| https://www.next-finance.net/en | |

|

Strategy

|

Five reasons why special situations outlook is brightening

Special Situations strategies have been under pressure in 2020, both on their event and credit arbitrage books. Due to their long structural market beta, managers have underperformed early this year. They have retraced most but not all they have lost.

Article also available in :

English ![]() |

français

|

français ![]()

Special Situations strategies have been under pressure in 2020, both on their event and credit arbitrage books. Due to their long structural market beta, managers have underperformed early this year. They have retraced most but not all they have lost. Being deep-value oriented, they have not fully benefitted from the rally, which primarily boosted other market segments. As a result, the beta contribution explains most of their 2020 returns, with limited alpha generation.

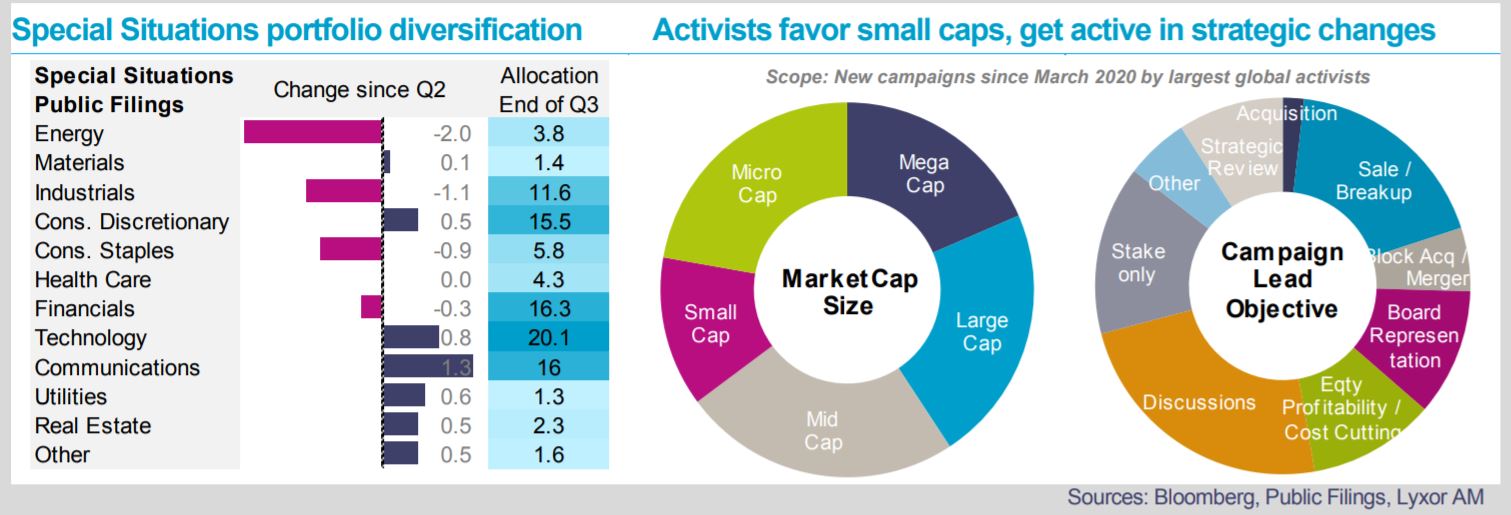

We think the tide has now turned in their favor for several reasons. First, prospects of large-scale vaccination and global economic normalization over 2021, and greater policy clarity in the U.S. would turn investors’ attention to fundamentals and value stocks. Continued stimulus support would also prevent large-scale corporate defaults. Special Situations would be prime beneficiaries. Second, portfolios are now more diversified, thus less risky. After March, most Special Situations managers rotated away from the prime victims of the virus, in favor of softer catalyst positions, cyclical value assets, as well as those belonging to the post-covid world (public filings show a reweighting of consumer discretionary and stocks of the new economy). Some managers, that little changed their portfolios earlier this year are rebounding the strongest since November. Third, after a nearly full-stop in corporate operations in H1, asset sales, M&A, IPOs, and spinoffs have all revived. Part of the recent spike is fueled by the pipeline of operations that had been postponed due to uncertainty or as due diligences were interrupted. Yet, early indicators (including the number of extraordinary meetings where corporate operations are decided, or undeployed cash from private equity standing at $2tn) point to sustained activity in 2021. These hard-catalysts are essential for Special Situations strategies. Fourth, a closer look into activist books – usually reliable lead indicators for other Special Situations segments – reveals that market beta exposures are back in full swing, showing greater confidence. New campaigns launched since March predominantly focused on smaller caps. Specifically, they targeted cheap, lagging value positions, with mixed credit conditions, in financial and industrial sectors, but displaying strong operational leverage and cyclical bias. Also, while the lead objectives of campaigns back in April seemed largely opportunistic (holding discussions, building stakes), activists are now increasingly seeking strategic changes (acquisition/assets sales, shareholders distribution, or governance change), a sign that turnaround situations are back in favor. We also note that they are increasingly looking for cheaper opportunities in Europe and Japan (in these regions friendly, suggestivist, or constructivist approaches tend to work better than hostile activism). Fifth, U.S. activists tend to welcome prospects of a split Congress (were the Senate to retain a Republican majority), with least changes to antitrust, taxes and energy/healthcare regulations. A Democratic Congress would at least translate into stronger stimulus, favorable for smaller caps. All in all, we see powerful tailwinds for Special Situations strategies in 2021.

Three weeks after U.S. elections and the vaccine announcement, the momentum in risk assets remained strong, led by U.S. and Japanese equities, oil prices and energy and financial sectors. Gold, the U.S. dollar, and other safe-haven assets.

All hedge fund strategies were up this week. Special Situations continued their strong monthly rally. Our peer group has fully retraced earlier losses. Some managers had little changed their portfolios after the crash and ignored the short-term extreme volatility. While they deeply suffered in H1, they rebounded the most in November, boosted by positions linked to airlines and tourism.

L/S Equity diversified strategies also captured part of the rally, though they generated little alpha due to their weaker exposures to value stocks and their weak directionality.

Lyxor Research , December 2020

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |