| https://www.next-finance.net/en | |

|

Strategy

|

EZ deflation risk not deterring buyers of inflation in primary

The strong demand in the primary market confirms what is already well known: whatever the inflation expectations, there is significant structural demand, notably from “buy and hold” investors such as pension funds, for bonds indexed to inflation.

Article also available in :

English ![]() |

français

|

français ![]()

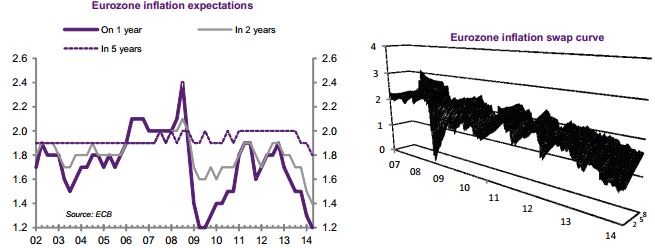

In the Eurozone, the deflation risk is now being considered officially by the European Central Bank. It stems notably from the price expectations mechanism. Whether it be at the level of the markets (breakeven inflation rates, forward inflation, etc.) or of the economic agents, inflation expectations are heading in the wrong direction, even though as yet the 5Y5Y inflation forward is managing to hold at 2%. Q1 2014 GDP, which was disappointing in several countries, notably France and Italy, has of course strengthened deflationary expectations.

Actual inflation is weak everywhere. It reaches only 0.4% in Spain, while at the level of the Eurozone it sits at 0.7%. Yet, this did not discourage the Spanish Treasury from issuing at the start of the week its first ever Bono indexed to European inflation, the Bono 1.8% Nov 2024. This auction was a success, with bids totalling EUR 20bn for EUR 5bn placed. The new 10-year linker attracted particularly strong demand from non-resident investors, notably from French investors (21%) and British investors (15%). Part of this success may, of course, be due to the price at which the paper was placed (against nominal and against BTP€i). The initial objective for the breakeven was 1%, but it ended up higher.

When it comes to arbitraging, the addition of a new European linker is a good thing. It is positioned in a segment of the European curve that is already crowded with Italian, French and German papers. Investors seeking protection against inflation and reaching for yield may obviously be seduced by this new linker. Its real yield exceeds 1.8%, which is significantly more than the 1.31% yield offered by a nominal German bond with the same maturity.

The strong demand in the primary market confirms what is already well known: whatever the inflation expectations, there is significant structural demand, notably from “buy and hold” investors such as pension funds, for bonds indexed to inflation.

Strategy: play convergence of the new linker’s breakeven towards the breakeven of its direct competitor, the BTP€i 2024, then that of the equivalent Bund€i.

René Defossez , May 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |