| https://www.next-finance.net/en | |

|

Opinion

|

Tech roars up: can markets follow?

From a more fundamental perspective, as mentioned in past updates, we are convinced that technology adoption (be it automation, cloud migration or less straightforward technology trends, such as AI, big data, machine learning..) still has a long way to go in a multitude of end markets.

Article also available in :

English ![]() |

français

|

français ![]()

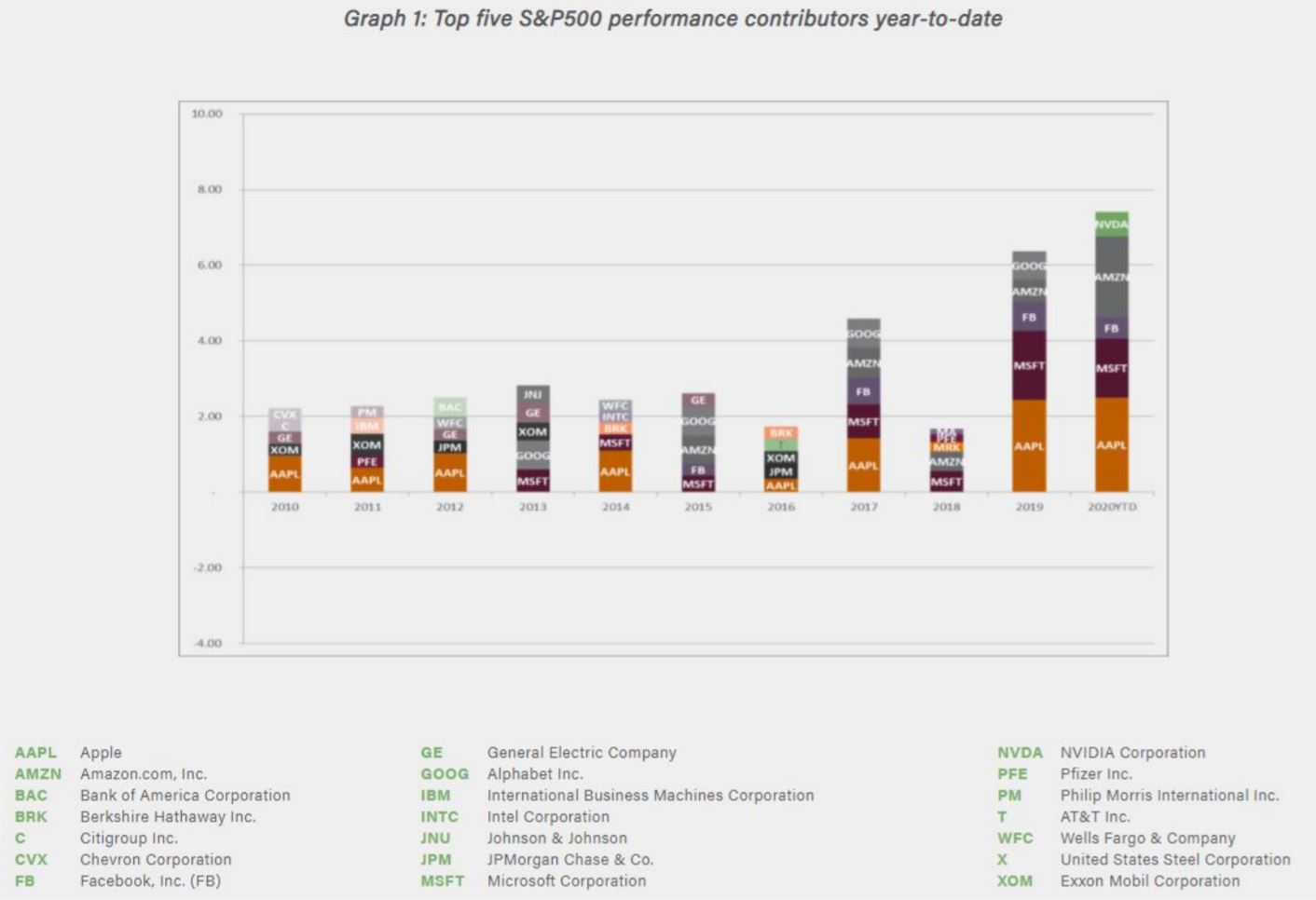

Since our last update from the beginning of July, equity markets in Europe have been flat-lining, while the S&P500 (in EUR terms) outperformed other major market indices till the end of August. During August, the FANG+ stocks (including Tesla and NVIDIA among others) jumped on average by a massive 20%. The polarisation of US stock markets has been going on over the last decade, with growth outperforming value. However, it has seen an accelerating trend in 2020 (with half of the last decade’s growth outperformance taking place in 2020), with a culmination phase during August. Another way to look at this polarisation trend is to calculate the top five S&P500 performance contributors year-to-date and compare it to the average contribution of the last 10 years. The performance contribution gap is approximately 4% points, and even higher than in 2019 (see graph 1).

Tesla was up an ‘electrifying’ 75% during the month of August, with its market cap nearing the aggregate market cap of all listed automobile OEM manufacturers. We were puzzled as to the fundamental reasons behind Tesla’s share price explosion (breakthroughs to be announced at its upcoming ‘Battery day’?, underestimated total available market beyond electric vehicles?) and have seen, in the meantime, a partial, but unsatisfying, explanation: a trebling in calls activity in big tech stocks (and thus including Tesla) since a couple of months, causing dealers to hedge and buy the underlying stock, magnifying the up-moves. Although Tesla has (for now) a competitive advantage in terms of battery technology or in-house software know-how to facilitate self-driving cars in the future, it will not annihilate the whole automobile sector (including other contenders such as Uber and Waymo). At the same time, it still has a lot to prove in adjacent areas (Tesla energy, insurance).

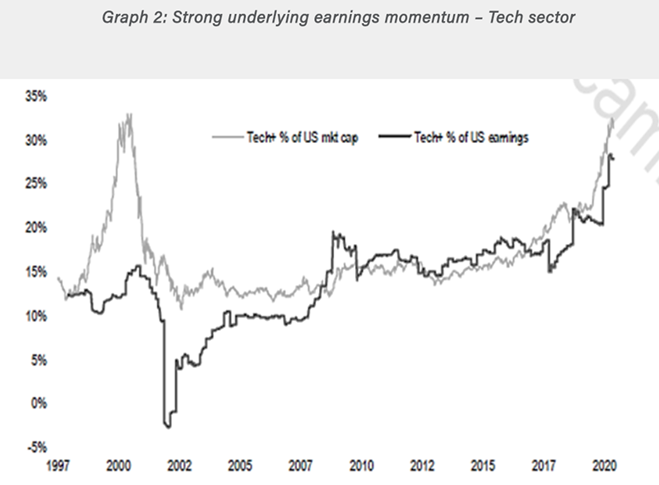

We acknowledge there are some areas of froth in the market (besides electric vehicle-linked companies, we would mention some recent software IPO’s). Still,we would refrain from making comparisons to the tech bubble of 2000. In terms of valuation, we highlight the strong underlying earnings momentum (see graph 2) of the Tech sector (IT and Communication services) and an average free cash flow (FCF) yield of 3.5% (due to its highest FCF conversion of any GICS1 sector), which is about in line with the market’s average.

A valuation exercise of these longer duration assets can obviously not be done irrespective of the interest rates and their future direction. With the Fed signalling last week it will not raise rates till Q4 2023 after adopting a new policy framework (allowing inflation to overshoot the 2% level) and our conviction that over the next couple of years inflationary pressures should be moderate (more on that below), one can expect long-term rates to remain subdued.

From a more fundamental perspective, as mentioned in past updates, we are convinced that technology adoption (be it automation, cloud migration or less straightforward technology trends, such as AI, big data, machine learning..) still has a long way to go in a multitude of end markets. The whole COVID crisis and ensuing lockdowns have only accelerated the trend, without any meaningful cannibalisation impact on the respective addressable markets in the future. Given the inherent scalability of most of these technology companies (especially software-related ones), adding sales comes at very low marginal costs. As a result, it enables fast margin progression and strong FCF generation. This also helps to explain the relatively higher price earnings ratio or price-to-sales multiples of some of these software companies, obviously provided that they are able to keep their competitive advantages.

Let us take the construction market as an illustration of an end market where digitisation is still in its infancy. Designing, planning and building an office building, with different parties involved (architect, contractor, subcontractors) is still mostly done with pen and paper. This causes substantial delays, cost overruns and wastage. With Building Information Management software, all these parties are digitally connected, helping to digitise in 3D the entire cycle of designing and building the office. Direct cost savings are substantial (around 25%) especially if construction projects are complex. However other indirect cost savings (project on time, less wastage) or benefits (think better energy efficiency of the office building) can be realised. The UK construction market is the furthest penetrated in Europe (25%) but some emerging markets like Brazil or China are only 2-3% penetrated. This example not only validates our point that technology adoption has a long leeway for further growth but also emphasises the deflationary forces caused by the same adoption. Other tech applications harnessing substantial cost efficiencies that come to our mind are precision farming, augmented reality (e.g. Hololens), machine learning and vision…

This brings us right at the heart of a key debate among market participants that has swelled in importance after the well-anticipated Fed’s new policy framework: inflation, its potential impact on different asset classes, and whether it could cause a major style rotation within equity. This participant is rather lukewarm on inflation spiralling higher over a relevant time horizon of 3-5 years. Although the size of the monetary and fiscal policy response to the pandemic is unprecedented (and will be sustained for the foreseeable future), there are strong disinflationary forces – on top of further tech adoption – one should not dismiss: significant output gaps, ageing of society (keeping velocity of money at bay), massive debt loads, increasing prevalence of zombie companies inhibiting pricing power of peers. Additionally, given the gap between the earnings yield and risk free rates, equities carry a more-than-reasonable inflation hedge. Thus, the inflation impact on any potential equity style rotation should not be overplayed. Rather, it merits more attention to focus on the structural drivers of any growth or value oriented sector to gauge its potential longer term prospects. Banks, for instance, are often touted as inflationary beneficiaries (due to the link with a steepening yield curve), but we deem structural headwinds more impactful and increasing in the longer term: the upcoming IPO of ANT Financial illustrates this conviction, as it encroaches more into the different traditional métiers of a bank in China (payment, consumer finance, wealth management, loans to small and medium-sized enterprises ) leveraging on its vast, installed user base and offering a superior consumer experience. In developed markets, more platform or fintech providers adopt ANT’s playbook, who itself is also starting to make inroads in developed markets. Banks risk being stuck in the middle (losing access to the final client), especially if they are not cognisant of this disruptive force and unable to adapt swiftly. Again, digitisation is crucial here.

Equity markets have been fairly resilient despite the resurgence of COVID cases and the uneven recovery we have seen till now. Some parts of the economy have recovered quickly, or are even overheating (look no further than the US lumber prices). However, subsectors relying on crowds continue to be affected and some, like the airline industry, have announced sizeable layoffs. Given the inherent labour intensity of these subindustries, social inequality (especially in the US) has further increased. More targeted fiscal measures are needed. Although Democrats and Republicans have not agreed on a new fiscal package yet, we expect a consensus to be reached. Unfortunately, nowadays, more often than before, this happens after some ‘rounds of political posturing’. Likewise in Europe, with a renewed episode in the Brexit saga, we also expect a middle ground to be found in the latest hour. With the advent of an effective vaccine (at the end of the year or beginning of next year), continued monetary and increased fiscal support, we expect the macro bounce to continue and to be more evenly spread. This could benefit companies that have seen the biggest impact from the sanitary crisis, although we would be very selective in picking so-called COVID-losers. The quality of the business model, balance sheet, and the potential to emerge stronger are key aspects in this selection process. As said on previous occasions, the core of any equity portfolio should consist of quality companies that are able to grow their top line through the cycle, with competitive advantages, relatively low leverage, less prone to disruptive forces and –ideally- with an ability to capitalise on the so-called sustainable development goals. In sum, a mildly positive backdrop for equity markets, although we do not expect fireworks either, as a widespread recovery has been well anticipated (and big index constituents have already done well this year). We stick to our view of a range-bound equity environment. Often, most of the upside in equity markets is realised when ‘things go from very bad to bad.’ In our view, the biggest risks for the last quarter of the year are a contested US election and a renewed spike in mortality rates due to COVID.

Alexander Roose , September 2020

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |