| https://www.next-finance.net/en | |

|

Opinion

|

Inflation in developed economies is on the rise

Inflation in developed economies is on the rise. Central banks and markets are currently relaxed about the upswing but this will change if economic growth revives from its recent mediocre pace.

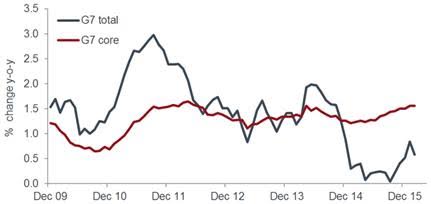

Consumer price inflation in the Group of Seven (G7) major economies rose from zero in September 2015 to 0.6% in February. More worryingly, “core” inflation – excluding food and energy prices – reached 1.6% in February, a four-year high.

G7 consumer prices

Source: Datastream, G7 Total and G7 Core prices, December 2009 to February 2016

Food and energy won’t suppress the headline inflation rate for much longer. If commodity prices remain at current levels, headline inflation is likely to move slightly above the core rate by end-2016. Assuming stable core inflation, this would imply a rise of about 1.75 percentage points in the headline rate from its recent low.

Upswing could continue

The core upswing may extend. Fluctuations in core inflation in recent years can be largely explained by two influences – labour market tightness and lagged pass-through of commodity price changes. The core rate tends to rise or fall depending on whether the G7 unemployment rate is below or above 6%. This “Phillips curve” relationship, however, has been regularly disrupted by large commodity price swings, which feed through to core inflation after about a year.

The unemployment rate fell below 6% in early 2015 and core inflation started to rise on cue. Commodity prices, however, simultaneously weakened sharply, their year-on-year fall reaching a maximum in mid-2015. This weakness moderated the increase in core inflation during 2015 and will remain a drag for much of 2016, allowing for the usual lag.

The tight labour market, though, should continue to exert upward pressure on core inflation, with the unemployment rate down further to 5.5% in January. The core rate, indeed, could rise sharply from late 2016 as commodity prices turn from being a headwind into a tailwind.

The policy response

How will central banks respond? If economic growth remains weak, they will probably look for excuses to maintain loose policies. A possible approach would be to argue that inflation should be allowed to overshoot for a while to compensate for the 2015-16 undershoot.

A rebound in growth later in 2016, however, is a plausible risk. Solid global money and credit trends suggest that an upside surprise is more likely than a recession. A dual acceleration of prices and economic activity would force reluctant central bankers to tighten.

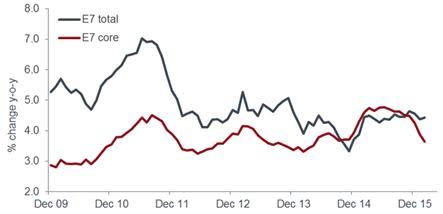

Rising inflation, it should be emphasised, is an issue for developed rather than emerging economies. Core pressures in the “E7” large emerging economies are moderating in response to weak activity and currency stabilisation. Falling inflation is opening the door to central bank easing even as G7 prospects argue for less accommodative policy.

E7 consumer prices

Source: Datastream, E7 Total and E7 Core prices, December 2009 to February 2016

Source: Datastream, E7 Total and E7 Core prices, December 2009 to February 2016

Simon Ward , April 2016

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |