World’s largest institutional investors expecting more asset allocation changes over next two years than in the past

Institutional investors worldwide are expecting to make more asset allocation changes in the next one to two years than in 2012 and 2014, according to the new Fidelity® Global Institutional Investor Survey.

Article also available in :

English ![]() |

français

|

français ![]()

Institutional investors worldwide are expecting to make more asset allocation changes in the next one to two years than in 2012 and 2014, according to the new Fidelity® Global Institutional Investor Survey [1].

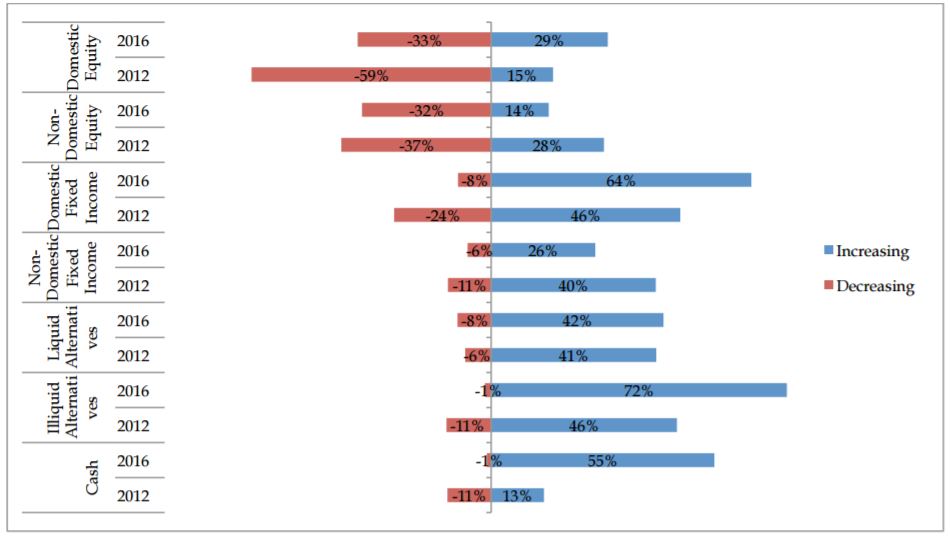

The survey, which includes responses from 933 institutions in 25 countries with US$21 trillion in investable assets, found the most significant anticipated shifts are within alternative investments, domestic fixed income, and cash. Globally, 72 percent of institutional investors surveyed say they will increase their allocation to illiquid alternatives in 2017 and 2018, 64 percent to domestic fixed income, 55 percent to cash and 42 percent to liquid alternatives.

Growing popularity of illiquid alternatives is particularly prevalent in the UK, with 92 percent of institutional investors saying they will increase their allocation within the next two years, up from 46 percent in 2012. Within domestic fixed income, 87 percent of UK investors expect to increase their allocation, up from 38 percent in 2012 and 74 percent expect to raise their cash positions, up from just 12 percent in 2012.

Graph 1: Expected asset allocation changes (global responses) [2]

Primary concerns for institutional investors

Overall, the top concerns for institutional investors are a low-return environment (28 percent) and market volatility (27 percent). These anxieties have heightened since 2010, where only 25 percent of survey respondents cited a low-return environment as a concern and 22 percent cited market volatility.

The survey revealed investment concerns vary according to the institution type. Globally, sovereign wealth funds (46 percent), public sector pensions (31 percent), insurance companies (25 percent), and endowments and foundations (22 percent) are most worried about market volatility. However, a low-return environment is the top concern for private sector pensions (38 percent).

Continued confidence among institutional investors

Despite their concerns, nearly all institutional investors surveyed (96 percent) believe that they can still generate alpha over their benchmarks to meet their growth objectives. The majority (56 percent) of survey respondents says growth, including capital and funded status growth, remain their primary investment objective, similar to 52 percent in 2014.

On average, institutional investors are targeting to achieve approximately a 6 percent required return. On top of that, they are confident of generating 2 percent alpha every year, with roughly half of their excess return over the next three years coming from shorter-term decisions such as individual manager outperformance and tactical asset allocation.

Improving the Investment Decision-Making Process

Nearly half (46 percent) of institutional investors in Europe and Asia have changed their investment approach in the last three years, although that number is smaller in the Americas (11 percent). Across the global institutional investors surveyed, the most common change was to add more inputs – both quantitative and qualitative – to the decision-making process.

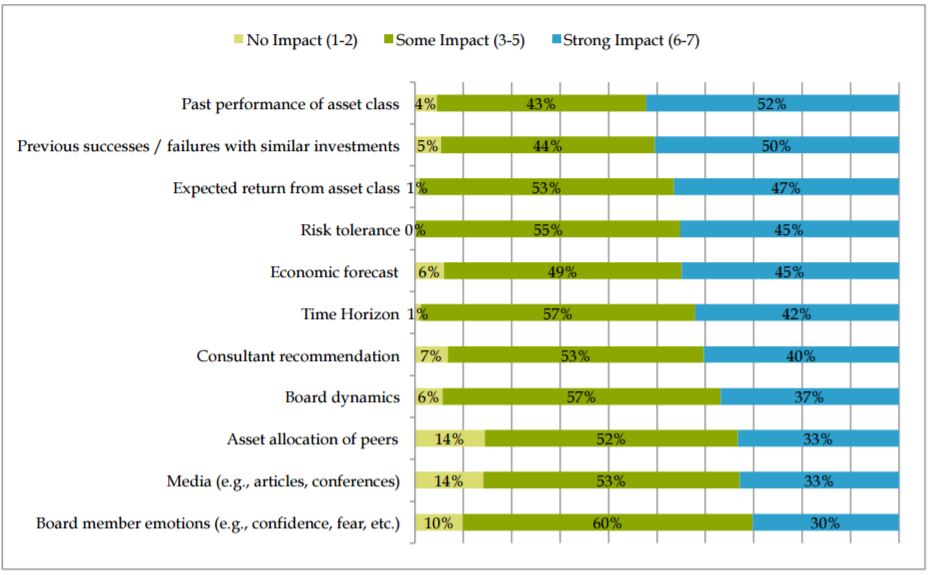

Graph 2: Factors impacting institutions’ asset allocation

Focusing on qualitative inputs, at least 85 percent of survey respondents say board member emotions (90 percent), board dynamics (94 percent), and press coverage (86 percent) have at least some impact on asset allocation decisions, with around one-third reporting that these factors have a significant impact.

Heather Fleming, Head of Institutional Distribution for UK and Ireland at Fidelity International, said: “The research shows that institutions are managing their portfolios in a more dynamic manner, making more investment decisions today than they have in the past. However, with increasing quantitative and qualitative influences on each investment decision, institutional investors may be about to face an information overload.

“To keep up with the overwhelming amount of data, institutional investors should consider evolving their investment process. A more disciplined investment process may help them achieve more efficient, effective and repeatable portfolio outcomes, particularly in a low-return environment characterised by more expected asset allocation changes and a greater global interest in alternative asset classes.”

Next Finance , December 2016

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] Fidelity Institutional Asset Management conducted its survey of institutional investors in the summer of 2016, including 933 investors in 25 countries (174 U.S. corporate pension plans, 77 U.S. government pension plans, 51 non-profits and other U.S. institutions, 101 Canadian, 20 other North American, 350 European, 150 Asian, and 10 African institutions including pensions, insurance companies and financial institutions). Assets under management represented by respondents totalled more than USD$21 trillion. The surveys were executed in association with Strategic Insight, Inc. in North America and the Financial Times in all other regions. CEOs, COOs, CFOs, and CIOs responded to an online questionnaire or telephone inquiry.

[2] Responses of “no change” and “do not use asset class” are not shown above. 2016 results use expected changes for hedge funds and private equity as proxies for liquid and illiquid alternatives, respectively. 2016 Canadian results use global equity, domestic core fixed income and investment grade corporate as proxies for non-domestic equity, domestic fixed income and nondomestic fixed income, respectively

Focus

Note EURO STOXX 50® Index implied repo trading at Eurex

This research paper focuses on the inseparable relationship between implied repo rates and equity index total return swaps. Written by Stuart Heath, Director Equity & Index R&D at Eurex, it covers the various aspects and calculations of both repo rates and the (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |