| https://www.next-finance.net/en | |

|

Opinion

|

High dispersion of hedge funds’ returns in panic markets

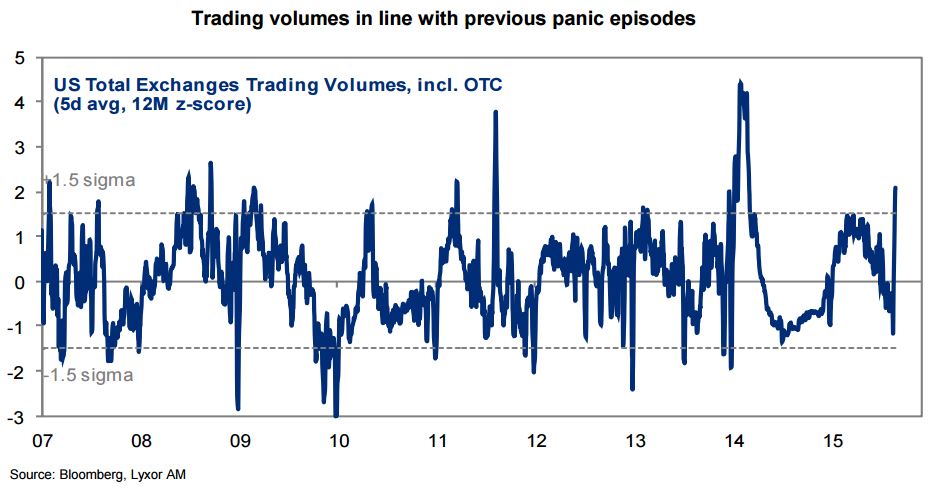

The deflation and growth scares morphed into a vicious cycle last week. Multiple trading anomalies were observed, especially on Monday, suggesting that systematic and algorithmic trading amplified the sell-off.

Article also available in :

English ![]() |

français

|

français ![]()

The deflation and growth scares morphed into a vicious cycle last week. Multiple trading anomalies were observed, especially on Monday, suggesting that systematic and algorithmic trading amplified the sell-off.

The bottoming process has already begun, but the sentiment remains febrile. On the one hand, the apparent disconnection of this sell-off with macro data is opening bargain opportunities. On the other hand investors are pondering whether a more fundamental change is being priced in, which would suggest a more bearish phase for risky assets.

Current concerns include:

- The true magnitude of the Chinese slowdown

- The risk of an FX crisis in some of the weakest EM countries

- The actual resilience of global growth to another round of deflationary pressures

- The uncertainty around the Fed’s normalization (the plunge in EM assets and commodities follows the April rout for sovereign bonds)

- Monetary policies’ ability to deal with any of these potential shocks.

Over the week, global equities plunged by 9%, the USD trade weighted dropped by more than 2.5%, energy spots plunged by another 10% and base metals lost 4%.

The Lyxor Hedge Fund Index was down 3.5% over the same period. Event Driven funds were the main losers. There was high dispersion in managers’ return, with losses in some heavy-weight funds.

Overall, CTAs and Fixed Income Arbitrage funds proved to be reasonably resilient. A milder pressure on credit and govies supported credit strategies.

The losses in the L/S Equity space were reasonable, with the notable exception of Asian and US long bias managers. A high dispersion was recorded among Global Macro funds.

Jean-Baptiste Berthon , Philippe Ferreira , September 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |