| https://www.next-finance.net/en | |

|

Opinion

|

Fed: The Art of Evasion

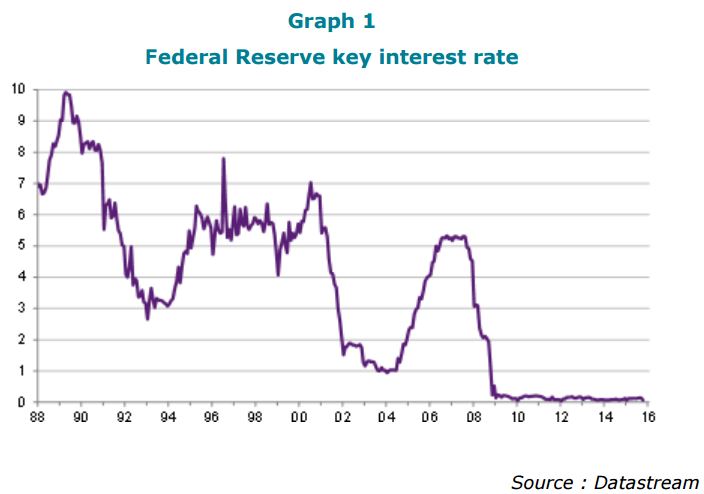

The US Federal Reserve maintained a status quo on its interest rates at its September meeting, thereby extending a period of zero interest rates that has lasted for virtually seven years already. This decision, which ought to have reassured investors, was on the contrary greeted with further significant equity market falls.

Article also available in :

English ![]() |

français

|

français ![]()

The US Federal Reserve maintained a status quo on its interest rates at its September meeting, thereby extending a period of zero interest rates that has lasted for virtually seven years already (Graph 1). This decision, which ought to have reassured investors, was on the contrary greeted with further significant equity market falls. Investors were frightened by the Fed’s press release explaining its decision to the markets. The Fed there referred to "global economic developments" likely to weigh on US growth and inflation. The hint at the Chinese equity market crash and the micro-devaluation of the yuan is clear. This emphasis on emerging risks as pretext to keep a status quo convinced the markets that US growth was, according to the Fed’s best assessment, more vulnerable to external shocks than expected.

Janet Yellen, the Fed Chair, made an effort to qualify this message the following week, by underlining that at this stage the emerging-country crisis is not threatening US growth, but only inflation via the low level of imported goods prices (commodities, industrial goods imported from emerging countries with weakened currencies). As a result, despite the solidity of real growth, the risk of imported disinflation justifies taking out insurance on the stability of longterm inflation expectations. To do so, inflation prospects should be stimulated in the medium term by temporarily pushing the economy into overheating. According to this approach, the impact from imported disinflation on headline inflation is offset by high inflation in the prices of goods produced locally.

Janet Yellen nevertheless stressed that she and majority of her FOMC colleagues expected a rate hike this year. The Fed has thereby tied its own hands, as only downright disappointing inflation figures could enable it to once again delay the rate hike without sparking panic in the markets.

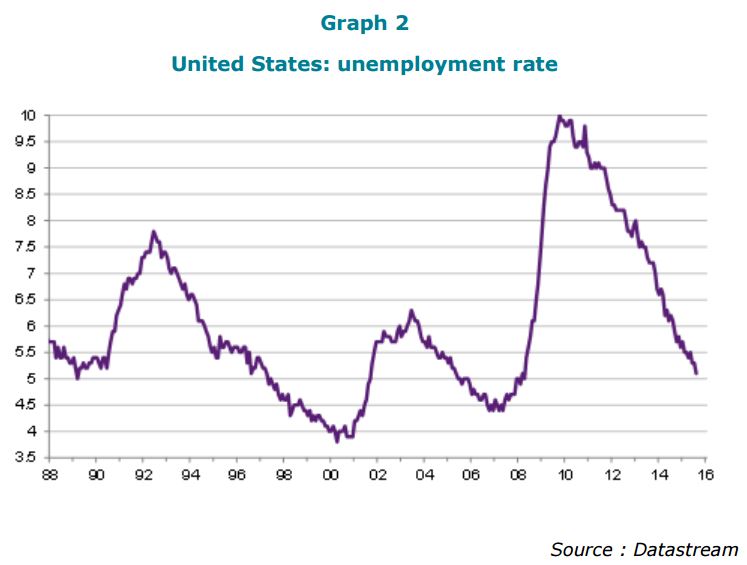

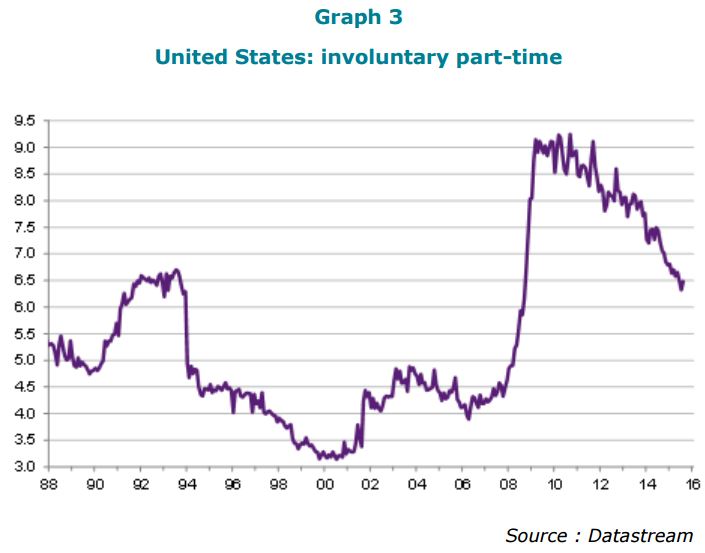

But that is not the most dangerous risk of this “temporary overheating strategy”. In our opinion, the danger is that it assumes that the central bank is able to fine-tune the economy, which is to a large extent unrealistic. Admittedly, the unemployment rate can be driven lower than its equilibrium rate without fear of a wage surge, because of the still significant presence of involuntary part-time workers in the labor force (Graphs 2 and 3).

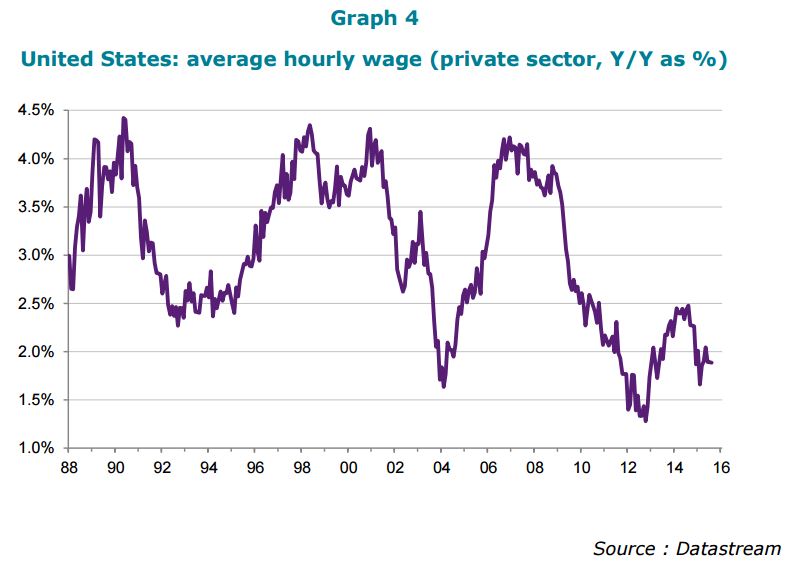

This population is a labor reserve that companies can draw on to increase the number of hours worked without increasing the hourly wage. But as soon as this "reserve army" is exhausted, employers must attract to the labor market persons whose reservation wage (the wage at which they accept to take a job) until now has been higher than those offered. As a result, the ongoing fall in unemployment will generate noteworthy wage increases (Graph 4). Given the structural weakness of productivity gains, companies will then have the choice between passing this increase in labor costs on to the final consumer in the form of final price inflation or dampening it by reducing their margins.

In the first case (increase in final prices), the Fed will, accordingly, be faced with a rapid rise in domestic goods inflation. While the Fed’s goal is to let this inflation component rise above its 2% target to offset imported disinflation, this suggests that the overheating then will be well entrenched in the labor market. If it does not want inflation expectations to soar under the effect of a wage-price spiral, the Fed would therefore have to make a U-turn in its policy and carry out a rapid rate hike. If it balks at this, it is the bond market that will cool down the machinery thorough a surge in long-term interest rates. Such an interest rate shock, whether initiated by the Fed or the bond market, might trigger an equity market crash. The markets could even expect this reaction, which could create detrimental volatility for the intermediate maturities of the yield curve.

In the second case, it is companies’ margins that would be reduced, leading to declining profitability and investment as well as a risk to market valuations. We believe the latter financial aspect of the reasoning is particularly sensitive in the current situation. As we have often seen, the valuation levels of a number of asset classes show an end-of-cycle shape - at a time when the monetary normalization cycle has not even started. Continued monetary laxity by the Fed would encourage investors to inflate these valuations even more, and they would therefore be all the more vulnerable to the future interest rate shock that Yellen’s strategy promises in her statement.

Does the Fed really believe in this risky monetary U-turn strategy? Or is it quite simply seeking to hide its own doubts behind vague statements? There are doubts about its ability to protect the US against the adverse winds blowing from Asia. There are doubts about its ability to obtain even a semblance of monetary normalization in a growth cycle that is already fading in some respects (stock, private debt, market valuations). Unlike in 2004, when the Fed’s previous policy tightening cycle started, a monetary cycle deployed in today’s situation would not be dampened, but, on the contrary, exacerbated by the effects of the financial cycle (tightening of lending conditions, contraction in stock multiples) and the currency cycle (steep appreciation of the dollar in a context of a currency war). The Fed is completely aware of this. It is getting trapped in its own contradictions, and markets in search of direction would be wrong to expect more transparency in its words, except the promise of persistently high volatility.

Raphaël Gallardo , October 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |