| https://www.next-finance.net/en | |

|

Strategy

|

Financial markets in 2016: From the « 3D » to the « 3R », a shift in market paradigm – is it going to last?

Three forces collided at the turn of 2015-2016 to make markets extremely anxious. First, the Fed stuck to its promise to start a tightening cycle in 2015, with an in extremis hike in December 2015. The accompanying “dot plot” priced in four more hikes for 2016.

Article also available in :

English ![]() |

français

|

français ![]()

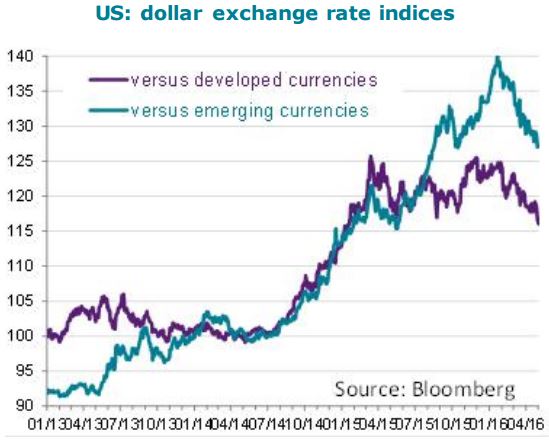

The Fed was then setting itself on a divergent path from the rest of the central bank community, where more negative rates and more QE were in order. The FOMC was clearly taking the risk to see the dollar appreciate rapidly in the context of a global currency war everywhere else in the world.

Second, the Chinese leadership seemed to have taken the tough decision to stop the debt -fuelled blind-run in their economy, and go down the road of painful restructuring, with potential Renminbi devaluation as a safety valve. The Fed-induced strength in the dollar and the Chinese deleveraging coalesced into a deflationary spiral on commodity prices, compounded by the decision of Saudi Arabia to enter into an all-out price war with Iran, Russia and US shale oil producers. Divergence in monetary policy, Deleveraging of the Chinese economy, Deflation scare fuelled by commodity prices, such was the toxic “3D” cocktail that sent equity markets in a tailspin at the beginning of the year.

As we pointed out from the beginning of the year, we did not believe that the Fed would stick to its “dot plot” rate path due to the incipient slowdown in US domestic demand. The macroeconomic newsflow confirmed our view: the US economy grew by a mere 0.5% in Q1, as investment remains in negative territory, destocking continues and the trade balance deteriorates. The tightening in bank credit conditions and the ebbing flow of profits means any rebound from Q1 should be short -lived. In coming months, the slowdown in job creations, a lagging indicator, should convince investors that the tide has clearly turned for this cycle. The Fed has de facto taken stock of this counter-performance, and chances are we do not see any rate hike before this Autumn’s presidential election. The market has preceded the Fed in the adjustment in its “dot plot” by leaving in the dollar curve only one rate hike for the year. Conversely, the ECB and BoJ abandoned their intentions to send policy rates deeper into negative territory, the former due to strong German opposition, the latter due to the disastrous impact on bank and JGB liquidity (see my last two posts on Japan). As a result, the dollar has reverted its ascending path.

In China, the economic policy U-turn is even sharper. The unreliability of Chinese statistics makes it even harder to follow the thought process of the Chinese leadership, but it seems the politburo got scared by the incipient increase in joblessness in the North-East “rust belt”. Consequently, far from tightening the financial constraint on over-indebted segments of the economy, the Chinese leadership unleashed a tsunami of new bank loans on an already over-indebted economy. Some defaults have been tolerated, but the mind-blowingly high flow of new bank credit suggests the politburo is ready to keep the army of “zombie SOEs” alive and well for now .

The perverse effects of this re-leveraging were not long in coming: house prices skyrocketed again in large cities, while a new “casino” market emerged for the excess savings of Chinese households and companies: the futures market for commodities.

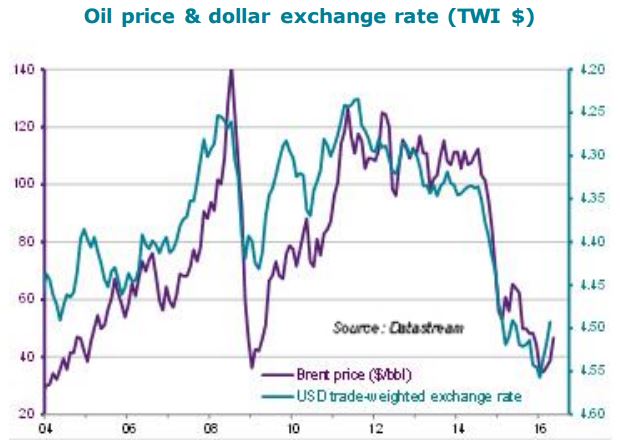

A weak dollar and Chinese speculative demand reverted the downward trend in commodity prices globally. The oil market was the most responsive to the new macroeconomic context. Oil prices even shrugged off the collapse of talks on an oil production freeze between OPEC and Russia in Doha. Thus, the “3 Rs” of monetary policy, Reconvergence, Chinese Releveraging and commodity price Reflation, led to a return of risk appetite on financial markets, particularly on emerging market assets (equity, debt, forex).

Is this new market paradigm going to last? We see several reasons to remain skeptical. First of all, the weakening trend of the dollar could be halted by the woes such trend inflicts on some trade partners of the US economy. Obviously, the biggest losers of this new environment are clearly the oil-importing countries against which the dollar is depreciating, chiefly Japan and the euro area. In the euro area, the euro has appreciated beyond the informal “line in the sand” of 1.15 to the dollar, which used to trigger verbal intervention by ECB speakers. But the ECB is running low on ammunitions to weaken the euro: the Germans have clearly indicated to Mr Draghi that a further rate cut is out of the question. The euro could thus continue to appreciate way beyond 1.15. Domestic demand seems robust enough to stomach such a rise in the short-run, but a renewed slowdown in H2 2016 could re-awaken some political risks likely to scare off markets again (Italian referendum in October 2016, French and German elections in 2017). In any case, if economies of the euro area are likely to suffer in silence in the short-run, a rising euro could weigh negatively on the relative performance of the equity market.

In Japan, the situation seems more dangerous in the short term. The sharp appreciation of the yen threatens to send the economy back into recession, at a time when the BoJ runs out of stimulating bullets. In addition, the US Treasury has issued a warning that, along with Germany, China, Korea and Taiwan, Japan should expect that any policy move to weaken its currency would be met with retaliatory measures by the US government. At a time when the TPP ratification lies in the balance, this is a powerful injunction. Japan might instead enact a new fiscal package, but this will further deteriorate the country’s public finances. A crisis of confidence in the yen could result, although this seems like a distant prospect as long as households continue to exhibit a very high preference for yen-denominated liquid assets. The end game for the unsustainable Japanese public debt could still be years away, but, as in the euro area, the equity market might continue to suffer from an appreciating yen.

What could then derail this market configuration in the short run? A weakening dollar and a rising oil price are likely to bring solace to the embattled manufacturing and energy sectors in the US. Would this be enough to reconcile the Fed with its tightening plan? We doubt it, as the causes of the current slowdown run deeper than the manufacturing lull. Corporate leverage has returned to pre-crisis levels, and banks and credit market alike have taken notice. They will impose higher premiums for corporates willing to continue the vicious game of piling up debt in order to pay for dividends and share buybacks. In addition, households remain cautious in their spending behavior (stable savings rate), despite the loosening in credit conditions (credit card, mortgages), and they are already expecting a slowdown in their earnings. There is little chance, in our view , that a possible cyclical “sweet spot” would lead the Fed to change its ultra-prudent stance.

The oil market could be the first to change course. As we approach the 45-50$/bbl range, we believe that some marginal players in the shale industry will restart drilling. This range coincides with the breakeven price for some well-positioned players, and we must keep in mind that the reaction time in the shale industry is a matter of months, not years or decades as in the conventional oil business. Saudi Arabia would not tolerate to lose more market share to the tight oil complex, and would probably increase its production to chase them out of the market again, through a weaker oil price. The kingdom has indicated that it was willing and able to increase its production by 1 million bbl/d in short order if need be.

At the end of the day, the biggest and most immediate threat to the “3R” paradigm lies in China. In our opinion, Chinese leaders have learnt their lesson last summer when they witnessed the devastating effect of the bursting of the equity bubble. They have also studied with angst the precedents of massive real estate bubbles in Japan and in the US. So they know the dangers of credit-fueled asset bubbles, and it seems dubious they would tolerate the inflation of a new bubble of real estate and commodities. We are likely to see some tightening measures aimed at cooling down the sector, followed by some new targeted stimulating measures – i.e. a succession of very short-term stop-go cycles. The next “stop” phase could not be far away when we see the explosion of transaction values on the housing market (+70% yoy).

This is why we believe that the oil and China factors of the rally have weak foundations, and are skeptical that the rally in risky assets can last in its current configuration. We are long equity, commodities and emerging assets, but each time with a bias in favor of the lower beta: we prefer developed to emerging equity, we prefer emerging debt to emerging equity, gold to oil in the commodity complex.

Raphaël Gallardo , May 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |