| https://www.next-finance.net/en | |

|

Strategy

|

Market neutral l/sto remain under pressure

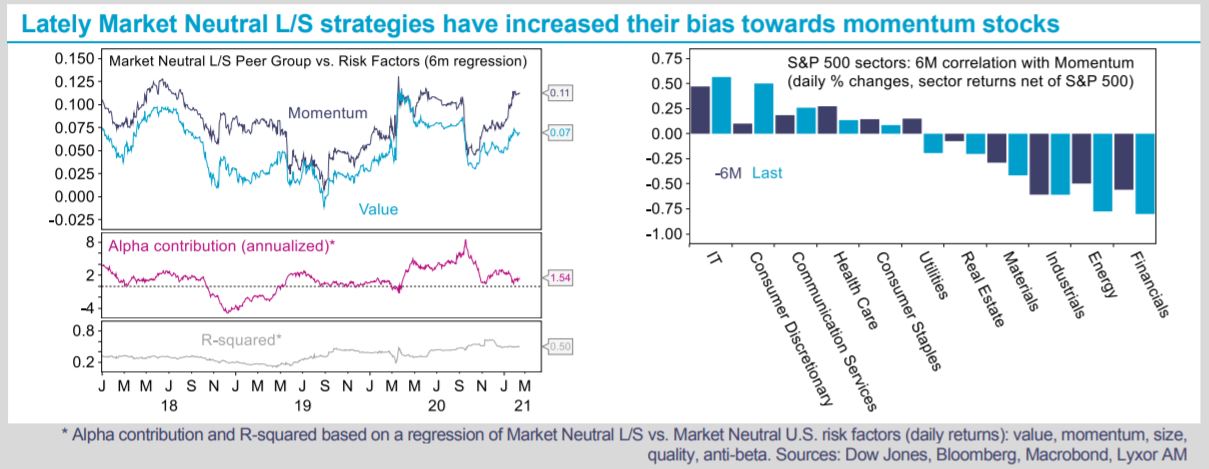

In recent months, Market Neutral L/S strategies underperformed other hedge fund strategies, in a context where risk assets rallied following the Pfizer vaccine announcement in November 2020. While the strategy is not designed to capture the equity market beta, the alpha contribution has declined since Q4-2020.

Article also available in :

English ![]() |

français

|

français ![]()

In recent months, Market Neutral L/S strategies underperformed other hedge fund strategies, in a context where risk assets rallied following the Pfizer vaccine announcement in November 2020. While the strategy is not designed to capture the equity market beta, the alpha contribution has declined since Q4-2020. Our stance on the strategy remains Underweight on the back of its exposure to the Momentum risk factor, which appears poorly suited for the current environment.

Market Neutral L/S experienced diverging fates in the past three months, but on average their performance has been disappointing, as it was already last year. This contributes towards explaining outflows from the strategy in 2020 and raises question marks going forward. Risk premia strategies, which in some cases can be associated with Market Neutral L/S, also struggled. On a positive note, multi-strategy platforms and offshore Market Neutral L/S strategies fared better last year.

Our views on the strategy remain quite defensive for two main reasons. First, Market Neutral L/S is a defensive strategy by nature, which is less attractive as the global economy heads towards a recovery.

Equity valuations are rich, and the strategy will help protect portfolios if the market rally reverses. However, this source of risk appears manageable in 2021 although we don’t exclude regular bouts of volatility as bond yields normalize at a higher level. Second, our estimates suggest the Market Neutral L/S and in particular, quantitative approaches, display a significant long bias towards the Momentum risk factor in equities. Although the attractive excess returns generated by this risk premium have long been documented in the academic literature, we find its correlation to the Value risk premium close to all-time lows at present. Momentum strategies in equities remain especially short financials and energy sectors. With bond yields starting to edge higher, the Momentum risk factor in equities appears vulnerable and may deliver minimal returns in the midterm. Although Market neutral L/S strategies have diversified this source of risk by gaining exposure to Value stocks, the returns of such strategies might continue to disappoint for some time, in relative terms, even if we adjust for volatility.

Lyxor Research , February 2021

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |