subordinated debt – worth a look for yield-starved investors

Bonds yield little, while equities are not particularly cheap. Against that unappealing backdrop, looking beyond the beaten track for alternatives may prove rewarding. Anthony Smouha, CEO of Geneva-based Atlanticomnium, explains why he believes that junior debt could be an attractive investment proposition.

Article also available in :

English ![]() |

français

|

français ![]()

Debt and equity analysts look at companies differently. Most commonly, debt bears a coupon and has a maturity, so a debt investor looks at whether the company can earn enough money to easily pay the cou-pon (interest coverage) and then will have either sufficient liquid assets to reimburse the debt at maturity, or income-generating assets to be able to refinance at maturity. Within high-yield debt, the risks are high-er that the liquid assets or income-generating assets could be insufficient to meet reimbursement obliga-tions, so the debt investor will also look at the recovery value. This includes analysing the seniority of the claims versus other creditors.

Equity investors may also be concerned with these matters. They primarily analyse the valuation, looking at capacity of the business much more dynamically. Questions will include: Will it grow? What protections does the business have versus competitors or potential entrants? What are its unique features? Is it well managed? Where is it placed within its sector?

Combining debt and equity-type analysis

When investing in subordinated debt, we use a combination of both debt and equity-type analysis. As subordinated debt holders, we usually give up the potential for unlimited gains that can be achieved by equity holders, but we are still a junior stakeholder if the company gets into trouble. We also give up the priority in debt repayment compared to a senior debt holder, in addition to giving up the certainty of a date of reimbursement.

In our approach, the analysis of subordinated debt focuses on a company’s business model and its sus-tainability. If these are unclear we will not invest. The difference between us and the equity analyst is: The equity analyst has to both like the company and the price of the stock before investing, whereas our only concern is whether we like the company. We are not concerned about the price of the stock. This also means that whether the residual value is judged to be more or less is not a critical issue for us. However, it must have a certain value, which has to be enough in good times and bad to service the debt.

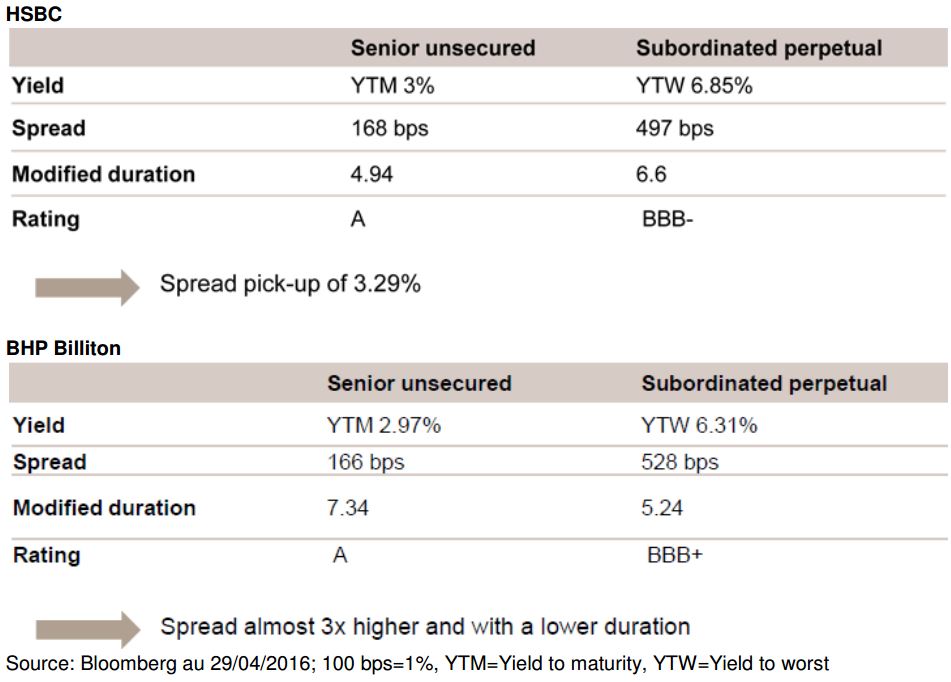

Whereas its share price can fluctuate significantly, as long as the company does not fall into distress we collect our coupons and retain our principal value claim. Equities have no principal value claim – losses can reach the total amount of capital invested. The tables below show two top-quality companies where the returns are compared between different types of bonds:

Junior debt versus senior debt and equity

Today’s environment makes it very difficult for income-seeking investors to obtain safe returns. Cash deposits give close to zero interest. Investing in subordinated bonds of high-quality companies can pro-vide this return, whereas equities can disappoint. For example, in the case of BHP Billiton, a major global commodity producer, the dividend was cut and the shares fell sharply. The chart below shows the price movements of the shares versus the subordinated debt, which was issued in October 2015.

While investing in subordinated debt has always been rewarding, its higher income was more marginal. Today, however, subordinated debt pays a multiple of senior debt. This means that the same capital can realise maybe three times as much income annually, which makes a huge difference for income-seeking institutions or individuals.

BHP Billiton shares vs. subordinated debt

Source: Bloomberg; 16/10/2015 to 29/04/2016

Source: Bloomberg; 16/10/2015 to 29/04/2016

Buffer against rising rates

But what happens if interest rates go up? It depends, as the terms of each issue of subordinated debt can be very different, but there are three main types. First, the examples above relate to so-called fixed-to-floating securities. The interest is fixed periodically, based on a certain spread above prevailing generic rates. Therefore, the interest rate risk exposure is limited to the time until reset, generally five to 10 years. Second, there are bonds with fixed rates into perpetuity, where there is indeed a risk of being stuck.

However, with yields on high-quality fixed-rate bonds above 6% in US dollars and sterling or 5% in euros, interest rates would have to go up a lot for that to become a problem. Third, there is subordinated debt that is floating rate and trades at a big discount. For example, floating rate note debt of HSBC pay-ing a small margin over Libor can be bought for just 54%. When interest rates go up, this can generate capital gains, and even when interest rates do not go up companies have been known to re-purchase these bonds at 15–20 percentage points premiums to the market price, as Standard Chartered did in March this year. For those worried about the future path of interest rates, it can help to diversify across a mix of fixed-rate, fixed-to-floating and discounted floating rate notes.

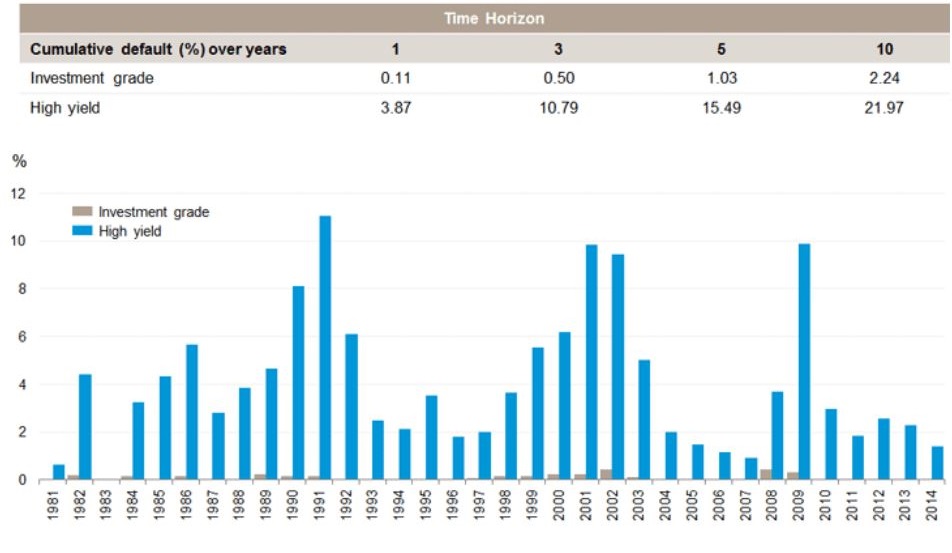

Low default risk for investment grate companies

While subordinated debt will always pay a premium over senior debt, it bears an extra risk. The above examples are the subordinated debt of high-quality investment grade companies. While we conduct our own fundamental analysis to judge whether they are good companies in which to own the debt, we can also be comforted by the investment grade ratings given to the companies’ senior debt by rating agen-cies, even if the subordinated debt is rated lower. Statistics show in the table below that the occurrence of bankruptcies among investment grade-rated companies is much lower than for high yield companies. And as long as they are not in distress, the subordinated coupons will be paid.

Global corporate average cumulative default rates (1981-2014)

Source: Standard & Poor’s Global Fixed Income Research and Standard & Poor’s CreditPro as at 30 Apr 2015

We believe that this is a particularly good time for investors who are after steady income to be investing in the subordinated debt of investment grade companies. However, it is important to keep in mind that each issue is different and requires careful analysis of the terms of the issue.

Anthony Smouha , June 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |