| https://www.next-finance.net/en | |

|

Opinion

|

Why we would start reweighting U.S. stock-pickers

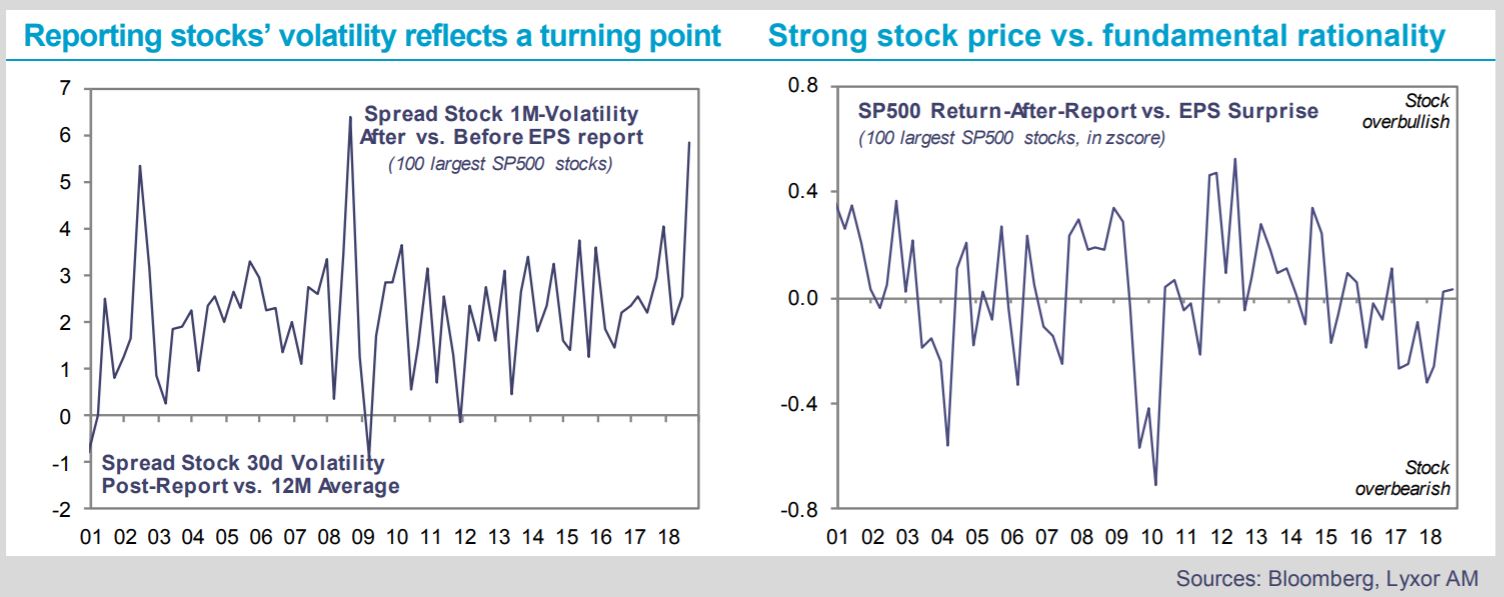

We are past the peak of the U.S. earnings reports. In the past, any unusually high individual stock volatility after an earnings announcement was a pattern that only appeared at macro inflection points.

Article also available in :

English ![]() |

français

|

français ![]()

The Q3 season tells us that any additional growth from the tax reform is now behind us and that corporate America is back at cruise level. The share of earnings beats, the size of surprises, guidance and next year’s expectations have all reverted to their long-term average.

After a rough start to the season, when any earnings disappointments were severely sanctioned, prices then became increasingly consistent with the stock’s fundamentals, i.e. a key pattern for managers who need prices to reflect the fundamentals they pick stocks for.

Meanwhile, increased dispersion at stock and sector levels, and moderate correlations would also provide a variety of arbitrage opportunities. These should emerge after the dust settles, when stock trends reshape again. More reasonable earnings expectations would also lower the hurdle. U.S. equities also showed a wider sector leadership, with cyclicals matching tech stock contributions.

These improvements are not a coincidence in our view. They come at a time when the U.S. economy is probably peaking, thus curtailing market directionality. The effects of the Fed’s hiking cycle are starting to be felt, with increased discounted cash flows and leverage differentiation. The fading impact of the tax policies should also allow, to some extent, sector and factor rotation to respond to traditional drivers (growth, rates, risk on/off etc.) rather than to transversal movers.

More arbitrage opportunities from low correlation, more fundamental stock differentiation, and greater price rationality, a reset for most equity trends, are all key ingredients for stock-pickers.

This is not to say the alpha environment is ideal yet. For now, a majority of L/S Equity managers have shrunk their cyclical exposure overall, and would only partially benefit from a rally, if any. Moreover, further political uncertainty is still a major alpha issue, in particular trade tensions, which are likely to unsettle stock-picking opportunities for a while. With these nuances in mind, we are considering reweighting U.S. stock-pickers.

Lyxor Research , November 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |