| https://www.next-finance.net/en | |

|

Opinion

|

Fed passes its turn

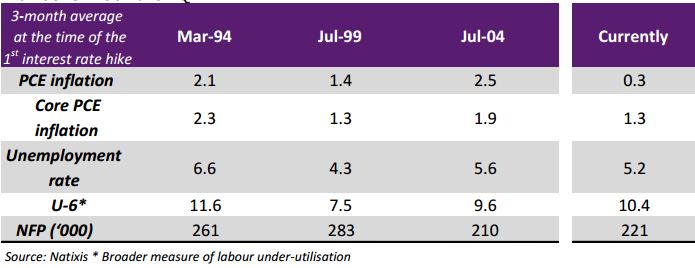

This had been one of the most eagerly awaited FOMC meetings, but in the end the Federal Reserve decided to pass its turn. The last time the Fed Funds rate was raised, back in June 2006, there was a far more compelling case, making the central bank’s job a good deal easier: unemployment was even lower than it is now (4.6% vs. 5.1%) and inflation towered at 4%, while growth reached 2.7% and the 10-year rate stood at 5.1%.

Article also available in :

English ![]() |

français

|

français ![]()

This had been one of the most eagerly awaited FOMC meetings, but in the end the Federal Reserve decided to pass its turn. The last time the Fed Funds rate was raised, back in June 2006, there was a far more compelling case, making the central bank’s job a good deal easier: unemployment was even lower than it is now (4.6% vs. 5.1%) and inflation towered at 4%, while growth reached 2.7% and the 10-year rate stood at 5.1%.

Currently, while the labour market is bearing up, inflation is 0.2%, lower than it was back in 2012 when the Federal

Reserve embarked on another round of QE.

Yet, back in July, Janet Yellen had explained that the US economy “can not only tolerate but needs higher rates”. It seems that the timeliness of an interest rate hike was discussed, but the FOMC decided that “a little more time was needed” even though there was a case for acting now, as pointed out by Janet Yellen during the press conference.

Clearly, developments in China, the strength of the US dollar and the downturn in commodity prices tipped the scales, the Federal Reserve taking the easy option, i.e. way for better visibility. The fall in crude oil prices and the appreciation of the US dollar will drive down inflation for slightly longer than had been envisaged initially by the FOMC.

The real change in the FOMC Statement lies the assessment that the “recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term”. China and emerging countries are seen as a risk for US exports, but not to the point of undermining the FOMC’s global scenario according to Janet Yellen, who explained that the “situation abroad bears close watching”.

There remains that the Federal Reserve is not hugely enthralled by the improvement seen by the labour market, which was played down. NAIRU has been lowered to 4.9%, although the Federal Reserve need not wait until this level is reached before acting.

On balance, we now expect the Federal Reserve to move in December. The Fed Chair repeated that “every meeting is a live meeting”, adding that a rate increase could be decided at the October meeting, at which point the Federal Reserve would call a press briefing.

Our scenario remains based on largely positive economic growth in the short term: while we are less bullish than the market consensus, our estimates nonetheless imply that growth will lastingly exceed its potential, which ought to lead to another improvement in the labour market. With relatively strong growth in employment, average hourly earnings that should accelerate slightly, and an improvement in purchasing power from lower gasoline prices, consumption will remain the main engine of growth. The construction sector can also be expected to fuel growth going forward. Although we see two factors that are likely to hold back growth (woes of the mining sector, negative contribution by foreign trade), the economic environment will remain buoyant. Concurrently, our assessment is that external risks (China in particular) would have limited consequences for the US economy. At any rate, these risks are not such as to bring into question the monetary tightening cycle planned by the Federal Reserve.

The weak inflation is explained by two main factors: (1) the main factor is the decline in crude prices, over which the Federal Reserve exerts no influence; and (2) the lagged impact of the US dollar’s appreciation on the price of imported goods, which can be expected to fade rapidly. The transitory nature of these factors, the stability demonstrated by inflation expectations and rise in prices for services mean that the Federal Reserve has a sufficiently high level of confidence to anticipate inflation recovering to 2% (which is the central bank’s official target) within two years.

Timing according to Fed Funds futures

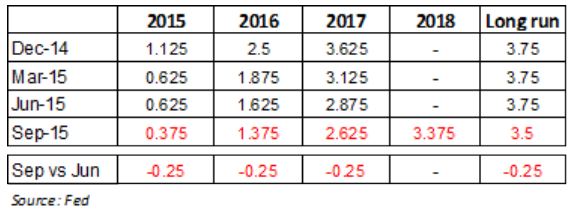

Before the FOMC meeting, the market’s view was that there was a 30% probability of an interest rate in September, with one interest rate hike priced in full by the end of the year. Two further interest rate hikes in 2016 were priced in by Fed Funds futures. After the meeting, the market still doubts rates will be raised this year (only a 50% probability of a hike by December), even though the dot plot suggests that the Federal Reserve will move before the end of the year.

Currently, FOMC members expect rates to be raised once this year, whereas at the June meeting they expected two interest rate hikes this year.

Next year, members see the Fed Funds rate around 1.375% at the year-end, which not as low as was being anticipated before.

Over the long run, the members put the equilibrium level at 3.50%, down from 3.75% previously.

The scenario therefore remains for a monetary tightening cycle that does not add up to real normalisation of monetary policy, but rather a slight tightening, i.e. far more subdued than previous monetary tightening cycles. Even then the 3.50% equilibrium level may seem nearly optimistic.

Average rise in Fed Funds rate during previous monetary tightening phases

Jean François Robin , Thomas Julien , September 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |