US Energy infrastructure: The MLP example

Among infrastructure assets, energy infrastructure assets such as pipelines, storage facilities or processing plants, are experiencing a rapid growth, especially in the USA. Master Limited Partnerships (MLPs) have played a key role in facilitating investment in US energy infrastructure.

Article also available in :

English ![]() |

français

|

français ![]()

What is an MLP?

An Master Limited Partnerships (MLP) is a publicly traded partnership (PTP). Unlike a corporate stock, an MLP does not pay tax on their income and to qualify for an MLP structure, a PTP must have at least 90% of its income derived from « qualifying sources ». Most MLPs operate in the field of energy and natural ressources, especially in the energy markets (crude oil and natural gas) through exploration, development, production, processing, refining, transportation or storage for example.

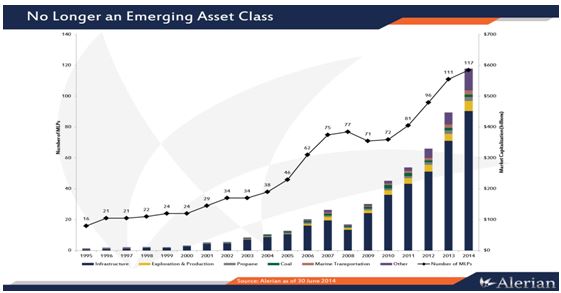

MLPs are listed on public exchanges such as the NYSE in the USA. Since 1995, the sector has seen a compound annual growth rate of 25% in market capitalization. As of June 30, 2014, there were 117 energy MLPs totaling over $500 billion in market cap.

Different types of activities

Energy infrastructure activities in the USA can be divided into three main areas:

Structure of a MLP

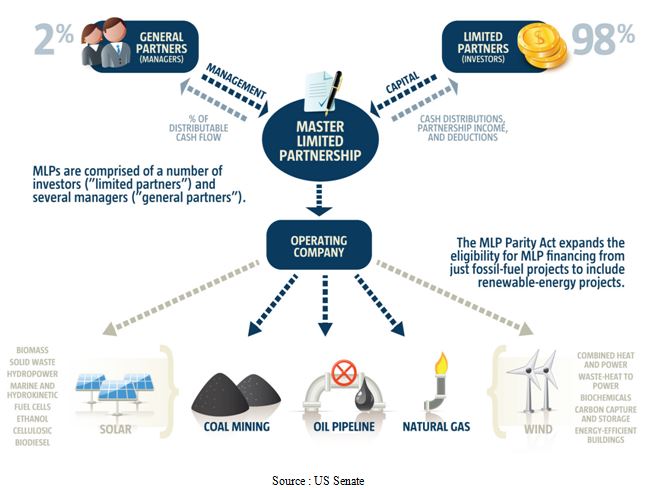

The ownership of a MLP is divided between the general partners (GPs) and the limited partners (LPs). The GPs manage the MLP and while the LPs only provide the capital and do not take part in the management of the MLP.

The LPs are initially entitled to receive the majority of the cash flow generated by the MLP. The cash flow available for distribution is allocated between GPs and LPs. The GPs typically hold 2% of the MLP equity but can grow its entitlement to the MLP profit margin through incentive distribution rights (IDR). The IDRs are calculated as a percentage of the cash distributed. As the distribution to LPs increases and reaches certain levels, the IDR increases as well and can represent up to 50% of the incremental cash flow available for distribution.

Key characteristics

Since the 2008 crisis, investors have become more cautious about market risk. In addition, with interest rates low, there has also been increasing demand for steady and stable yields. MLPs provide potential solutions to both of these needs.

According to Henry Boua, Associate Director for France and Monaco at ETF Securities, historically, MLPs have tended to show the following investment characteristics:

- Higher and more stable distribution yield than equities and bonds

- Higher total return relative to other asset classes over the past five years

- Better risk/return ratio than equities, bonds and commodities

- Diversification potential, as MLPs have a low correlation to bonds and a declining correlation to equities and commodities

- Inflation hedge characteristics

Over the past 10 years since June 30, 2004, MLPs have generated 392.4% on a total return basis, as compared to 176.3% for Utilities, 148.7% for REITs, 111.6% for the S&P 500, and 61.9% for Bonds. On an annual basis, this translates to 17.3% for MLPs, 10.7% for Utilities, 9.5% for REITs, 7.8% for the S&P 500, and 4.9% for Bonds.

As of December 31, 2013, MLPs averaged annualized returns of 18.3% for the past 10 years; yield has comprised 7% of the return, distribution growth represented around 7%. Going forward, industry expectations for MLPs are yields around 5%-6% and distribution growth of 4%-8%.

Markets drivers and risks

The US energy landscape has altered dramatically in recent years as technological advances have allowed access to previously unrecoverable shale oil and gas, and oil-sand reserves. As energy production in the USA would increase in the coming years, there is huge expected growth in infrastructure spending ahead.

“Risks to MLPs growth may come from a potential change in the regulations, the controversial reward system using IDR, MLPs exposure to market prices (interest rates and commodity) and extreme weather conditions or terrorism that can damage their business” warns Henry Boua, Associate Director for France and Monaco at ETF Securities.

Next Finance , October 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Note EURO STOXX 50® Index implied repo trading at Eurex

This research paper focuses on the inseparable relationship between implied repo rates and equity index total return swaps. Written by Stuart Heath, Director Equity & Index R&D at Eurex, it covers the various aspects and calculations of both repo rates and the (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |