| https://www.next-finance.net/en | |

|

Opinion

|

Trade war concerns unsettle financial markets

While the US macroeconomic data flow last week was on balance broadly in line with expectations, euro area data surprised again on the downside intensifying concerns about a slowing economic momentum.

The US central bank hiked again by 25 bps on Wednesday, but the median dot for 2018 was unchanged. However, the dots for 2019 and 2020 moved up by 25 bps on average.

- The imposing of tariffs by the US administration triggered a shift in market sentiment last week. This led international equity markets lower and supported assets deemed as safe by investors. The expected key rate hike by the Fed on Wednesday was put in the background.

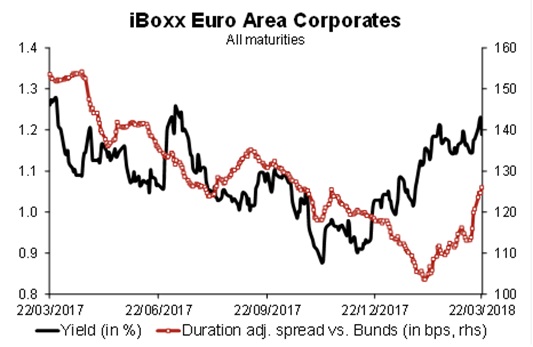

- The weakness of corporate bond markets continued last week. Meanwhile, (duration-adjusted) euro area IG corporate bond spreads are back to the levels of November. However, in light of the expected slowing of primary market activity, it is likely that corporate bond spreads will be able to recover moderately in the near term.

- With macroeconomic data releases unlikely to be particularly market moving this week, financial markets are expected to follow closely the future development on the trade war issue.

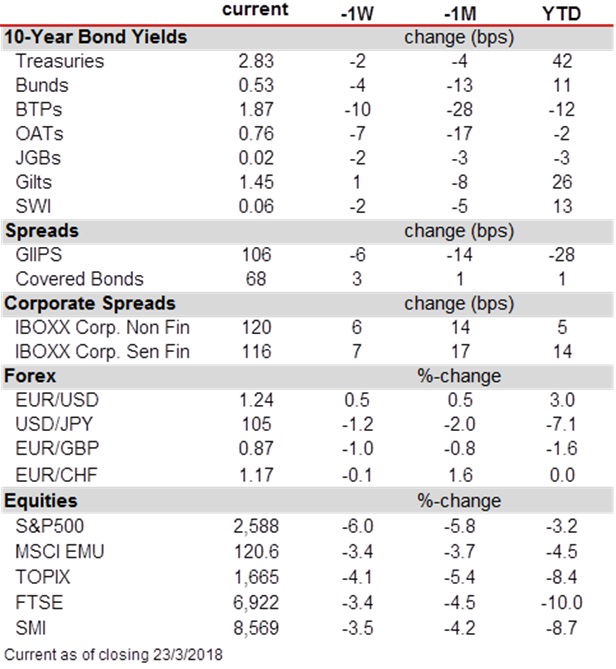

Though, headlines last week were dominated by escalating concerns about a trade war. The US administration decided to impose tariffs aimed at China. The prompt retaliation triggered a strong rise in risk aversion on financial markets. On balance, the MSCI EMU fell by 3.4% and the S&P 500 even dropped by 6.0%. The accompanying flight to quality triggered lower euro area core yields, particularly at the long end of the curve (30-year Bund yields down by 5 bps). In contrast, the upbeat economic assessment of the Fed helped to keep the US yield curve almost stable compared to one week ago. In effect, the transatlantic yield spread reached new long-term highs across all maturities last week. Credits could not escape the increased risk aversion and spreads widened significantly last week (by around 6 bps). However, euro area IG corporate yields only rose by 4 bps, thanks to the decrease in underlying yields.

Beside the factors mentioned above, we regard a strong primary market activity as the main reason for the weak performance of euro area IG corporate bonds. Since the start of the month, the duration-adjusted spread has increased by 16 bps to 128 bps. The net issuance will be on the highest level for at least two years in March. At the same time, fund inflows have turned into negative territory in February and weekly data show that this did not change in March. Although the ECB kept on buying, this combination burdened corporate bond markets over the recent weeks. However, as the fundamental situation is forecast to remain benign and primary markets are unlikely to keep up the issuance speed, we see scope for corporate bonds to recover moderately in the near term.

The macroeconomic data releases are unlikely to be market moving during this week. While financial markets will scrutinize data with respect to indications of a further loss of the economic momentum in the euro area, the focus will likely remain on the development of the trade conflict. While the short-term effects of the announced tariffs on growth are likely to remain muted, the impact on risk sentiment can be significant. What is more, a further escalation can trigger a deterioration of the economic outlook in the medium term. This would have a more noticeable and lasting impact on financial markets, too.

Florian Späte , April 2018

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |