| https://www.next-finance.net/en | |

|

Strategy

|

Equities vs. high yield ? The answer becomes clearer…

During the initial phase of the turnaround in high-risk American assets, equities and high yield moved very similarly. In contrast, since mid-2012, equities have been accelerating more quickly, outpacing the credit market by a decent margin.

Article also available in :

English ![]() |

français

|

français ![]()

This trend is less noticeable on the graph, yet over the past few weeks of trading,

equities and high yield have even moved in opposite directions, since the S&P 500

continued to climb while America’s Citigroup high yield market index recorded a

few declining sessions.

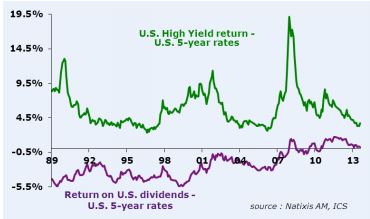

Two explanatory factors can be forwarded. The first is likely to be connected with valuations. On the one hand, the return on stock dividends offers a consistently more attractive remuneration than 5-year U.S. government bond rates, as underscored by the upward trend in this spread.

On the other hand, the same spread for private bonds is seen to be continuously narrowing, albeit in positive territory, which constitutes the very definition of high yield. We’re also observing that the 3% level of spread is often the point where this value has historically rebounded and would seem to form a floor that’s difficult to penetrate. Moreover, a rise in bond rates would be proportionately applicable on both spreads, yet its mathematical effect would be negative and certain, whereas its effect on stocks would remain uncertain.

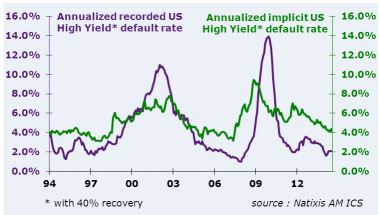

The second explanation is likely to be found in companies’ intrinsic value.

From this perspective, the implicit high yield default rate stemming from the instantaneous return of this asset class protects against a rise in the actual recorded default rates.

These rates are undoubtedly at their minimum levels, though we can still notice that the discrepancy between implicit and recorded has held, and the market has not taken advantage of the limited number of U.S. corporate bankruptcies to lower the return on private bonds by more than a proportional amount.

Nonetheless, another element is disturbing companies’ fundamentals, with a significant increase in debt. As a matter of fact, while the amount of accumulated debt had leveled off during the 2007-2008 crisis, its growth has taken off at a good pace since then, especially over the past few years.

This re-leveraging of balance sheets may worry the markets at some point when the issue of raising rates in the U.S. returns to the fore and when the unfavorable spread for U.S. government bonds hits a historically low level as we’ve already witnessed.

Obviously, it’s still too early to draw any conclusions on the divergence of these two markets, but high yield will need to be closely monitored, given that it remains less liquid than the equity markets.

During a correction, investors might feel trapped and wind up accelerating this decline by running for the exits at any price.

Franck Nicolas , July 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |