| https://www.next-finance.net/en | |

|

Strategy

|

Dollar depreciation helps CTAS

Since the U.S. presidential election on November 3 th, the USD has started a descent that may have legs under the new administration. The easing of trade tensions and an accommodative policy mix could put additional pressure on the DXY, which was down -1.7% since the election, to the benefit of European currencies.

Article also available in :

English ![]() |

français

|

français ![]()

Since the U.S. presidential election on November 3 th, the USD has started a descent that may have legs under the new administration. The easing of trade tensions and an accommodative policy mix could put additional pressure on the DXY, which was down -1.7% since the election, to the benefit of European currencies. Two runoff Senate elections in Georgia on January 5th will have key implications for the outlook. A Democratic Senate majority would entail more aggressive fiscal accommodation and probably a weaker USD. Current polls suggest the race is very tight.

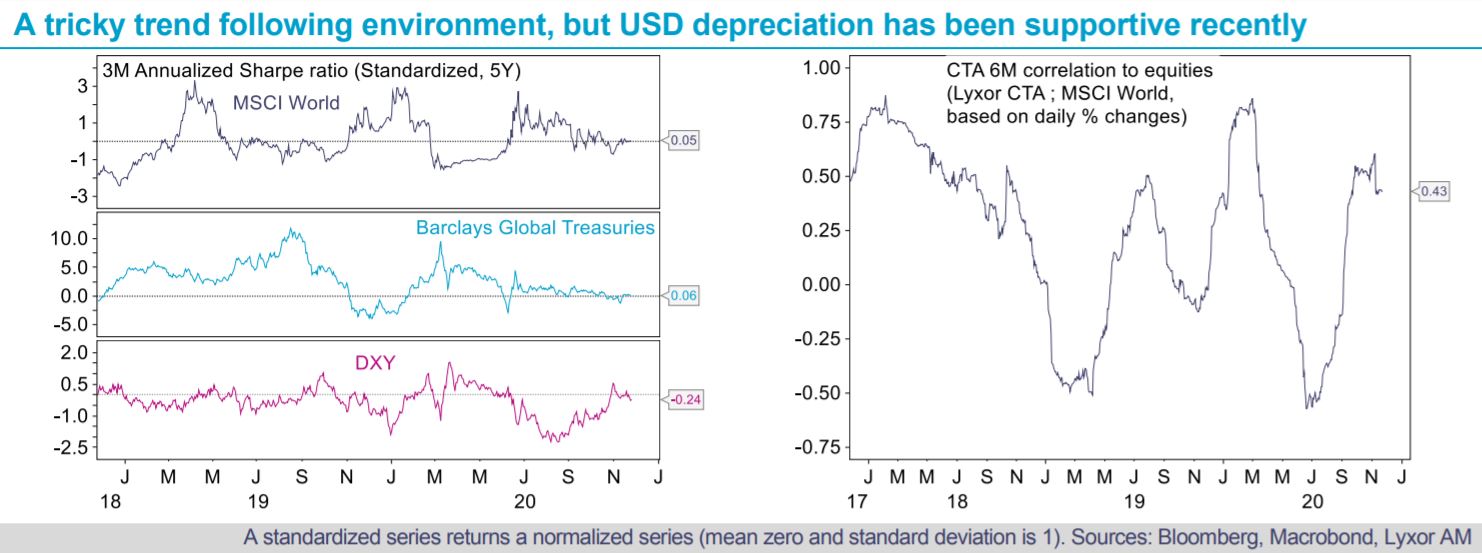

In the alternative strategies space, CTAs and Global Macro strategies have largely benefitted from the downward USD trend. After difficult months for CTAs due to trend reversals in equity, bond, and commodity markets, a solid downward USD trend would be supportive.

CTAS typically face difficulties during deep transitions such as the one we are experiencing now. The announcement of a Covid-19 vaccine earlier in November fueled cyclical assets (equities, HY credit, oil, EM currencies) vs. defensive ones (sovereign bonds, gold, DXY). CTAs were on the right side in FX and are adjusting their positions on other asset classes. The long gold/ short energy trade was costly in recent weeks for those who trade commodities.

Yet, dispersion is high and within a CTA universe that we estimate is down -5% so far this year, we find some strategies up in excess of +7%. Short to midterm CTAs largely outperformed long term CTAs and strategies with a higher degree of diversification underperformed.

Going forward, CTAs’ correlation to equities has started to normalize at a higher level. This suggests the strategy should not lag too much if the rally in risk assets continues. From a different angle, the strategy currently provides diversification and would remain highly resilient if hopes of an economic recovery fade. Our stance stands at Neutral, considering the headwinds discussed above, but also the opportunities from a bottom-up perspective. Midterm strategies have shown to be highly resilient in Q1 and opportunistic in the rest of the year. They should be favored as market conditions continue to evolve rapidly.

Lyxor Research , November 2020

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |