| https://www.next-finance.net/en | |

|

Pedagogy

|

Using Risk Premia for a true diversified portfolio

For investors seeking meaningful diversification of their portfolios, alternative beta strategies (sometimes called liquid risk premia) have low or no market beta and, if executed correctly, have low correlations to the major asset classes.

Article also available in :

English ![]() |

français

|

français ![]()

Based on academic research spanning nearly 40 years, alternative beta strategies (or liquid risk premia) offer institutional investors a practicable solution to the problem of where to find uncorrelated returns. Alternative beta represent return streams associated with systemic characteristics (or factors) embedded in the markets. Unlike traditional betas, alternative betas are accessed through non-traditional investment strategies, such as rules-based long/short, relative value, arbitrage, and the like. Alternative betas are available across asset classes – including equities, fixed income, credit, currencies and commodities. They exploit a large number of different anomalies – such as size and value for equities, momentum for all asset classes, and carry (holding two offsetting positions) for fixed income, credit, currencies and commodities. The result is portfolios that can provide meaningful diversification for institutional investors.

How to access alternative betas

Alternative betas can primarily be accessed in two ways. First, a counterparty can systematically manufacture an index that captures a specific risk premium, which can then be purchased via a swaps contract. To design an index to capture the value-equity risk premium, for instance, a counterparty would take an index such as the MSCI ACWI, rank the securities within the index by a valuation metric such as price-to-book, and then go “long” the top quintile of cheapest stocks and simultaneously go “short” the bottom quintile of the most expensive stocks. The three quintiles of stocks in the middle are not used. This structure extracts the value premium and seeks to remove any market beta exposure. These rules-based indices can be structured as daily liquidity vehicles, which are relatively inexpensive, and offer full transparency to the underlying positions.

Alternatively, an asset manager can develop their own indices to gain access to alternative betas, using their internal quantitative research teams. Either method needs to focus on capital efficiency and low cost. Asset owners/allocators looking to access alternative betas may find the most effective way to access the asset class is to hire an asset manager with specialist expertise. Selecting the most appropriate and effective alternative beta structure is one important element in deriving ultimate benefit from the strategy. Equally, if not more, crucial, is the portfolio construction of multiple exposures. Given their low correlation to one another alternative betas are most powerfully employed in multi-position, multi-asset class portfolios. The methodology utilized to weight these multi-exposures over time differs among providers and is often the primary determinant of investment success.

Smart beta

A contrasting approach using similar techniques is smart beta. Smart beta is a long-only construct also focused on extracting risk premia, or risk factors. Because smart beta strategies employ long-only techniques, they typically carry more general market directionality in their profile. They also target relative returns and are more highly correlated with the major asset classes. By contrast, alternative beta strategies, when done well, seek to generate market neutral absolute returns, uncorrelated with the major asset classes.

Alternative betas themselves tend to be uncorrelated with one another, leading to low or negative beta to traditional directional asset classes. Based on our internal research looking at the returns of a diversified basket of alternative betas, the correlation of their return to each other, and to the market overall is very low – an average of 0.05. [1] (For the period March 31, 2003 – December 31, 2015. Source: Columbia Threadneedle Investments). This low average is the result of multiple negatively-correlated relationships, which makes alternative betas extremely powerful portfolio building blocks and provides a very compelling story for any investor seeking meaningful diversification – especially when compared to a long-only smart beta approach.

Investor demand

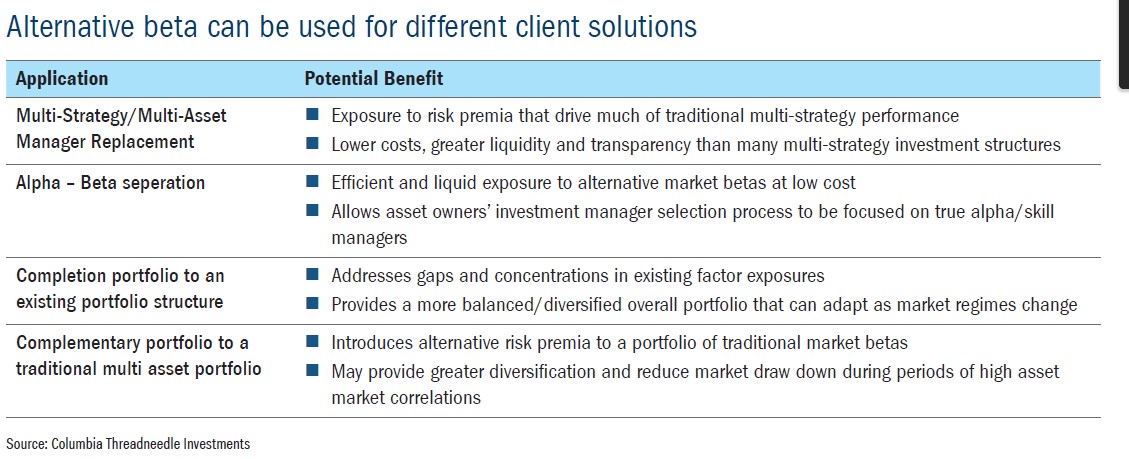

While this is still a relatively new investment approach, we have seen a few broadly-defined objectives emerge among investors who have demonstrated interest in alternative betas (see table below). These include: adding alternative betas to an existing alternatives allocation; replacing current, expensive, alternative investments that are delivering beta and pricing it as if it were alpha; and employing alternative betas to smooth out the volatility of an existing portfolio.

The Columbia Threadneedle Investments solution

At Columbia Threadneedle Investments, we are able to customise the profile of portfolios to meet most client needs. For instance, we can build standalone multi-strategy, multi-asset class portfolios, where all five asset classes and all of the long/short, arbitrage, and relative value structures are represented. We can also design portfolios to complement existing factor exposures – a “completion portfolio” – that seeks to balance concentrations and gaps that an investor may have in their existing portfolio. Because of the wide array of alternative betas to choose from, there is significant flexibility in building customized portfolios using alternative betas.

As investor understanding of alternative betas develops, we believe that the approach will likely become mainstream either in standalone form, as part of a diversified multi-strategy portfolio, or as a completion portfolio.

Meer informatie over onze alternatieve bètastrategieën vindt u op onze website columbiathreadneedle.fr

William Landes , October 2016

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] Correlation is scaled between +1 for assets that are perfectly positively correlated and -1 for assets that are perfectly negatively correlated

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |